Introduction

Most retirement advice is built on a lie: the idea that your home is your greatest asset. In reality, for many Americans over 60, the family home has quietly transitioned from a “Nest Egg” into a Strategic Debt Trap.

But how do you know if you are sitting on a gold mine or a ticking financial time bomb?

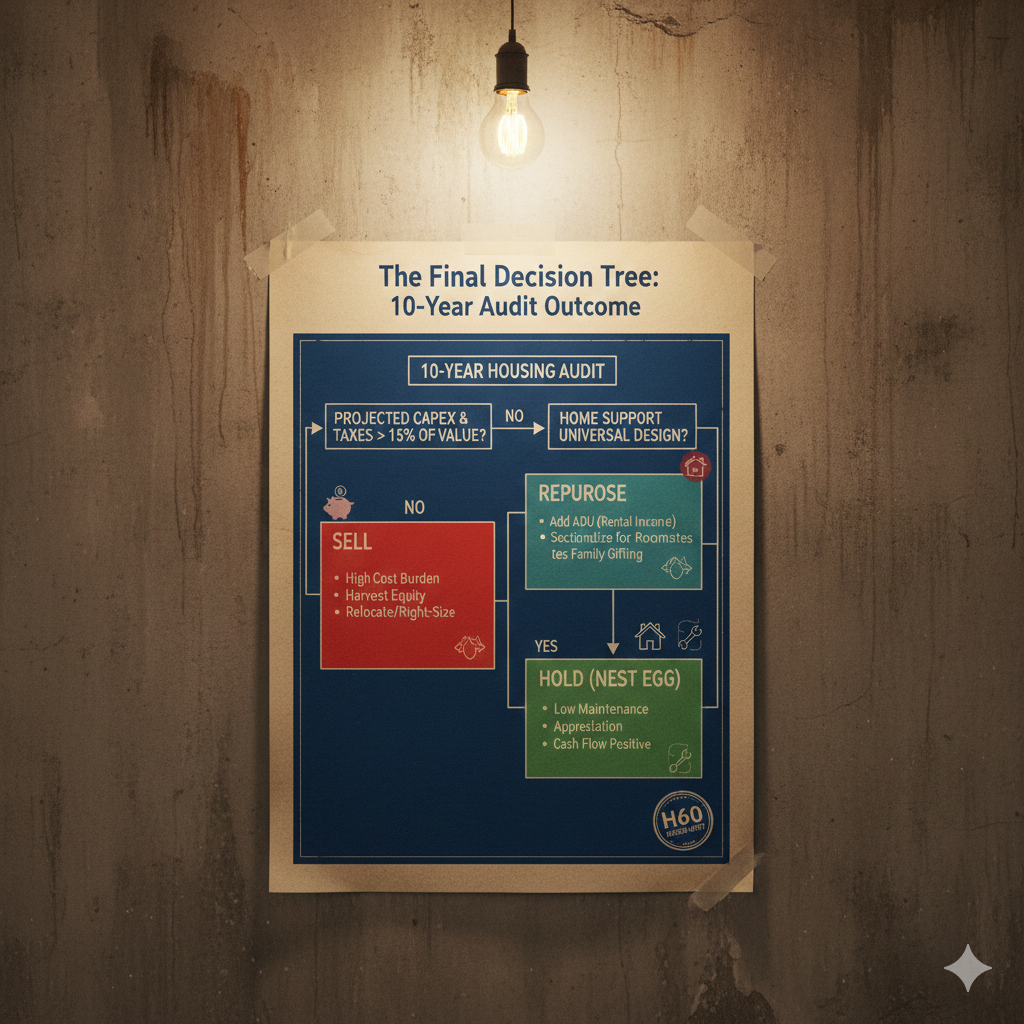

You don’t guess—you audit. Today, we are applying Charles O’Dell’s 10-Year Housing Audit, a first-principles logical framework designed to strip away the nostalgia and look at the cold, hard math of “Cluster Failure” windows and equity erosion. This isn’t a checklist of “handyman tips.” It is a technical deep-dive into the 15% Rule and the Asset vs. Liability Matrix. By the end of this audit, you will have a data-backed directive: Sell, Hold, or Repurpose. If you aren’t willing to look at your primary residence as a cold line item on a balance sheet, stop reading now. If you want to protect your net worth for the next decade, let’s begin the calculation.

Video Guide Overview

Affiliate Disclosure

This article contains links to specific tools and technologies that I recommend for home auditing and safety. If you purchase through these links, HousingAfter60 may receive a commission. I only recommend products that meet my technical standards for durability and ROI.

The Short Answer

For senior housing needs, the 10-Year Housing Audit is a binary assessment: if the projected cost of maintenance, taxes, and physical retrofitting exceeds the cost of a strategic relocation by more than 15 percent over a decade, you must move. Staying is only logical if the structural integrity of the home supports “Universal Design” without exceeding 25 percent of the current market value in renovation costs.

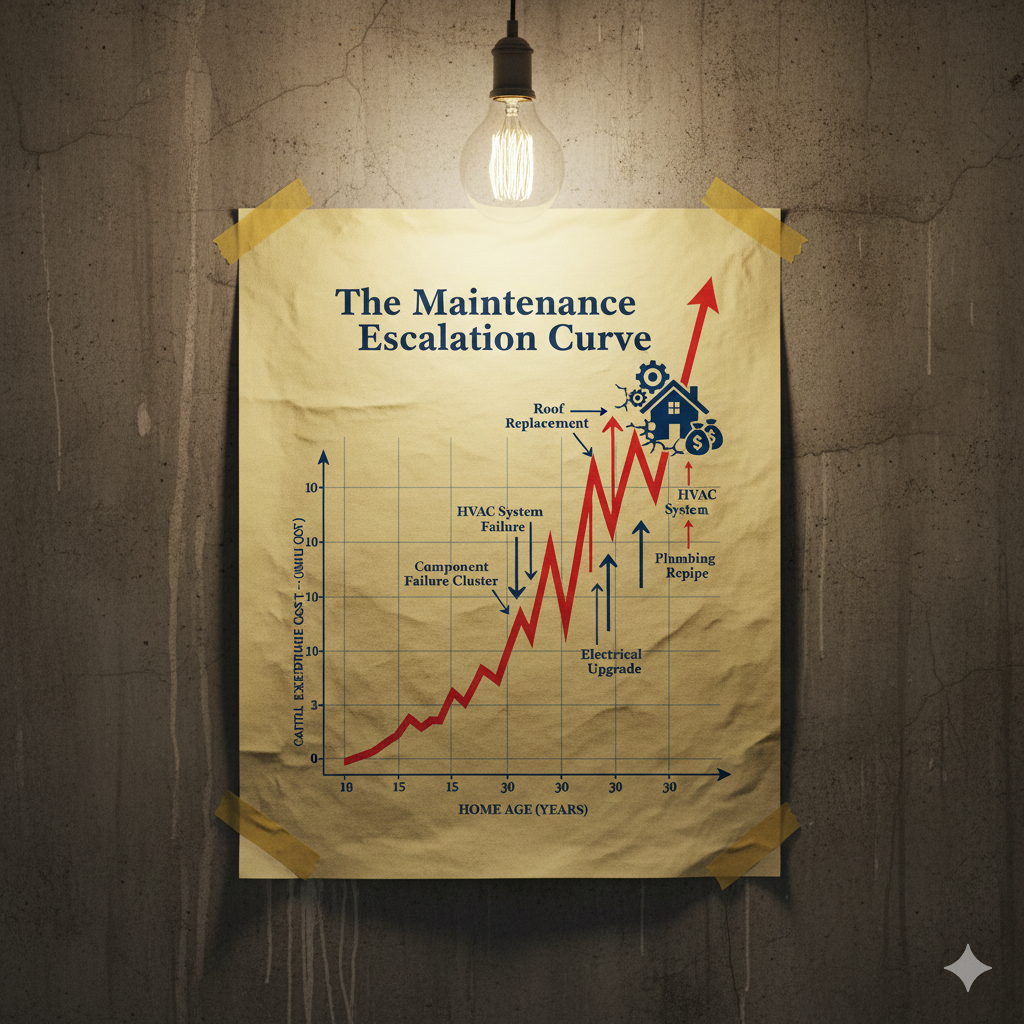

The Financial Physics of Aging Property

Properties do not age gracefully. After two decades in this business, I can tell you that systems fail in predictable cycles. If your home was built or last renovated 20 to 30 years ago, you are entering a “Cluster Failure” window. This is when the HVAC, roof, and water heater all reach their end-of-life simultaneously. In 2026, the cost of labor has shifted significantly. We are no longer in a market where a few thousand dollars fixes a major system.

I view a home through the lens of first-principles logic: a house is a collection of depreciating components sitting on an appreciating piece of land. To ignore the depreciation of the components is to bleed equity. In the 2026 market, labor costs for skilled trades have plateaued at historic highs. Replacing a roof today costs significantly more than it did five years ago. You must calculate these “Shadow Expenses” into your 10-year projection. If you stay, you are signing up for a capital expenditure (CapEx) schedule that most retirees are unprepared for. The 1 percent rule for maintenance is now a 2 percent reality for homes over 30 years old.

Technical Deep Dive: The 2026 Capital Expenditure Reality

Let’s look at the numbers. A 2,500 square foot home built in 1996 is now 30 years old. Logically, the original architectural shingles have reached their terminal velocity. In 2026, a tear-off and replacement with architectural shingles averages 7 dollars to 10 dollars per square foot. That is a 20,000 dollar to 25,000 dollar hit. Simultaneously, your copper plumbing may be reaching a point of pinhole leak clusters, particularly if your local municipality has high mineral content in the water. A full repipe in 2026 using PEX-B materials will run between 8,000 dollars and 15,000 dollars depending on the number of fixtures. If you stay, you are essentially buying your house back from the contractors one system at a time.

Tax Implications and IRC Section 121

From a technical standpoint, your primary residence is a tax-advantaged vehicle, but it has a ceiling. Under current IRS rules, a married couple can exclude up to 500,000 dollars of gain from the sale of their home. If you have lived in your home for 30 years in a high-growth market, you likely have equity that far exceeds this threshold. Staying longer only increases the tax trap where more of your net worth becomes illiquid and subject to capital gains upon your eventual exit.

I often advise clients to harvest their equity now, reset their tax basis in a new property, and move the surplus into a more liquid, income-producing asset. This is especially relevant in 2026, as discussions regarding modernizing the tax code to reflect housing inflation are ongoing, but current limits remain fixed. If your gain is 800,000 dollars and you are married, that 300,000 dollar excess is taxable. By selling now and right-sizing, you can lock in that 500,000 dollar tax-free gain and put it to work elsewhere. This is the difference between having a 300,000 dollar tax bill later or 300,000 dollars in a high-yield account now. The math does not lie.

Structural Engineering: The “Universal Design” Filter

You cannot will yourself to be mobile forever. A logical audit requires a technical assessment of your home’s skeleton. Most homes built in the late 20th century were designed for young, able-bodied families. They feature narrow 30-inch doors, sunken living rooms, and master suites on the second floor. These are structural liabilities for anyone over 65.

To stay, your home must pass the Universal Design test. Can a wheelchair navigate the hallway? Is there a 5-foot turning radius in the bathroom? If the answer is no, you are looking at structural remediation. Widening a door is not just about trim: it often involves moving electrical runs, plumbing stacks, or load-bearing studs. If your home is built on a concrete slab, moving plumbing for a zero-entry shower requires jackhammering the foundation. In 2026, a high-end bathroom gut-renovation for accessibility can easily exceed 35,000 dollars. If the cost to retro-fit your current home exceeds the transactional cost of buying a new, modern-spec home, the data says you should move.

Deep Dive: Load-Bearing Wall Modifications

Many seniors believe a “remodel” is a simple cosmetic fix. It is not. To widen a hallway from 36 inches to the ADA-recommended 48 inches usually requires stealing space from adjacent rooms. If those walls are load-bearing, you are looking at temporary shoring, the installation of LVL (Laminated Veneer Lumber) headers, and significant drywall and flooring repairs. In 2026, the price for a single structural opening can range from 4,000 dollars to 7,500 dollars. Multiply that by every doorway in your home. You are looking at a 50,000 dollar structural bill before you even pick out a paint color. This is why staying in a non-conforming home is often a financial catastrophe.

Zoning and Regulatory Hurdles for ADUs

One way to make staying logical is through “Income Offsetting.” In 2026, many municipal zoning laws, particularly in states like Arizona and California, have shifted to allow Accessory Dwelling Units (ADUs). If your lot allows for a 600-square-foot cottage, you could potentially move into the ADU and rent out the main house. This turns your primary residence into a cash-flow asset.

However, you must audit the local zoning code. Does your municipality allow ADUs as a Permitted Use? What are the Setback requirements? In 2026, cities like Phoenix have cleared the way for ADUs on most residential lots, but strictly enforced HOA rules can still block you. You must know your local ordinances before committing to a stay strategy based on future development. Building an ADU is a 150,000 dollar to 250,000 dollar investment: it is not a hobby project. If you cannot generate at least a 7 percent cap rate on that investment, the project is a failure.

Shadow Regulatory Risks: Property Tax Reassessments

In many jurisdictions, a major renovation—such as adding an ADU or a massive accessibility overhaul—triggers a property tax reassessment. You might be currently paying taxes based on a 200,000 dollar valuation from twenty years ago. If the county assessor sees a 200,000 dollar permit for an ADU, they will reassess your entire property at current market value. In 2026, with property values at historic highs, this could quadruple your annual tax bill. This “Tax Shock” is a hidden cost that most “Aging in Place” advocates fail to mention. I don’t fail to mention it because I have seen it ruin portfolios. Your audit must include a call to the local assessor’s office.

Market Analysis: The 2026 Liquidity Crisis

We are currently seeing a divergence in the market. Large, multi-story suburban homes are becoming harder to sell because the primary buyer pool—Millennials and Gen Z—is struggling with affordability, while the aging population is trying to offload them. Conversely, single-story, accessible homes are at an extreme premium.

If you own a large family home, you are holding a “Degrading Asset.” Every year you wait to sell, you are competing with more people just like you who are also finally realizing they can’t handle the stairs. This creates a supply glut of “Senior-Owned Liabilities.” By selling now, you are exiting the market while there is still a thin layer of liquidity for these larger properties. If you wait ten years, you may find that the only buyers left are institutional investors looking to “bottom-fish” for 60 cents on the dollar. Logic dictates that you sell into strength, not weakness. This is the reality of senior housing needs.

2026 Cost Transparency Table

The following table outlines the projected costs for typical “Stay” vs. “Move” scenarios in the current economic environment. These figures represent national averages for mid-to-high-tier markets. Do not assume your “handyman” friend can do this for half; in 2026, unlicensed labor is a liability you cannot afford.

| Audit Category | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Bathroom Accessibility (Zero-Entry) | 8,500 dollars | 35,000+ dollars |

| HVAC & Heat Pump (2026 Specs) | 8,000 dollars | 22,000 dollars |

| Smart Home Safety Suite | 1,500 dollars | 6,500 dollars |

| Selling Costs (Comm. + Repairs) | 6% of Value | 10% of Value |

| Relocation/Downsizing Logistics | 3,000 dollars | 15,000 dollars |

| Electrical Panel Upgrade (200 Amp) | 2,500 dollars | 5,500 dollars |

The Opportunity Cost of Maintenance

Every dollar spent on a 20,000 dollar roof for a house you plan to leave in five years is a dollar with zero ROI. Buyers in 2026 expect a working roof: they will not pay a premium for it. They will, however, penalize you heavily if it is failing. This is the Maintenance Trap.

When you conduct your 10-year audit, you must look at your Opportunity Cost. If you sell now and move into a lower-maintenance condo or a newer active adult community, that 20,000 dollars—plus the saved property taxes and insurance premiums on a larger home—could be invested in a high-yield brokerage account. At a 7 percent return, 200,000 dollars in harvested equity yields 14,000 dollars a year in income. Staying in a house that drains 10,000 dollars a year in maintenance creates a 24,000 dollar annual swing in your net worth. Over ten years, that is 240,000 dollars. This is the logic of Right-Sizing. If you can’t see why 240,000 dollars is better than a bigger garage, you shouldn’t be managing your own finances.

Energy Efficiency and the 2026 Grid

Modern homes built after 2024 meet the 2021 International Energy Conservation Code (IECC) standards, which are approximately 34 percent more efficient than older benchmarks. Older homes have settled foundations that create air leaks, degraded insulation, and inefficient ductwork. A technical audit should include a thermal imaging scan of your home. If your “Envelope” is leaking, you are burning cash. Retrofitting an old home to meet 2026 efficiency standards—think R-60 attic insulation and smart HVAC zoning—is often a sunk cost. It is more logical to buy efficiency than to build it into an aging shell. In 2026, with electricity rates up 15 percent in many states, this is not a small detail; it’s a major monthly cash flow item.

Recommended Affiliate Products

If you decide to stay and audit your home’s efficiency and safety, these are the technical tools I trust for my own flips and senior-specific renovations. These aren’t toys; they are diagnostic equipment.

| Product Type | Brand/Model Recommendation | Technical Benefit |

|---|---|---|

| Thermal Imaging Camera | FLIR ONE Edge Pro | Detects heat loss and hidden moisture behind walls without demolition. |

| Smart Water Leak Detector | Moen Flo Smart Water Monitor | Automatically shuts off water to prevent catastrophic foundation damage. |

| ADA-Compliant Lighting Control | Lutron Caséta Wireless System | Eliminates the need for physical rewiring to add accessible wall switches. |

The “Lock-In” Effect: A 2026 Warning

In 2026, we are seeing the “Lock-In Effect” begin to fade as mortgage rates stabilize around 6 percent. However, many homeowners over 60 are still locked in to 3 percent rates from 2021. Logically, you might think staying is the only choice to keep that low rate. This is a fallacy. If your home costs you 15,000 dollars more per year in maintenance and taxes than a smaller, more efficient home, you are paying for that low rate twice over. Do not let a low interest rate anchor you to a sinking ship. A 6 percent rate on a 300,000 dollar home is mathematically superior to a 3 percent rate on a 600,000 dollar home that requires 40,000 dollars in immediate repairs. I see people clinging to their “cheap” debt while their “expensive” house eats their retirement. It’s foolishness.

The Insurance Crisis: A Technical Reality

We need to talk about the cost of insuring older homes. In 2026, many carriers are refusing to write policies for homes with roofs older than 15 years or electrical panels like the old Federal Pacific or Zinsco models. If you stay, you may find your premiums doubling or your policy canceled entirely. Relocating to a new-build or a certified retrofitted condo often slashes insurance costs by 40 percent. This isn’t just about saving money; it’s about being “insurable” at all. If you can’t get insurance, you can’t get a mortgage, and you can’t sell to anyone but a cash-heavy investor who will squeeze you on the price.

Actionable Audit Checklist

Run your property through this technical gauntlet. If you check more than three boxes in the Move column, your logic should dictate a listing agreement. Use a pen, not your feelings.

- Topography: Is the approach to the front door flat or stepped? (Stepped = Move)

- Major Systems: Is the roof, HVAC, or Water Heater >15 years old? (Yes = Move)

- Distance to Care: Is a Level 1 Trauma center or specialist more than 20 minutes away? (Yes = Move)

- Bedroom Location: Is the primary sleeping area on the second floor? (Yes = Move)

- Tax Velocity: Have property taxes increased by >20% in the last three years? (Yes = Move)

- Social Isolation: Can you walk to a grocery store or community center? (No = Move)

- Energy Score: Is your monthly utility bill >300 dollars for a 2-person household? (Yes = Move)

- Doorway Width: Are interior doors less than 32 inches wide? (Yes = Move)

- Foundation: Are there visible cracks or evidence of hydrostatic pressure? (Yes = Move)

- Insurance: Has your premium increased by more than 50 percent since 2023? (Yes = Move)

Internal Resources

To further refine your strategy, I recommend reading our deep dives on specific transition tactics:

- The Senior Downsizing Blueprint: How to Purge 30 Years of Junk in 30 Days (Coming Soon)

- Maximizing Home Equity: Reverse Mortgages vs. Right-Sizing in 2026. (Coming Soon)

- The Hidden Costs of Aging in Place: Why “Free and Clear” Homes Still Cost 2,000/Month (Coming Soon)

Summary

Deciding whether to move or stay is not a lifestyle choice: it is a capital allocation decision. You are the CEO of your retirement. A CEO does not keep an underperforming, high-cost factory open just because they like the view from the office. Perform the 10-year audit. If the math shows that your current home will cannibalize your savings through maintenance, taxes, and retrofitting, then sell. The 2026 market favors those who are mobile and liquid. Your children don’t want your 4,000 square foot liability; they want you to be financially independent. Sell the house, buy the freedom. Do not let your house become your cage.

About Charles O’Dell

Charles O’Dell is the founder of HousingAfter60.com and a veteran real estate investor with over 23 years of experience. He has successfully executed 100+ property flips and facilitated hundreds of transactions specifically for the 60+ demographic. Charles specializes in first-principles real estate logic, helping homeowners strip away the emotion to make high-ROI decisions about their living situations. He is widely considered a leading expert in senior housing transitions and 2026 market trends. He doesn’t believe in fluff, only the bottom line.

Written by Charles O’Dell: 23+ years experience, 100+ flips, and hundreds of senior housing transitions facilitated.