Introduction

CCRC Entrance Fee Audit 2026. I have spent 23 years analyzing property devaluations and contract law. When most people look at a CCRC, they see “peace of mind.” I see a massive capital deployment with complex liquidity constraints. If you are over 60, your primary residence is likely your largest asset. Moving into a CCRC requires liquidating that asset to pay an entrance fee that can exceed $1,000,000.

My goal is to determine if that capital is working for you or for the facility’s bondholders. In the current 2026 economic landscape, the cost of capital is too high to ignore. To truly protect your wealth, you must look past the brochures and perform a ruthless audit of the facility’s “Days Cash on Hand” and the structural integrity of the physical plant.

Video Guide Overview

Affiliate Disclosure

This article contains links to professional tools and services. If you purchase through these links, HousingAfter60 may receive a commission at no additional cost to you. I only recommend high-performance tools that meet my technical standards for real estate and financial auditing.

The Short Answer

CCRC Entrance Fee Audit 2026: My Technical Review of Type A vs Type C Contracts. A CCRC entrance fee is a pre-payment for future healthcare liabilities disguised as a real estate transaction. Whether it is a “trap” depends entirely on your projected health trajectory and the specific contract type (A, B, or C). In 2026, the primary risk is no longer just facility solvency, but the erosion of purchasing power on “refundable” portions and the high opportunity cost of tied-up capital.

Contract Typology: The Logic of Risk Transfer

The core of the CCRC model is the transfer of “longevity risk” from the individual to the institution. You pay an upfront fee to lock in a monthly rate for care that remains stable even if you require 24/7 skilled nursing. However, not all transfers are equal. We must categorize these into Type A (Extensive), Type B (Modified), and Type C (Fee-for-Service) to understand where the value truly lies.

Type A – Technical Deep Dive: Actuarial Math and ROI Trajectories

To understand the “Return On Investment” (ROI) of an entrance fee, we must apply first-principles logic to the “break-even” point. In a Type A contract, you are essentially purchasing an insurance policy. If the current cost of skilled nursing in 2026 is $15,000 per month and your CCRC monthly fee is $5,000, the facility is subsidizing $10,000 of your care monthly. If your entrance fee was $500,000, your “break-even” period begins only after 50 months of high-level care. If you die in independent living, the facility has captured the spread on your $500,000 for the duration of your stay. We must also account for the “lost” compounding interest. At a conservative 5% return, that $500,000 would have generated $25,000 annually in a brokerage account. Therefore, your real monthly cost in a CCRC is the Monthly Service Fee + (Entrance Fee * Opportunity Cost) / 12. If this sum exceeds the market rate for comparable private-pay home care, the CCRC is a net-wealth evaporator. You must analyze the “Days of Cash on Hand” for any facility you consider; if it is under 150 days, the facility is a credit risk. This is the same logic I use when evaluating investment liquidity in any high-stakes real estate portfolio. In 2026, the spread between Treasury yields and CCRC cost-subsidies has narrowed, making the Type A contract less mathematically attractive than it was a decade ago.

Tax Implication Logic: IRC Section 121 and 213

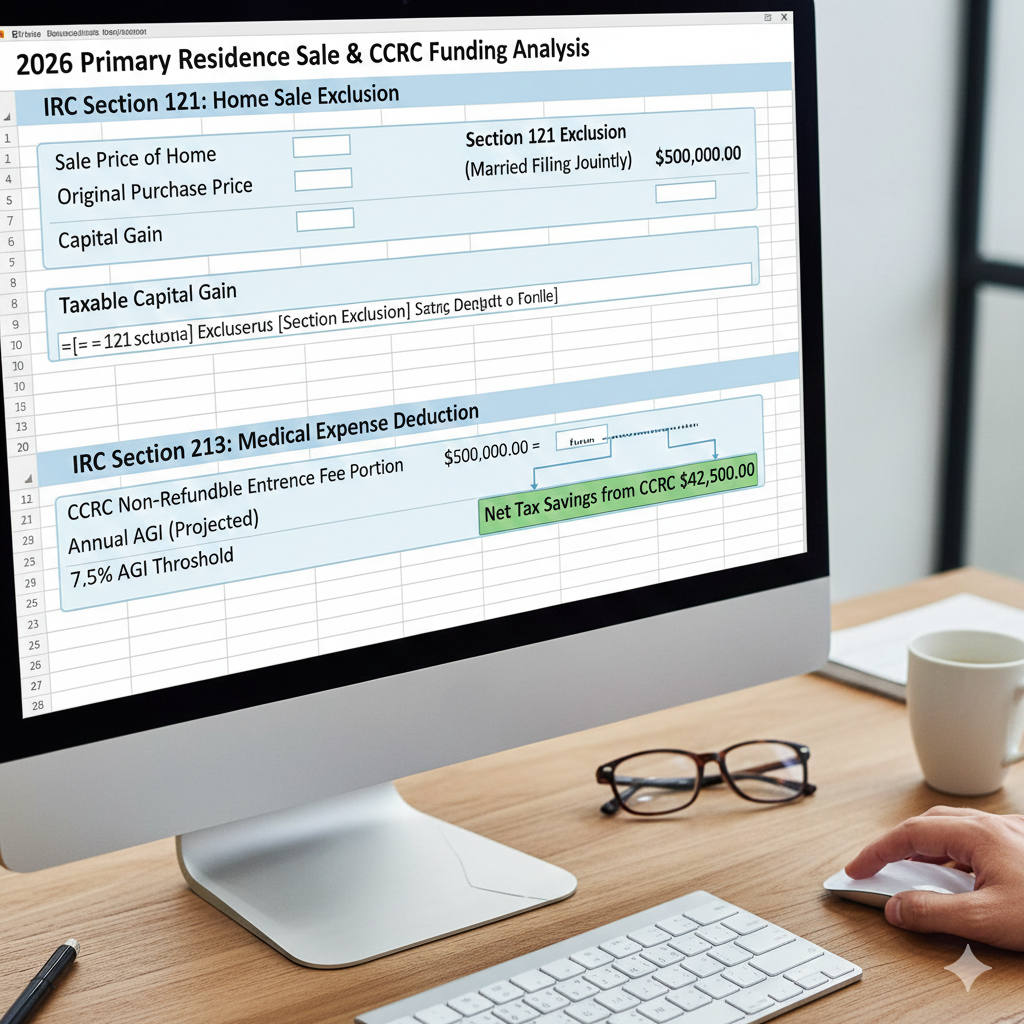

The IRS treats portions of CCRC entrance fees differently than standard real estate down payments. This is where most retirees fail to optimize their exit strategy from their primary residence. When you sell your home to fund a CCRC, you are triggering a massive liquidity event that must be shielded from the taxman with surgical precision.

Technical Deep Dive: Granular IRC Section 121 Analysis

Under IRC Section 121, you can exclude up to $250,000 (single) or $500,000 (married) of capital gains from your home sale. However, in 2026, many properties in high-demand markets have appreciated far beyond these limits. Any gain above the threshold is subject to a 20% long-term capital gains tax plus the 3.8% Net Investment Income Tax (NIIT). The CCRC entrance fee offers a unique “hedge” here. Under IRC Section 213, a significant portion of a non-refundable entrance fee: and even a portion of your monthly fees: can be categorized as a “prepaid medical expense.” This is deductible in the year of payment to the extent it exceeds 7.5% of your Adjusted Gross Income (AGI). By timing the home sale and the CCRC entry in the same tax year, you can use the Section 213 medical deduction to offset the capital gains tax liability that exceeds the Section 121 exclusion. This is a technical maneuver that requires precise coordination between your real estate broker and your CPA. Failure to align these dates results in a “dead” tax year where you pay maximum gains on the sale and have no income to offset with the medical deduction in the following year. This is a critical component of tax-efficient downsizing strategies for high-net-worth investors. Furthermore, you must verify if the CCRC provides an annual “Medical Percentage” letter, which specifies exactly how much of your monthly fee is deductible. Without this documentation, an IRS audit will disqualify the deduction.

Structural Engineering and MEP Life Cycles

When you “buy” into a CCRC, you aren’t just buying a contract; you are buying into a physical plant. If the facility has aging Mechanical, Electrical, and Plumbing (MEP) systems, your “Monthly Service Fee” is guaranteed to skyrocket as the facility faces special assessments or capital improvement costs. You are essentially a shareholder in a multi-million dollar infrastructure project.

Technical Deep Dive: Facility Infrastructure Audit

Before deploying $500k into an entrance fee, you must audit the facility’s Reserve Study. In structural engineering terms, look for the “Facility Condition Index” (FCI). An FCI over 0.10 indicates a facility with significant deferred maintenance. Specifically, investigate the HVAC cycles. Many CCRCs built in the late 1990s use centralized chiller systems that are reaching the end of their 25 to 30 year lifespan in 2026. Replacing a commercial-grade chiller plant costs millions. If the CCRC’s “Capital Reserve Fund” is underfunded (less than 70% of the recommended reserve), the residents will bear the cost through fee hikes. Furthermore, check the R-values of the building envelope. Poor insulation in older “Class B” facilities leads to massive utility overhead, which is passed directly to you. I prioritize facilities that have undergone LED retrofitting and sub-metering, as these are indicators of competent management that understands the bottom line. This is the same level of scrutiny I apply when performing commercial-grade inspections on 100+ unit multi-family flips. You should also ask about the roofing material: if they are using EPDM membranes approaching the 20-year mark, expect a major capital call soon.

2026 Cost Transparency Table

| Cost Category | Low-End (Type C / Basic) | High-End (Type A / Pro) |

|---|---|---|

| Entrance Fee | $180,000 – $350,000 | $600,000 – $1,200,000+ |

| Monthly Service Fee | $3,200 – $4,800 | $6,500 – $11,000 |

| Health Care Surcharge | Market Rate ($450/day) | $0 (Included in Base) |

| Annual Fee Inflation | 4% – 6% | 3% – 5% |

Zoning, Regulatory Hurdles, and Land Use

A CCRC’s financial stability is also tied to its ability to expand and adapt. If the facility is land-locked or faces local zoning restrictions, its ability to generate new entrance fees (its primary source of liquidity) is capped. This leads to a “fee-spiral” where existing residents must cover all operational deficits because there is no “new blood” funding the reserves.

Technical Deep Dive: Entitlement Risks and Expansion Logic

CCRC Entrance Fee Audit 2026: My Technical Review of Type A vs Type C Contracts. You must examine the “Use Permit” and “Master Plan” filed with the local municipality. If the CCRC is operating under a “Non-Conforming Use” status because of local zoning changes, they may be unable to rebuild in the event of a fire or natural disaster. Furthermore, check for “Density Bonuses” the facility may have utilized. If they have already maxed out their Floor Area Ratio (FAR), they cannot add more high-margin assisted living units to subsidize the lower-margin independent living residents.From a wealth protection standpoint, you want to enter a CCRC that owns its land fee-simple, rather than a facility on a long-term ground lease. Ground leases are ticking time bombs; as the lease expiration approaches, the facility’s ability to refinance debt vanishes, and your “refundable” entrance fee becomes a secondary claim behind the ground lessor and the primary mortgage holders. In 2026, we are seeing several CCRCs in urban corridors face massive lease escalations that threaten their very existence. Always ask to see the Title Report.

Affiliate Products for Financial Auditing

| Product Name | Primary Function | Target User |

|---|---|---|

| **EstateLogix Pro Suite** | Calculates 2026 Capital Gains vs. Medical Deductions. | Investors selling high-value primary residences. |

| **StructureCheck Infrared Scanner** | Detects thermal leaks and poor insulation in facility units. | Due-diligence focused prospective residents. |

| **ActuaryCalc 3.0** | Models break-even points for Type A vs. Type C contracts. | Family fiduciaries and financial planners. |

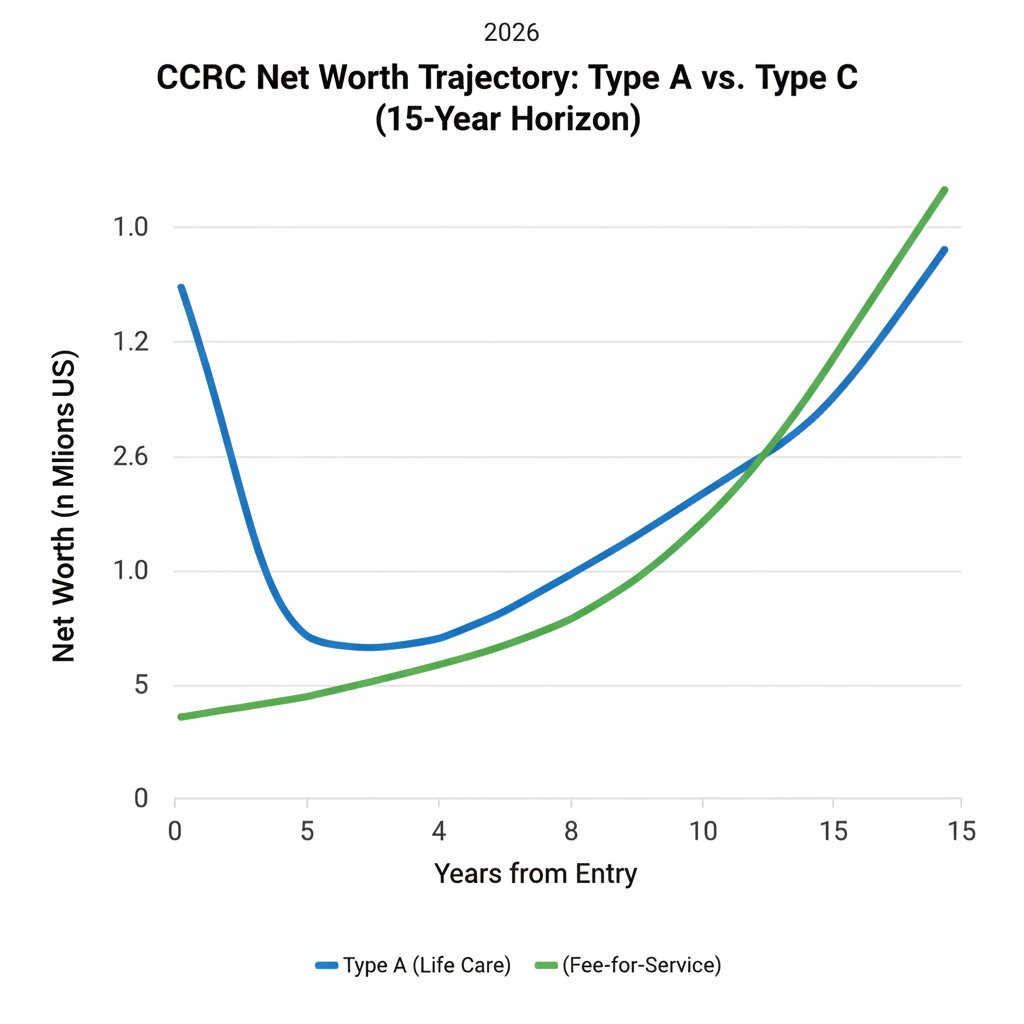

The 10-Year Net-Worth Trajectory

The final metric is the opportunity cost of the “Refundable” entrance fee. Many CCRCs offer a “90% Refundable” option. On a $500,000 fee, you expect $450,000 back. However, that refund is often not paid until your unit is re-sold to a new resident. This is a “latent liquidity” trap that many fail to model in their estate planning.

Technical Deep Dive: Liquidity Math and Inflation Erosion

If it takes 18 months to re-sell your unit after you vacate or pass away, your estate is out $450,000 of liquidity for that period. At a 2026 inflation rate of 4%, the purchasing power of that $450,000 erodes by $18,000 annually. More importantly, most CCRC contracts stipulate that the facility does not pay interest on the refundable portion. If you stayed for 10 years, and the market returned 7% annually, the $500,000 you “loaned” the facility for free would have grown to approximately $983,575 in a standard brokerage account. By choosing the CCRC, you essentially paid $533,575 in “hidden interest” for the privilege of the healthcare guarantee. You must decide if the $10,000 per month healthcare subsidy (if needed) is worth the $500k+ in lost capital growth. For many, the answer is “no,” and they would be better served by a “Fee-for-Service” model while keeping their capital in a diversified REIT or bond ladder. This is the same logic of capital preservation I apply when evaluating investment liquidity for high-net-worth clients.

Actionable Audit Checklist

- Audit the Disclosure Statement: Obtain the last 3 years of audited financial statements. Look specifically for “Net Assets without Donor Restrictions.”

- Check the Occupancy Rate: Anything below 90% is a red flag for financial instability and impending fee hikes.

- Verify the Refund Trigger: Does the refund pay out upon “move out” or “re-occupancy”? Never sign a “re-occupancy” clause without a 24-month sunset provision.

- Test the MEP Systems: Use a thermal scanner to check for window seal failures in the specific unit you are considering.

- Calculate the “Shadow Cost”: Add (Entrance Fee * 0.05) to your annual monthly fees to see your true cost of living.

- Interview the Residents’ Council: Ask about the frequency and percentage of fee increases over the last 5 years.

Internal Resources

- Tax-Efficient Downsizing: Protecting Your Gains (Coming Soon)

- Commercial Inspection Standards for Senior Living (Coming Soon)

- The Investor’s Guide to Liquidity in Retirement (Coming Soon)

Summary

CCRC Entrance Fee Audit 2026: My Technical Review of Type A vs Type C Contracts. A CCRC is not a home; it is a complex financial instrument. If you approach it with nostalgia, you will lose. If you approach it as a hedge against the 2026 healthcare market, you can find value. The “trap” is not the fee itself, but the failure to account for inflation erosion, tax timing, and the structural integrity of the facility’s balance sheet and physical plant. Prioritize Type C contracts if you have high liquid net worth and can self-insure. Use Type A only if you have a family history of longevity and want to cap your “tail risk” expenses. Above all, treat this as a business transaction, not a lifestyle choice.

2026 Audit: Aging in Place vs. CCRC Type A Investment

This table compares the 2026 median costs for a high-net-worth individual maintaining a 3,000 sq. ft. primary residence versus transitioning to a Class A “Life Care” CCRC. Note the inclusion of Opportunity Cost—the most overlooked metric in senior housing.

| Expense Category | Aging in Place (Monthly) | CCRC Type A (Monthly) |

|---|---|---|

| Housing/Rent/Entrance | $0 (Assuming Mortgage-Free) | $4,166 (Opportunity Cost of $1M Fee @ 5%) |

| Property Tax & Insurance | $1,200 – $2,500 | $0 (Included in Fee) |

| MEP Maintenance & Landscaping | $600 – $1,200 | $0 (Included in Fee) |

| Base Service/Monthly Fee | $0 | $5,500 – $8,500 |

| Home Care (40 hrs/week) | $5,400 – $6,200 | $0 (Prepaid via Entrance Fee) |

| Major Accessibility Mods | $2,500 (Amortized over 10yrs) | $0 (ADA Compliant Grade) |

| TOTAL MONTHLY LIQUIDITY BURN | $9,700 – $12,400 | $9,666 – $12,666 |

First-Principles Analysis

In the 2026 market, the “Total Monthly Liquidity Burn” is nearly identical for both options if you require part-time care at home. The CCRC model wins on volatility protection: if you need 24/7 skilled nursing (which costs $20k/month at home), the CCRC fee stays flat. Aging in place wins on capital control: you retain the 5% yield and the future appreciation of your primary residence, which historically outpaces CCRC “refundable” price increases. If your home is in a high-appreciation zip code, staying put is almost always the superior net-worth play.

*Data assumes 2026 national medians for Class A facilities and specialized in-home care agencies. Opportunity cost is calculated using a 5% risk-free rate on a $1,000,000 entrance fee.*

Bio: Charles O’Dell

Charles O’Dell is the owner of HousingAfter60.com and a veteran real estate investor with over 23 years of experience. Having flipped 100+ properties and facilitated hundreds of high-stakes transactions, Charles specializes in the technical and financial audit of senior housing solutions. He focuses on first-principles logic to help the 60+ demographic protect their net worth during major life transitions.

Authored by Charles O’Dell, a real estate veteran with 23+ years of experience and 100+ property flips, who applies first-principles financial logic to senior housing audits and wealth preservation.