Introduction

Stop Being House Rich and Cash Poor. I have spent 23 years in the dirt. I have flipped over 100 properties, and if there is one thing I’ve learned, it’s that nostalgia is a terrible investment strategy. If you are over 60, you are likely sitting on a gold mine that is currently disguised as an oversized, drafty house. We call this being “House Rich and Cash Poor.” It is a mathematical tragedy. You have $500,000 or $1,000,000 in equity, yet you are worried about the price of eggs at the grocery store. That is a failure of logic.

In this guide, we are going toperform an “Equity Harvest” in order to help seniors cash out home equity. This isn’t just selling your home; it’s a strategic extraction of capital. We are moving your wealth from a stagnant, high-maintenance asset into a liquid, cash-flowing portfolio. We are going to look at the structural engineering of your home, the 2026 tax codes, and the cold, hard ROI. If you want to keep the house because of the “memories,” go look at a photo album. If you want to live a high-quality life for the next 30 years, keep reading.

Video Guide Overview

Affiliate Disclosure

I’m Charles O’Dell, and I believe in transparency. This article contains affiliate links for products and tools that I personally trust to help manage real estate assets or facilitate a move. If you click a link and make a purchase, I may earn a commission. This helps me keep providing high-level data to the 60+ community without charging you a dime for the advice.

The “Short” Answer

The Equity Harvest is the process of liquidating a primary residence to capture tax-free gains under IRC Section 121 and reinvesting that capital into higher-yielding, lower-maintenance assets. By downsizing into a modern “Mechanical, Electrical, and Plumbing” (MEP) efficient environment, seniors can eliminate thousands in annual overhead while generating a monthly “paycheck” from their previously trapped equity. However, most seniors trigger a massive tax trap in Step 3 of this process. Stop Being House Rich and Cash Poor. Here is how to avoid it…

Technical Deep Dive: The 2026 IRC Section 121 and Tax Logic

Capital Gains, Step-Up in Basis, and the 2026 Sunset

Let’s talk about the IRS. They aren’t your friends, but they do provide a very specific window for you to take your money and run. Under IRC Section 121, if you have owned and used your home as your primary residence for at least two out of the five years preceding the sale, you can exclude up to $250,000 (single) or $500,000 (married) of gain from your income. In 2026, this remains the most powerful tax shelter for the average American. However, first-principles logic requires us to look at the “Opportunity Cost of Waiting.”

Many seniors hold onto their homes until death to provide their heirs with a “Step-Up in Basis.” This means the kids inherit the house at its current market value, effectively erasing the capital gains tax. While that is great for your kids, it is terrible for your current cash flow. If your home has appreciated from $200,000 to $1.2 million, you have $1 million in gain. Even with the $500,000 exclusion, you owe taxes on the remaining $500,000. In 2026, with the Net Investment Income Tax (NIIT) of 3.8% and long-term capital gains rates hitting 20%, that is a $119,000 tax bill.

However, if you harvest now, you can take that $1.2 million, pay the tax, and move $1,081,000 into a 6% yield environment. That generates $64,860 per year in income. If you wait 10 years to give your kids the “Step-Up,” you have forfeited $648,600 in potential income. From a net-worth perspective, holding the house is a losing move. You are essentially paying over $64,000 a year for the privilege of living in a house that is probably too big for you anyway. We must also account for the 2026 inflation-adjusted brackets. If your other income is low, you might be able to harvest portions of your equity at the 0% capital gains rate by staggering the sale or utilizing installment sale strategies. This is about precision, not guesswork.

Technical Deep Dive: Structural Engineering and MEP Cycles

The Physics of Aging Assets: When the Machine Breaks Down

A house is not a static object; it is a mechanical system. As an investor who has flipped 100+ homes, I look at your house like a machine. And if your house was built in the 1970s or 80s, that machine is reaching “Critical System Failure.” We focus on MEP: Mechanical, Electrical, and Plumbing. From a structural engineering standpoint, the materials used 40 years ago have a finite lifespan. Galvanized steel pipes have an average life of 50 years before the interior diameter is so restricted by scale that water pressure drops to a trickle. Cast iron sewer lines are likely cracking as we speak.

In 2026, the cost of labor for “Subsurface Remediation” (fixing pipes under your slab) has skyrocketed. You are looking at $25,000 to $40,000 just to tunnel under a foundation. By harvesting your equity now, you are “selling” these future liabilities to a younger buyer who has the timeline to absorb the cost. Furthermore, consider the R-value of your insulation. Most older homes have R-11 or R-19 in the attic. Modern 2026 building codes often require R-49 to R-60. You are literally bleeding money through your roof every summer.

The “Structural Pivot” involves moving your capital into a smaller footprint with high-performance MEP systems. Think 18-SEER2 heat pumps, tankless water heaters with recirculating pumps, and 2×6 framing that allows for superior thermal envelopes. This isn’t just about comfort; it’s about reducing your monthly “burn rate.” If I can move you from a house that costs $1,200 a month to maintain and heat into a modern unit that costs $300, I have just handed you a $900-a-month raise before we even talk about investment returns. That is first-principles efficiency.

Technical Deep Dive: ROI and Opportunity Cost

The 10-Year Net Worth Trajectory: Liquidity vs. Dead Equity

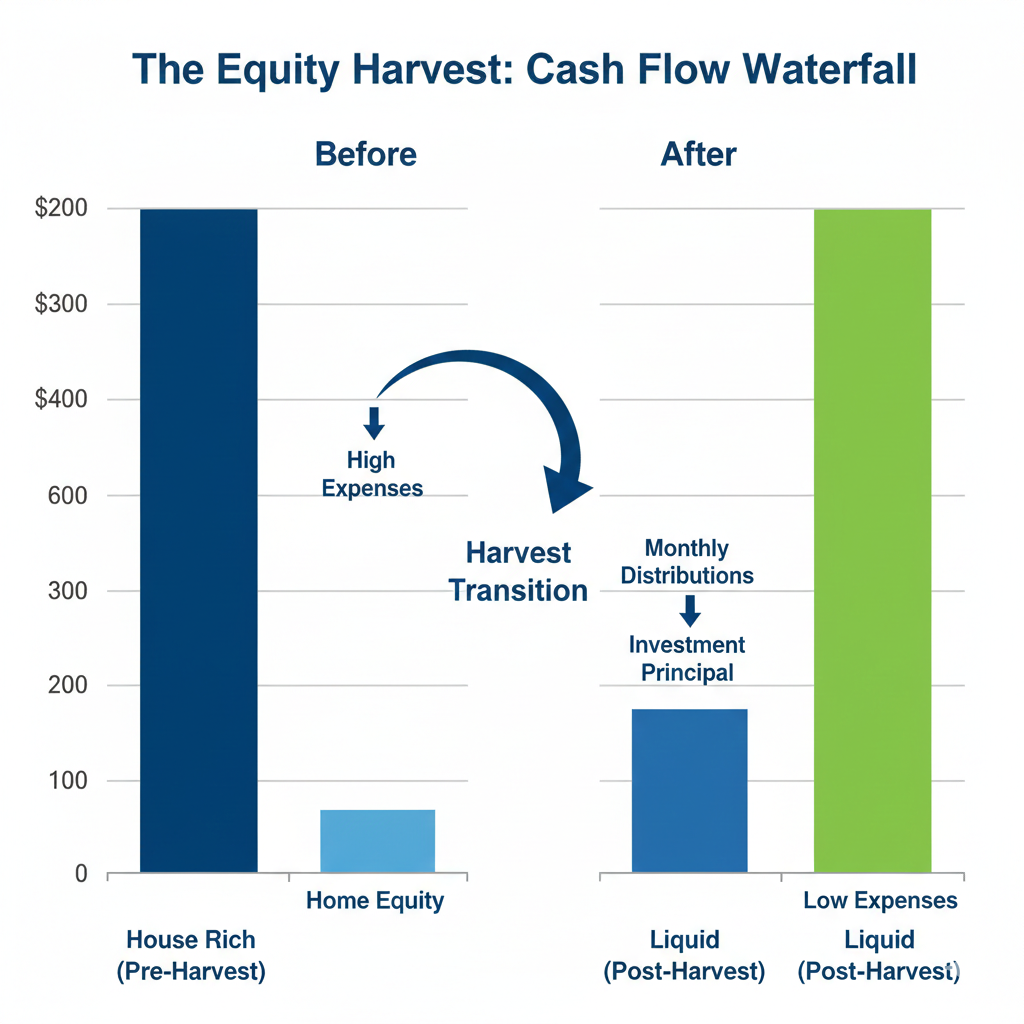

Let’s run the numbers. Imagine you have a $750,000 home with no mortgage. You feel “safe.” But is that money actually working? National real estate appreciation averages around 3-4%. In 2026, property taxes, insurance premiums, and a 1% “Maintenance Reserve” (what you should be saving for repairs) total roughly 3.5% of the home’s value annually. In real terms, your home is a “Zero-Yield Asset.” Your growth is being eaten by your holding costs.

Now, let’s harvest that $750,000. After a 6% selling cost and a 15% tax on the gain above your exclusion, you walk away with $680,000. We move that into a diversified portfolio. Even a conservative 2026 “Income Floor” strategy (Bonds, REITs, and Dividend Aristocrats) can yield 5.5% annually.

- Option A (Keep House): Net cash flow is negative $26,250 (Taxes, Insurance, Repairs).

- Option B (Harvest Equity): Net cash flow is positive $37,400 (Dividends/Interest).

The delta between staying and harvesting is $63,650 per year. Over ten years, that is a $636,500 difference in your quality of life. If you stay in the house for “emotional reasons,” you are effectively paying $5,300 a month in “Nostalgia Tax.” As a professional investor, I can tell you: no kitchen island is worth $5,000 a month. By converting the dead equity into liquid cash, you create a “Waterfall of Liquidity” that funds travel, healthcare, and legacy gifts while you are still alive to enjoy them.

2026 Cost Transparency Table

| Service / Expense | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Pre-Sale Home Inspection | $500 | $1,500 (Includes Sewer Scope) |

| Staging & Curb Appeal | $1,200 (Mulch & Cleaning) | $15,000 (Furniture Rental) |

| Real Estate Commissions (2026) | 2.5% (Flat Fee/Limited) | 6% (Full Service Concierge) |

| Closing Costs & Title Insurance | 1% of Sale Price | 2% of Sale Price |

| Downsized Unit Move-In | $2,000 | $10,000 (White Glove) |

Technical Deep Dive: Zoning, ADUs, and Regulatory Hurdles

The Backyard Harvest: Leveraging SB-9 and Local Zoning

Sometimes, the Equity Harvest doesn’t mean moving to a condo in Florida. In 2026, many states (like California, Oregon, and Washington) have enacted laws that allow you to “harvest” your backyard. By building an Accessory Dwelling Unit (ADU) or splitting your lot, you can monetize the land without giving up the neighborhood you love. But this is a technical minefield. You must understand “Setback Requirements”—the distance a structure must be from the property line. In most jurisdictions, a detached ADU requires a 4-foot rear and side yard setback.

From a first-principles perspective, building an ADU is a “Yield Play.” If it costs you $250,000 to build a 600-square-foot cottage and you can rent it for $2,500 a month, your “Unlevered Yield” is 12%. That blows away the stock market and the appreciation of the main house. However, you must account for “Utility Capacity.” Many older homes have a 100-amp electrical service. To add a second dwelling, you’ll likely need to upgrade to a 200-amp or 400-amp service. In 2026, the cost of a panel upgrade and new service drop from the utility company can range from $5,000 to $12,000. If you don’t calculate this “Load Requirement” early, your project will stall at the permit office.

The smartest move I see seniors making? Move into the high-tech, small ADU yourself and rent out the big, drafty main house. You keep your primary residence tax status on the entire property, but you’ve effectively turned your backyard into a $30,000-a-year pension plan. You’ve harvested the equity while keeping the dirt. That is how a pro thinks.

Affiliate Products Table

| Product | Function | Strategic Value |

|---|---|---|

| Phyn Plus Smart Water Monitor | Leak Detection | Prevents equity-destroying water damage in aging pipes. |

| Ecobee Premium Thermostat | HVAC Management | Optimizes MEP efficiency to lower monthly burn rates. |

| August Wi-Fi Smart Lock | Keyless Entry | Essential for managing “Lock and Leave” properties or ADU rentals. |

Actionable Checklist: Executing the Harvest

- Perform a “Technical Home Audit”: Hire a licensed inspector to identify the remaining useful life of your roof, HVAC, and sewer. If the total repair liability exceeds 5% of the home’s value, you are in a “Sell Now” situation.

- Calculate your “Net Proceeds” (2026 Logic): Take your estimated sale price, subtract 6% for commissions/closing, and then subtract your cost basis plus the $250k/$500k exclusion. If the remaining taxable gain is large, call a CPA immediately to discuss a 1031 exchange or an installment sale.

- Interview three “Senior Real Estate Specialists” (SRES): You don’t want a “neighborhood expert” who just puts a sign in the yard. You want someone who understands 2026 tax law and the logistics of a senior transition.

- Define your “Target Envelope”: Decide where you are moving. Logic dictates a smaller, MEP-efficient unit with “Universal Design” features (no stairs, 36″ doorways). If the new place requires a remodel, calculate that cost before you sell.

- Execute the “Purge”: Apply the 80/20 rule. You likely use 20% of your belongings 80% of the time. Get rid of the other 80%. Every pound of “stuff” you move is a drag on your harvested capital.

- Establish your “Income Engine”: Work with a flat-fee financial advisor to move your harvested equity into a diversified income-generating portfolio. Ensure the monthly distributions are automated.

Internal Resources

- The ADU Revolution: Why your backyard is your best retirement plan. (Coming Soon)

- Universal Design 101: How to renovate for your 80-year-old self today. (Coming Soon)

- 2026 Tax Strategies for Seniors: Navigating the sunset of the TCJA provisions. (Coming Soon)

Summary

Stop Being House Rich and Cash Poor. The Equity Harvest is not about losing a home; it is about gaining a life. For 23 years, I have watched people cling to “dead equity” like a life raft, only to realize the raft is made of lead. If you are over 60, your primary objective should be liquidity and efficiency. By analyzing your home through the lens of structural engineering and first-principles finance, you can see it for what it truly is: a tool. When the tool becomes too heavy or too expensive to maintain, you trade it in for a better one. Take the $500,000, take the $60,000 a year in income, and let someone else worry about the leaking roof. That is the Charles O’Dell way.

Bio: Charles O’Dell

Charles O’Dell is the expert voice behind HousingAfter60.com. With 23+ years in real estate, 100+ successful flips, and hundreds of facilitated transactions, Charles specializes in helping homeowners over 60 optimize their portfolios. He uses a direct, logic-based approach to strip away the emotional baggage of homeownership and focus on the bottom line. When he isn’t analyzing cap rates or structural load specs, he is helping seniors transition into high-performance, low-maintenance living environments.

Written by Charles O’Dell: 23+ years in RE, 100+ flips, and hundreds of senior housing transitions.