Summary: In 2026, rising assessments are cannibalizing senior equity. This guide uses first-principles logic to break down “Circuit Breakers,” Homestead Exemptions, and the structural risks of high-tax jurisdictions. We provide the 2026 Cost Transparency Table to help you decide between fighting taxes or selling for a profit.

Note: Local labor rates for property tax consulting and appraisals changed in Jan 2026. See our full regional cost table below.

Introduction: Your Home is a Business, Not a Memory

If you are over 60, it is time to stop looking at your home through the lens of nostalgia. Tax relief is an important factor for every senior. After 23 years in this game: flipping over 100 properties and closing hundreds of deals: I can tell you that the most dangerous thing a senior can do is fall in love with a piece of real estate. In 2026: your home is a line item on a balance sheet. If the overhead: consisting of property taxes, maintenance, and insurance: exceeds the utility you derive from it: you are holding a failing asset.

Property taxes are the most aggressive form of equity erosion. Unlike a mortgage, they never end. In fact: they grow. In 2026: many states have aggressively reassessed values to cover municipal budget gaps. If you sit back and do nothing: you are voluntarily donating your retirement savings to the local government. This article provides the technical blueprint to stop the bleeding using “Circuit Breakers,” exemptions, and relocation logic. We are going to look at the numbers: because the numbers are the only thing that won’t lie to you.

Video Guide Overview

Affiliate Disclosure

Transparency is my policy. Some links in this article are affiliate links. If you purchase through them: I may earn a commission. I only recommend technical tools that I would use on my own investment properties to track value or manage tax appeals.

The “Short” Answer

To reduce property taxes in 2026, you must apply for a Homestead Exemption or a “Circuit Breaker” program that caps taxes as a percentage of your income. Eligibility generally requires you to be 61 to 65 years old with a total household income between $40,000 and $84,000: depending on your state. Failure to file by the Q1 2026 deadline means you forfeit these savings entirely for the fiscal year.

2026 Property Tax Transparency Table

| Service/Expense Type | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Tax Appeal Filing Fee | $0 – $50 (County Dependent) | $500 (Legal Representation) |

| Certified Appraisal Report | $475 (Standard Form) | $1,200 (Narrative/Expert) |

| Tax Consultant Commission | 0% (Self-Managed) | 35% of Total Tax Savings |

| Estate Title Transfer | $150 (Quitclaim Deed) | $2,500 (Asset Protection Trust) |

Affiliate Product Comparison Table (2026 Tech)

| Product | Utility | 2026 Price Est. |

|---|---|---|

| PropertyTaxHero Software | Analyzes local comps to find appeal evidence. | $129/appeal |

| Bosch Laser Measurer | Verifies square footage for assessor errors. | $89 |

| Trust & Will Estate Suite | Simplified deed transfers for senior exemptions. | $599 |

Section 1: The First-Principles of Tax Assessment

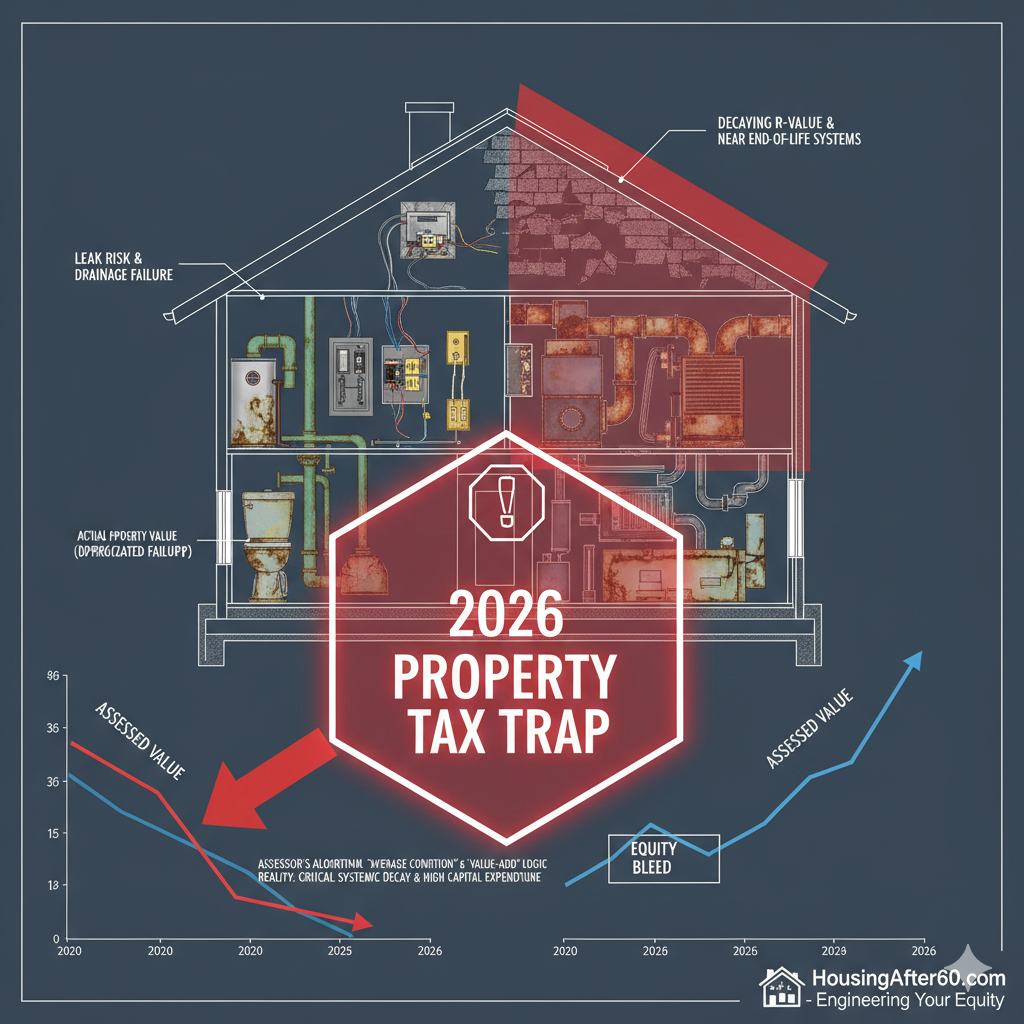

Why are your taxes going up while your income stays the same? It is a failure of logic. Most people think their tax bill is based on what they could sell the house for today. That is incorrect. In 2026: your bill is based on an “Assessed Value” which is a mass-appraisal calculation performed by an algorithm. These algorithms are notoriously bad at accounting for “Functional Obsolescence.”

Technical Deep Dive: Structural Engineering & The Tax Trap

From a structural engineering perspective: a home is a collection of systems with finite lifespans. In 2026: we categorize these as the MEP (Mechanical, Electrical, Plumbing) cycles. A standard asphalt shingle roof has a 20 to 25-year cycle. A copper plumbing system has a 50-year cycle. An HVAC system has a 15-year cycle.

The “Tax Trap” occurs when the assessor’s algorithm assumes your 30-year-old home is in “Average Condition.” If you have not performed a systems refresh: the house is actually in “Fair” or “Poor” condition from an engineering standpoint. The R-value of your insulation has likely degraded by 20% since 1990: increasing your utility overhead. If you spend $50,000 to modernize these systems: the assessor will likely trigger a “Value-Add” event: raising your taxes further. The logic is brutal: stay in a decaying house and lose money on utilities: or fix the house and lose money on taxes. To win: you must prove to the assessor that your home’s “Effective Age” is much higher than its “Actual Age” due to system degradation: thereby lowering the taxable base without actually letting the house fall down.

Section 2: The Circuit Breaker Mechanism

The “Circuit Breaker” is the most powerful tool for any homeowner over 60. Just like an electrical circuit breaker stops a surge from burning down your house: these tax programs stop a “tax surge” from burning through your savings. In 2026: 18 states have robust circuit breaker laws.

Technical Deep Dive: Tax/Legal Logic & IRC Section 121

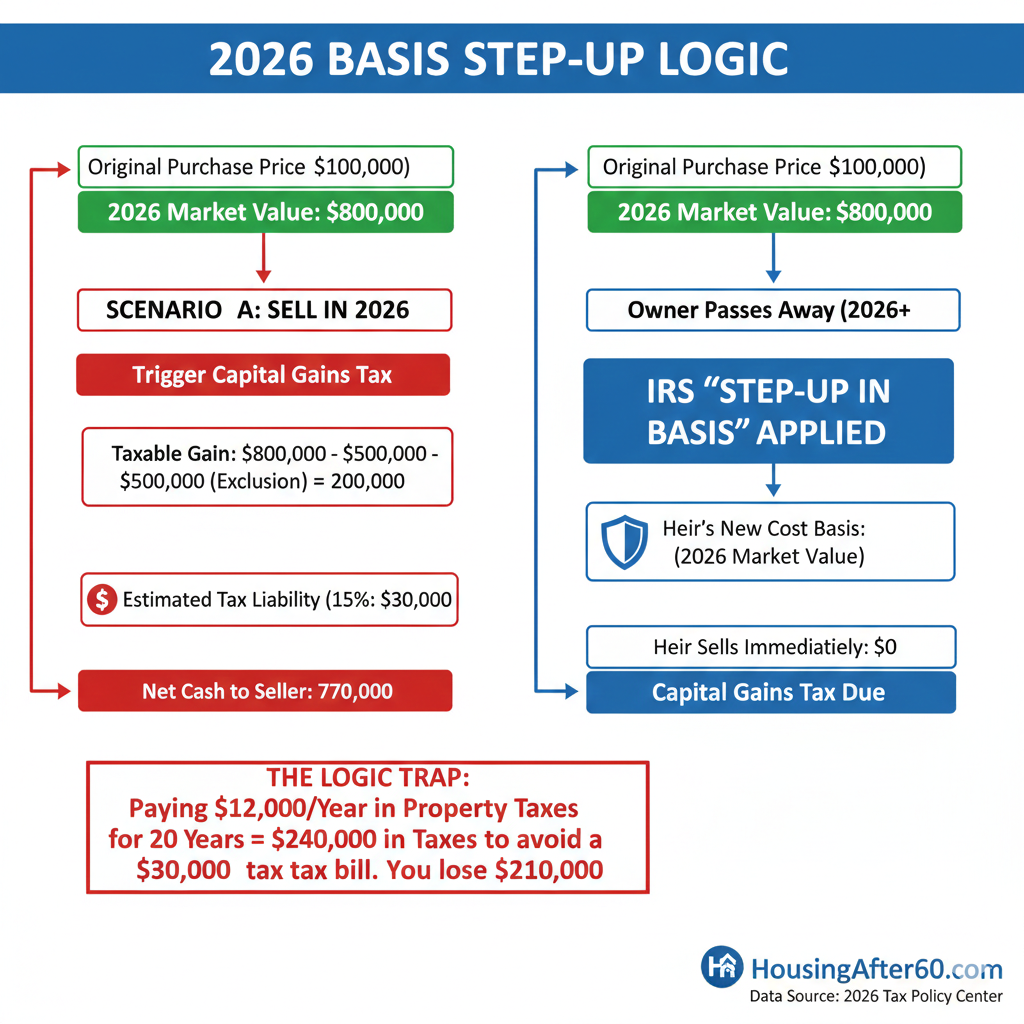

Let’s look at the legal logic of staying vs. leaving. Many seniors are trapped by the fear of capital gains tax. Under IRC Section 121: you have a $250,000 (single) or $500,000 (married) exclusion on the gain of your primary residence. In 2026: we are seeing “Equity Bloat.” If you bought a home for $50,000 in 1985 and it is now worth $750,000: you have a $700,000 gain. As a married couple: you still owe tax on $200,000 of that gain.

However: the 2026 “Step-Up in Basis” rule provides a massive incentive to hold until death. When you pass away: your heirs receive the property at its 2026 market value: effectively wiping out the $700,000 gain. But here is the logic catch: if you pay $12,000 a year in property taxes for the next 20 years: you have spent $240,000 to “protect” an inheritance. If the capital gains tax on the $200,000 excess gain would have only been $30,000 (15% rate): you have effectively spent $210,000 more than necessary. Holding a high-tax asset for the “Step-Up” is often a mathematical error for the middle class. You must calculate the crossover point where the cumulative tax paid exceeds the capital gains liability of an immediate sale.

Section 3: State-By-State Exemption Arbitrage

In 2026: where you live is a tax strategy. States like Florida and Texas are popular for having no state income tax: but they compensate with high property taxes. Conversely: states like South Carolina offer the “Homestead Exemption Program” for those 65+ that exempts the first $50,000 of fair market value from all property taxes. In a low-cost county: this can reduce your bill to nearly zero.

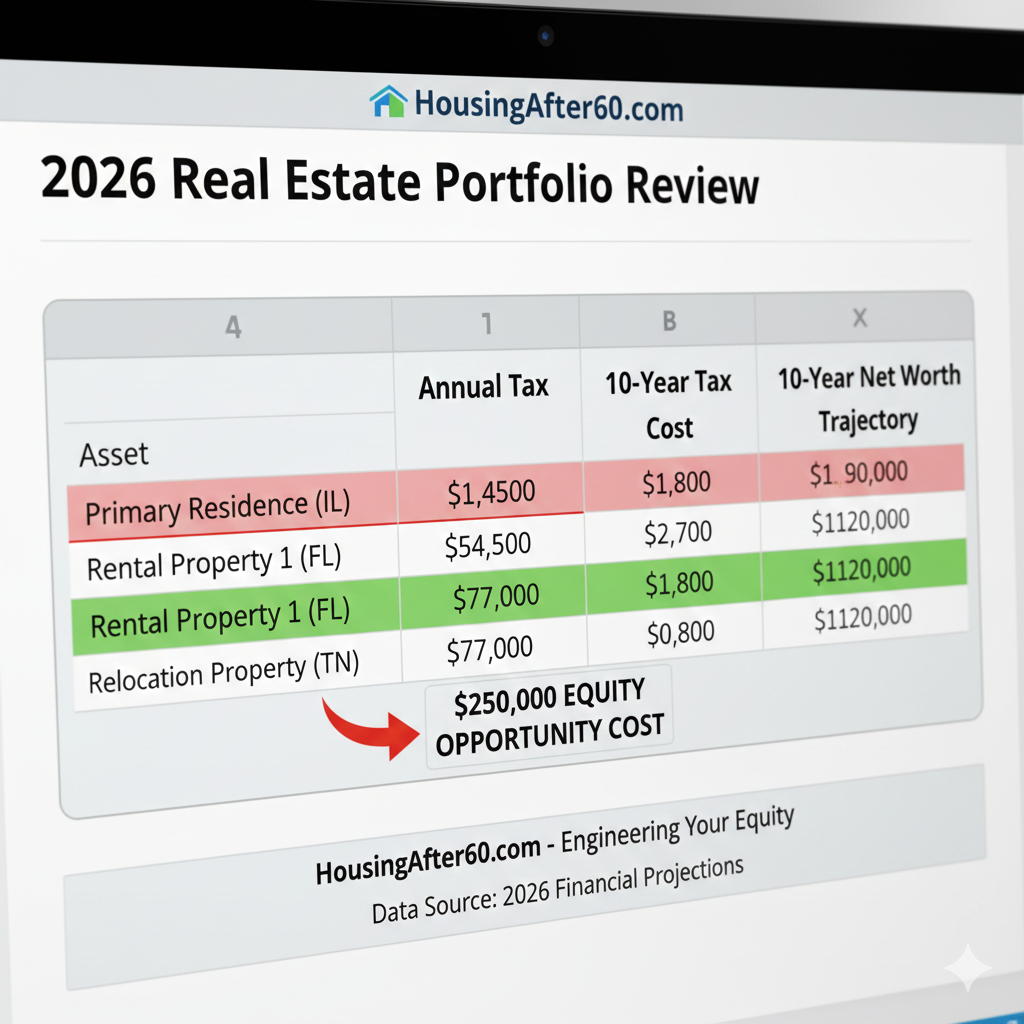

Technical Deep Dive: ROI Calculations & 10-Year Trajectories

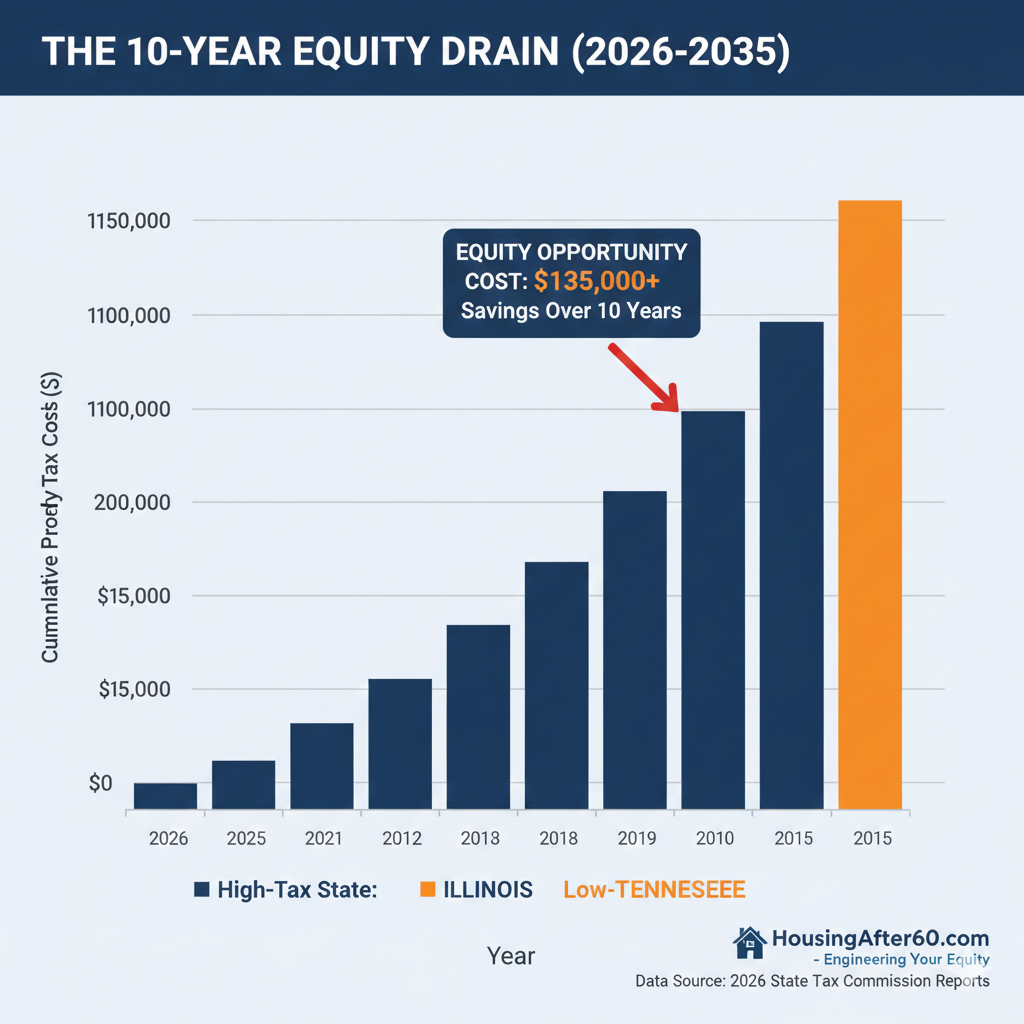

Consider the “Opportunity Cost” of a high-tax jurisdiction. If you live in a $500,000 home in New Jersey: you are likely paying $15,000 a year in taxes. If you relocate to a “Tax Haven” county in Tennessee: you might pay $1,500 for a similar home.

Scenario Analysis: Scenario A (NJ): $15,000/year x 10 years = $150,000 out of pocket. Scenario B (TN): $1,500/year x 10 years = $15,000 out of pocket. The $13,500 annual difference: if invested in a conservative 2026 Treasury Bond yielding 4.5%: grows to approximately $172,000 over a decade. In Scenario B: you haven’t just saved money; you’ve created a $172,000 “Tax Hedge” fund. When you factor in the lower cost of living and the potential to buy a single-story home (reducing future MEP maintenance costs): the ROI on relocation is often 300% higher than staying and fighting a losing tax battle. Logic dictates that you move the moment your property tax bill exceeds 5% of your gross annual income.

Section 4: The Internal Audit Protocol

Before you apply for relief: you must conduct an internal audit of your property’s data. Assessors often make “Dimensional Errors.” I once saw a property taxed for 3,000 square feet that only measured 2,400. They were counting an unheated garage as living space. In 2026: these errors are common because counties use aerial drone flyovers to estimate size without verifying interior utility.

Technical Deep Dive: Zoning & Regulatory Hurdles

Another area of relief is “Zoning De-valuation.” If your property was recently rezoned for high-density residential or commercial use: your taxes likely spiked. However: as a senior: you may be able to apply for a “Special Use Valuation.” This legally forces the assessor to value your land based on its *current* use (a single-family home) rather than its *highest and best* use (an apartment complex). This is a technical nuance that most homeowners miss. You must file a zoning variance or an “Agricultural Forest Land” deferral if you have more than a few acres. In 2026: these deferrals can reduce the land portion of your tax bill by up to 90%. If you aren’t looking at the zoning map: you are paying for potential you aren’t using.

Actionable Checklist: The 2026 Tax Relief Step-by-Step

- **Audit the Property Record Card:** Visit your county assessor’s website and download the “Property Record Card.” Verify the bedroom count, bathroom count, and square footage. Any error in their favor is an immediate ground for appeal.

- **Check the “Age 61” Threshold:** Many people wait until 65. In states like Washington: the “Senior Citizen and People with Disabilities” exemption starts at age 61. Check your local statutes for early-entry dates.

- **Gather Your Income Data:** Calculate your “Combined Disposable Income.” This includes Social Security, pensions, and interest. If your income is under $84,000 (in high-cost states): you likely qualify for a partial freeze.

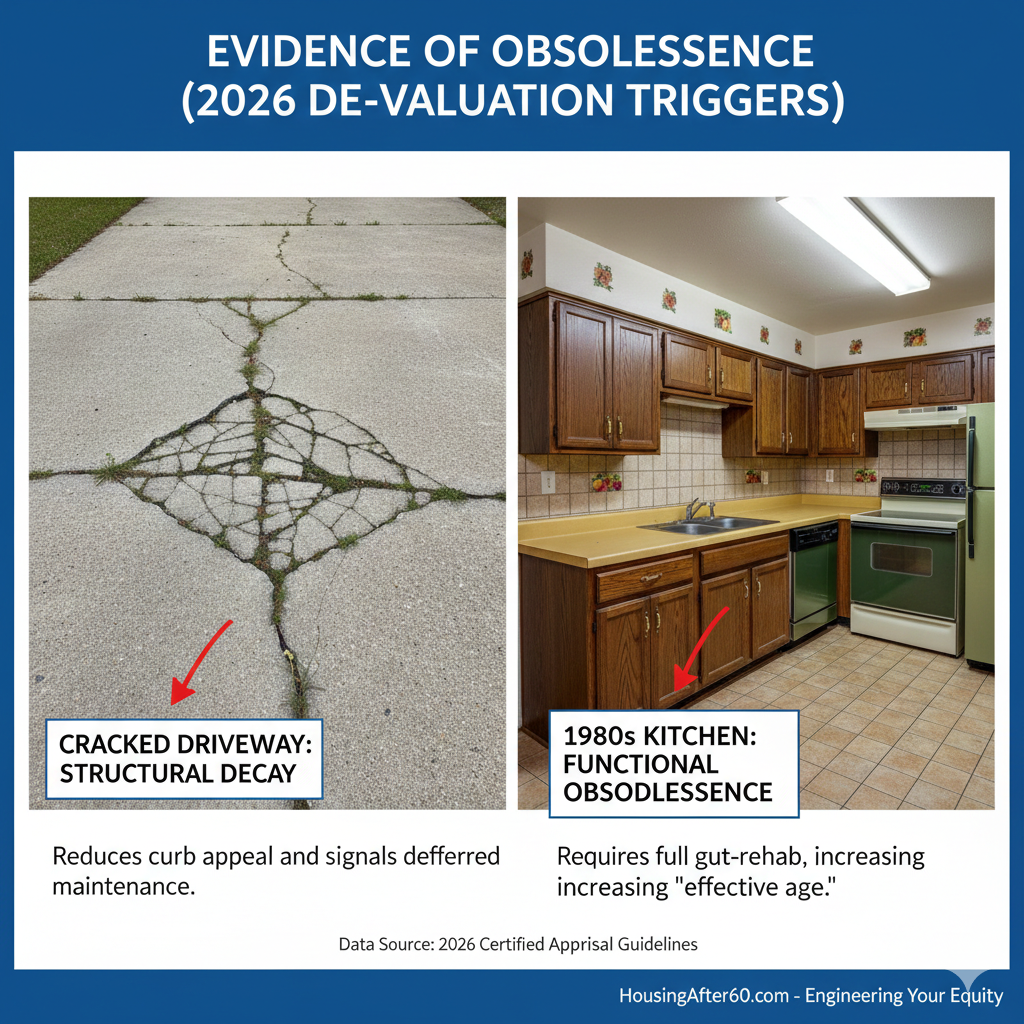

- **Document Functional Obsolescence:** Take high-resolution photos of any structural issues: dated finishes: or non-working systems. A 20-year-old roof is “Near End of Life” and reduces the market value of the structure.

- **File the “Homestead Declaration”:** If you haven’t filed this: you are paying “Non-Owner Occupied” rates: which are significantly higher. This is the simplest fix in the book.

- **Submit the “Circuit Breaker” Form:** This is usually a separate state form from the county exemption. You must provide a copy of your 2025 tax return to prove your income-to-tax ratio.

- **Hire a Consultant for the Final Mile:** If your property is valued over $1 million: do not DIY the appeal. Professional consultants have access to the “Co-Star” and “MLS” databases that you don’t. Their 30% fee is worth the 70% of the savings you keep.

Internal Resources

To further optimize your 2026 real estate strategy: read our deep dive on 2026 Downsizing Costs: Professional Movers vs. DIY. You should also review HVAC ROI: 2026 Energy Credits for Seniors and our critical analysis of 2026 Reverse Mortgage Warnings: Don’t Lose Your Equity. (All coming soon)

Summary: Control the Controllables

You cannot control the economy: and you cannot control the local government’s spending habits. You *can* control your property’s taxable base. By 2026: the “Circuit Breaker” and “Homestead” exemptions are not suggestions; they are financial necessities. Use the first-principles logic we’ve discussed: audit your property record: calculate your 10-year ROI: and stop being a victim of “Equity Bleed.” If the numbers don’t add up: sell the asset and move to a jurisdiction that respects your retirement. Your home should serve you: not the other way around.

Bio: Charles O’Dell

Charles O’Dell is the Lead Technical Strategist at HousingAfter60.com. With 23+ years in real estate and 100+ successful flips: Charles focuses on the intersection of structural engineering and financial logic. He helps seniors navigate the transition from “Homeowners” to “Asset Managers”: ensuring that their primary residence remains a source of wealth rather than a liability.

Charles O’Dell has 23+ years of experience and 100+ flips, specializing in senior real estate logic.