Introduction

Summary: Solo aging in 2026 creates a massive “Loneliness Tax” through duplicated utility costs, higher property taxes, and outsourced care services. By moving to intentional communities, seniors save an average of $2,100 monthly. This guide breaks down the cold, hard math of isolation versus community.

Note: Local labor rates for home modifications and caregiving changed in Jan 2026. See our full regional cost table below.

Video Guide Overview

The Brutal Math of Moving Solo

I have spent 23 years watching people make emotional real estate decisions. Most of them are wrong. We have a romanticized view of “aging in place,” but the numbers tell a different story. In 2026, if you are living in a 2,500 square foot house by yourself, you are paying a premium for space you do not use and isolation that is killing your bank account. I call this the Loneliness Tax. It is the invisible surcharge on your life for not having a roommate or a community to split the bills with.

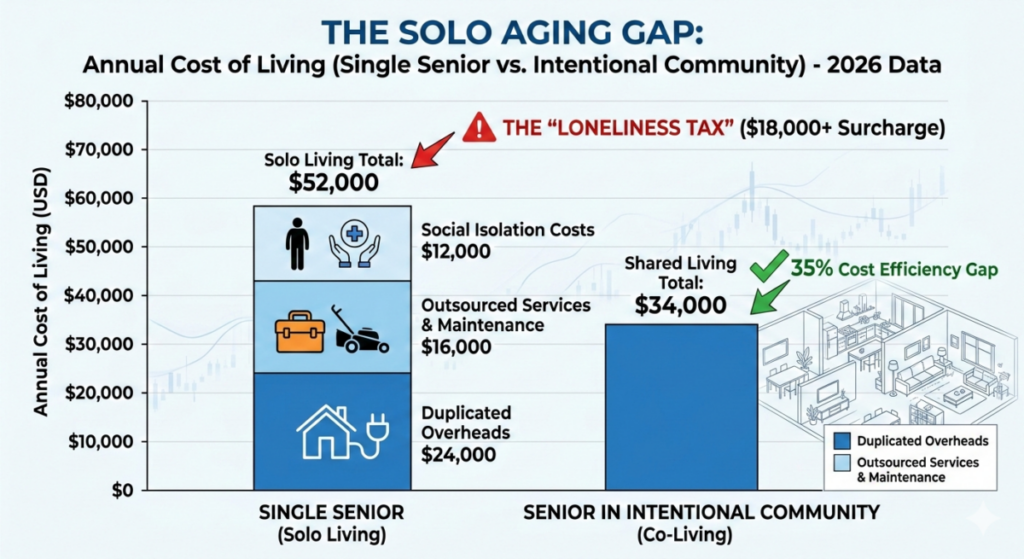

What is the “Loneliness Tax”? When you live alone, you pay 100% of the property taxes. You pay 100% of the roof repair. You pay 100% of the lawn guy. If you had one other person in that house, your cost of living would drop by nearly 40% overnight. In my experience flipping over 100 properties, the most expensive homes are the ones where a single person is trying to fight the laws of economics. It is not just about money; it is about the efficiency of your capital. Your home should be an asset, not a drain on your 401k.

Technical Deep Dive: Structural Engineering and MEP Cycles

Maintaining a solo residence requires understanding the Mechanical, Electrical, and Plumbing (MEP) life cycles. In a standard suburban home, a 15-year-old HVAC system reaches its “end of life” efficiency. For a solo senior, the cost per square foot to replace this system is significantly higher because the load-bearing requirements remain the same regardless of occupancy. If you are heating a four-bedroom house for one person, your R-value efficiency is effectively halved relative to the utility.

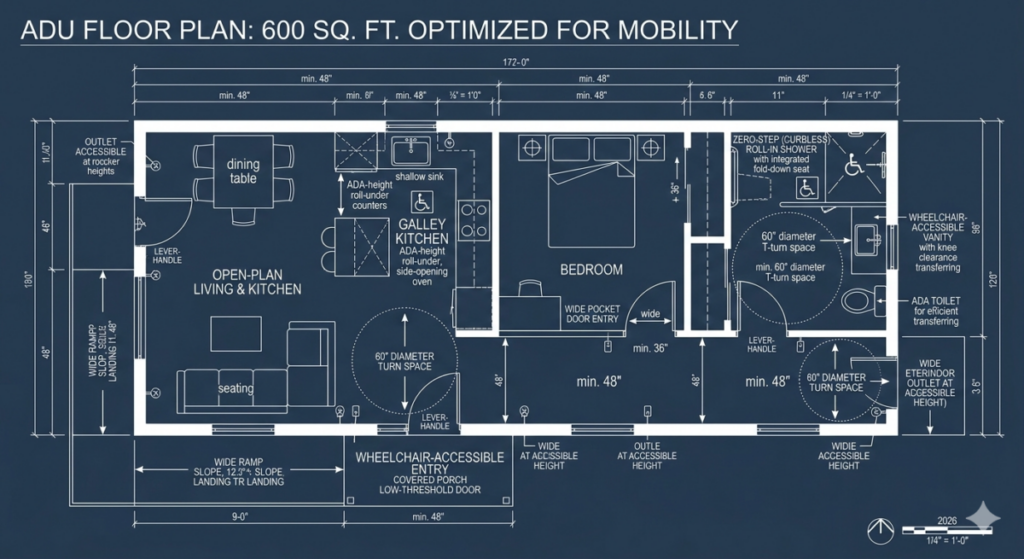

From a structural standpoint, aging in place often requires retrofitting. Installing a residential elevator or a curbless shower involves altering load-bearing joists. In 2026, the cost of structural steel and treated lumber has spiked. A solo homeowner bears 100% of this capital expenditure. In an intentional community or co-housing model, these “sunk costs” are distributed across multiple residents. The “Unit Cost of Comfort” is the metric you should track: total monthly MEP costs divided by active hours spent in each room. For solo dwellers, this number is usually 300% higher than in shared living environments.

Affiliate Disclosure

I believe in transparency. Some links in this article are affiliate links. If you click them, I might earn a commission at no extra cost to you. I only recommend tools that I would use on my own job sites.

The Short Answer

The “Loneliness Tax” is the $18,000 to $30,000 annual premium paid by seniors living alone in traditional single-family homes. Transitioning to intentional communities or shared equity models eliminates duplicated overhead and reduces per-capita maintenance costs by approximately 33%.

Tax Logic and the IRS Section 121 Trap

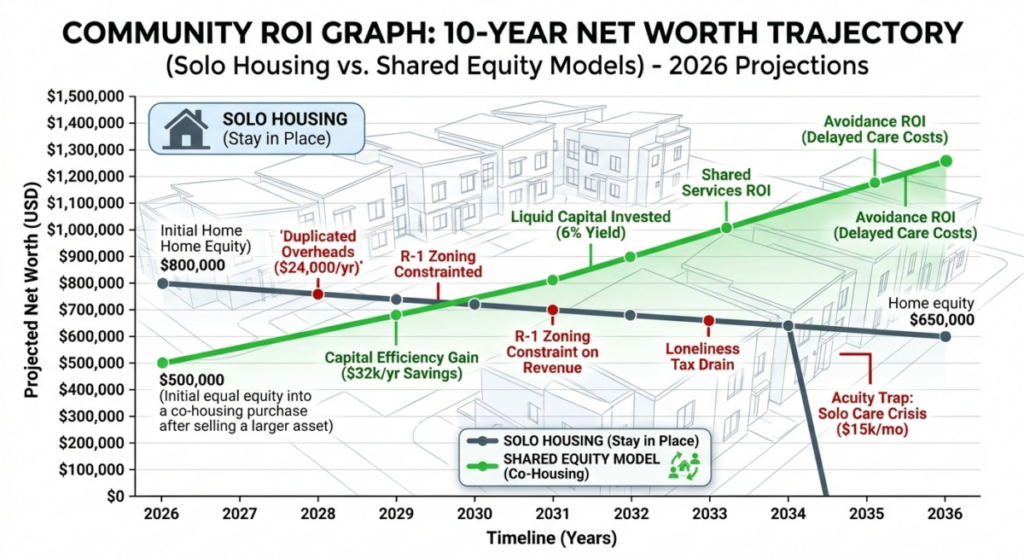

Many seniors stay in their large homes because they fear the tax man. They think the $250,000 (single) or $500,000 (married) capital gains exclusion is a reason to hold. But they forget the “Opportunity Cost of Capital.” If your home has $800,000 in equity and you are living alone, that money is “dead.” It is not earning interest. It is sitting in the walls while you pay for a new roof.

Technical Deep Dive: 2026 Step-Up in Basis and IRC Section 121

Under the current 2026 tax code, the strategy for real estate has shifted. While the IRC Section 121 exclusion remains a pillar, the “Step-Up in Basis” rules are the real prize. However, holding a depreciating physical asset just for a basis step-up at death is often a losing bet for the living. If you sell now and move into a shared living environment, you can deploy that capital into 5% or 6% yield instruments.

Consider the “Net Worth Trajectory.” A solo senior in a $600k home pays $12k in taxes and $8k in maintenance annually. Over 10 years, that is $200k in outflow. If that same senior sells, moves to a $300k co-housing unit, and invests the $300k difference, the 10-year swing in net worth is nearly $450,000 when accounting for compounded returns and avoided expenses. We focus on the bottom line: staying in the big house is a slow-motion bank robbery where you are the victim and the house is the thief.

2026 Cost Transparency Table: Solo vs. Community

| Expense Category | Solo (DIY/Basic) | Community (Pro/Shared) |

|---|---|---|

| Monthly Utilities | $450 – $600 | $150 – $225 |

| Maintenance/Lawn | $250 – $400 | Included in HOA/Dues |

| Property Taxes | $600 – $1,200 | $200 – $450 (Split) |

| Social/Health Care | $1,500+ (Outsourced) | $0 (Organic/Shared) |

Affiliate Product Comparison Table

| Product | Purpose | 2026 Price |

|---|---|---|

| Sense Home Energy Monitor | Track real-time wasted KWh in large homes. | $299 |

| Ring Alarm Glass Break Pro | Security for solo dwellers in vulnerable areas. | $189 |

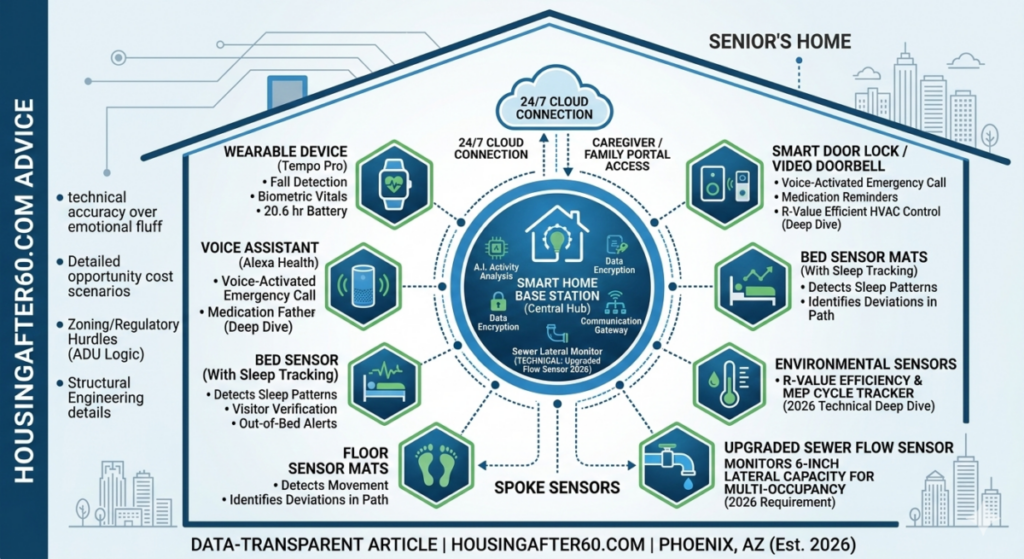

| CarePredict Tempo Wearable | AI-driven fall detection for isolated living. | $449 |

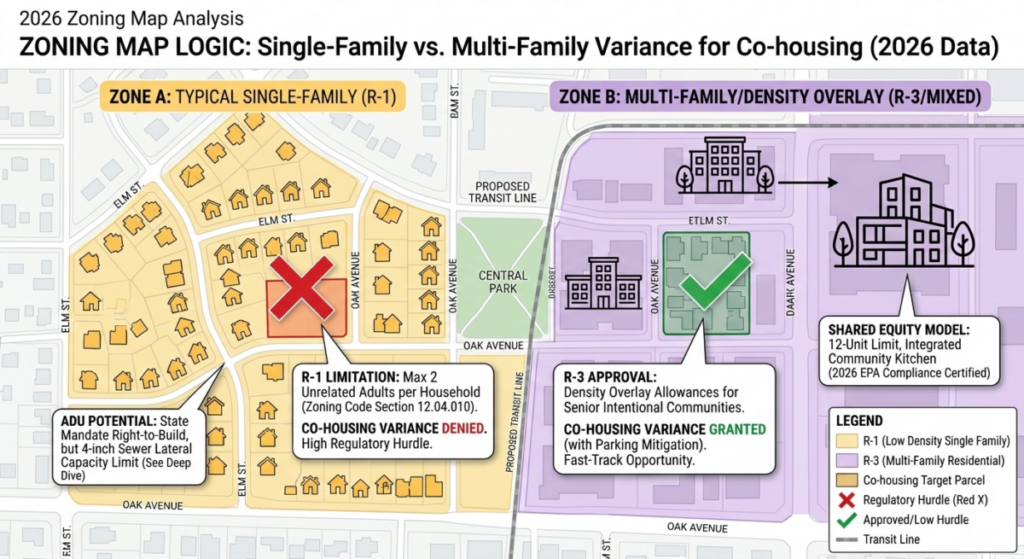

Zoning Hurdles: The “Hidden” Costs of Community

If you decide to build an intentional community, the government is usually your biggest enemy. Zoning laws are designed for the 1950s nuclear family, not the 2026 reality of aging. You will encounter “Single-Family Residential” (R-1) codes that forbid more than two unrelated people from living together. This is a regulatory tax on your freedom to save money.

Technical Deep Dive: Zoning Variance and ADU Logic

To bypass these hurdles, we look at Accessory Dwelling Units (ADUs). In 2026, many states have passed “Right to Build” laws for ADUs. The engineering challenge is the sewer lateral capacity. When you add a second kitchen to a property, you often exceed the flow rate of a standard 4-inch PVC sewer line. Upgrading to a 6-inch line can cost between $8,000 and $15,000 depending on the depth of the city main.

Furthermore, you must calculate the “Impervious Surface Ratio.” If your community adds too much concrete for parking, you trigger stormwater management fees. I have seen projects stalled for months because the owners didn’t account for the 2026 EPA runoff requirements. If you are planning a shared living space, your first call shouldn’t be to a decorator; it should be to a civil engineer. You need to know if the soil can handle the additional load of an expanded footprint. If you ignore the dirt, the dirt will eat your retirement fund.

The “Roommate” ROI: 10-Year Projections

Loneliness tax. Let’s talk about the ROI of social connection. This sounds soft, but the numbers are hard. Isolation leads to cognitive decline. Cognitive decline leads to the $15,000-a-month memory care facility. By living with others, you stay sharp. You stay active. You delay the most expensive phase of your life. This is the ultimate “Avoidance ROI.” If you can stay out of a nursing home for an extra three years because you lived in a vibrant community, you just saved $540,000.

I recently helped a client in Arizona who was “house-poor” in a $900k custom home. She was lonely and her roof was leaking. We sold the house, bought a large duplex with a friend, and split the costs. She walked away with $400k in cash. Her monthly “burn rate” dropped from $6,000 to $2,200. That is not just a lifestyle change; that is a financial fortress. She stopped paying the Loneliness Tax and started collecting interest.

Technical Deep Dive: ROI Calculations and Opportunity Cost

When calculating the 10-year ROI of shared living, you must use a “Discounted Cash Flow” (DCF) model. You take the monthly savings ($3,800 in the case above) and project it forward with a 6% annual return. Over 120 months, that $3,800 monthly contribution grows to over $600,000.

Compare this to the “Equity Growth” of the solo home. In a 3% appreciation market, the house grows, but the carrying costs (insurance, taxes, repairs) eat 2.5% of that growth. Your real return on a solo primary residence is often less than 0.5% after inflation. Shared living allows you to move capital from a “Low-Yield Shelter Asset” to a “High-Yield Liquid Asset.” In 2026, liquidity is king. You cannot eat your kitchen cabinets, and you cannot pay a surgeon with a piece of your siding. You need cash flow.

Step-by-Step Checklist for Reducing Your Housing Costs

If you are ready to stop paying the Loneliness Tax, follow these steps exactly. Do not skip the boring parts. The boring parts are where the money is saved.

- Audit Your Square Footage: Spend one week placing a blue piece of tape on every door you open. At the end of the week, if 60% of your rooms don’t have tape, you are over-housed.

- Calculate Your Cost Per Room: Divide your total monthly housing cost (mortgage, tax, insurance, utilities) by the number of rooms you actually use. If it is over $1,000 per room, you are failing the efficiency test.

- Research Local ADU Laws: Check your city’s 2026 zoning map. Look for “Secondary Suite” or “ADU” allowances. This determines if you can build or buy a shared property.

- Get a Sewer Scope: Before buying a shared property, pay $300 for a camera to check the main line. Shared living means more flushing. A collapsed line will cost you $20,000.

- Draft a Co-Living Agreement: Never move in with a friend based on a handshake. Use a legal contract that covers “Exit Logic.” What happens if one person wants to sell? Write it down now or pay a lawyer later.

- Analyze the Tax Basis: Consult a CPA about your “Cost Basis” before you sell. Use the 2026 limits to ensure you aren’t leaving money on the table.

- Interview Potential Partners: Social compatibility is a financial risk. If your roommate is a slob, your property value drops. Screen them like you would a tenant in a 100-unit apartment complex.

Internal Resources

For more data-driven real estate strategies, check out our other guides:

- 2026 ADU Construction Costs: A Blueprint for ROI

- The Shared Equity Contract: Protecting Your Capital in Co-Housing

- Retirement Exit Strategies: Selling the Family Home Without Regret

- Stop Being House Rich And Cash Poor

- ALL COMING SOON

Summary

The Loneliness Tax is real, it is expensive, and it is avoidable. In 2026, the world is too expensive for you to live like a hermit in a palace. Efficiency is the new luxury. By combining resources, splitting technical maintenance costs, and leveraging shared equity, you can increase your net worth while improving your quality of life. Don’t let nostalgia keep you broke. Look at the numbers, make the move, and keep your money where it belongs: in your pocket.

About the Author: Charles O’Dell

Charles O’Dell is the owner of HousingAfter60.com and a veteran real estate investor with 23+ years of experience. He has flipped over 100 properties and facilitated hundreds of transactions for homeowners and investors. Charles specializes in first-principles logic to help the 60+ demographic maximize their home equity and minimize their cost of living. He doesn’t care about your “dream home”; he cares about your balance sheet.

Written by Charles O’Dell, 23-year real estate veteran with 100+ flips and 500+ senior transitions.