Summary: Downsizing Costs. Downsizing in 2026 requires a 24-month tactical window to maximize your net worth. Failure to account for capital gains shifts and rising labor costs for “clutter remediation” can cost you $50,000 in lost equity. Note: Local labor rates for professional junk removal and estate staging changed in Jan 2026. See our full regional cost table below.

Affiliate Disclosure: This post contains links to tools we use for asset liquidation. We may earn a commission if you purchase through these links at no extra cost to you.

The Short Answer: Moving after 60 is a math problem, not an emotional one. To succeed, you must treat your home as a depreciating asset and liquidate systematically over 24 months to avoid the “panic-sale” discount.

Video Guide Overview

Introduction: Nostalgia is Your Biggest Expense

I have flipped over 100 houses. I have seen grown men cry over a dusty workbench and women refuse to sell because of a height-marker on a door frame. I am here to tell you that those memories are free, but the square footage housing them is costing you $400 a month in taxes and maintenance. In 2026, the real estate market does not care about your sentiment. It cares about updated MEP (Mechanical, Electrical, Plumbing) systems and clean floor plans. If you are over 60, your “forever home” is likely becoming a “forever liability.”

The “Last Move” isn’t just about finding a smaller bedroom: it is about a ruthless extraction of equity. Most people wait until a hip fractures or a spouse passes to move. That is a strategic failure. By then, you are a motivated seller, and motivated sellers get slaughtered in negotiations. We are going to build a 24-month master plan that treats your move like a corporate merger. We are liquidating the “Old You, Inc.” to fund a high-liquidity, low-maintenance retirement. We will look at the hard costs of labor, the tax traps of 2026, and the structural realities of older homes that most “friendly” realtors won’t tell you about.

Technical Deep Dive: Structural Engineering and MEP Life Cycles

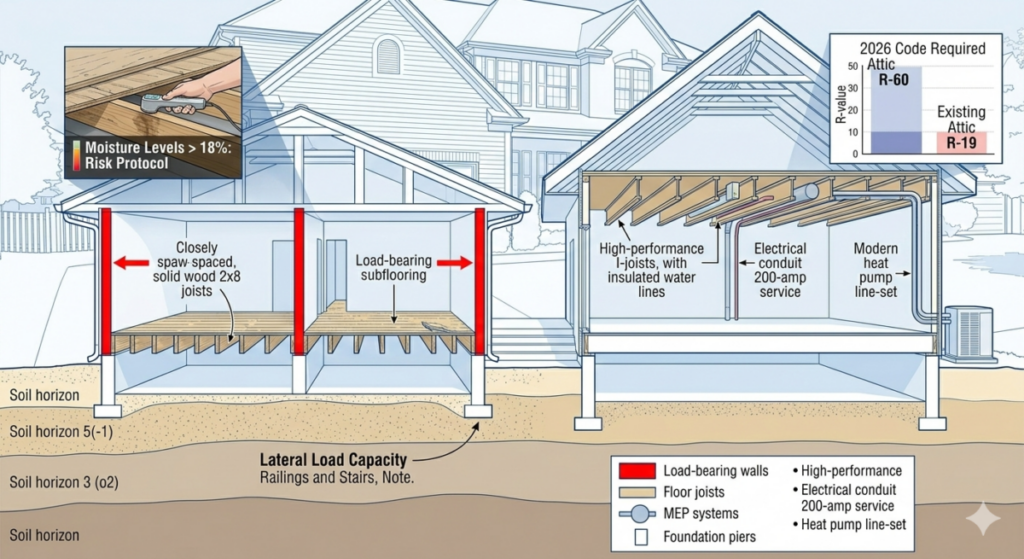

When you stay in a home for 30 or 40 years, you become blind to “structural creep.” In 2026, home inspections have become significantly more invasive due to new infrared scanning technologies and AI-driven moisture detection. Your “Last Move” plan must begin with a cold-blooded assessment of your home’s skeletal health. Most homes built between 1970 and 1995 are now hitting the end of their primary MEP cycles. Your copper plumbing is likely pitted: your electrical panel probably lacks the capacity for modern EV charging or heat pump systems: and your attic insulation R-value is likely 40% below 2026 code requirements.

From a structural physics perspective, your floor joists have likely experienced creep deflection under the weight of 40 years of stored boxes in the attic or garage. In engineering terms, wood under a constant load for decades undergoes a permanent deformation. If you have a crawlspace, the vapor barrier is likely shredded, leading to subfloor moisture levels exceeding 18%, which triggers mold remediation protocols in any 2026 sales contract. Before you list, you must calculate the Repair to ROI ratio. In many 2026 markets, spending $15,000 on a structural piering system to stabilize a settling corner will yield a $45,000 increase in final sale price. Ignoring it will result in a $60,000 price drop during the inspection period. Do the math: fix the bones before you paint the skin. This includes checking the lateral load capacity of your railings and stairs, as 2026 insurance requirements for buyers have tightened significantly on fall-risk hazards.

Additionally, the 2026 mechanical landscape has shifted. Older SEER-rated HVAC units are now viewed as liabilities due to the Phase-Out of legacy refrigerants. If your furnace or condenser is more than 12 years old, a 2026 buyer will likely demand a replacement credit of $12,000 to $18,000. By being proactive and installing a high-efficiency heat pump system in Month 9 of your plan, you not only eliminate this negotiation leverage but also appeal to the energy-conscious demographic that is currently driving the 2026 buyer pool. We must also address the Electrical Load Calculation. Most homes from the 1980s have 100-amp service. In 2026, modern lifestyles require at least 200-amp service to accommodate induction cooktops and high-speed home data hubs. Upgrading this early prevents your deal from falling through during the appraisal contingency.

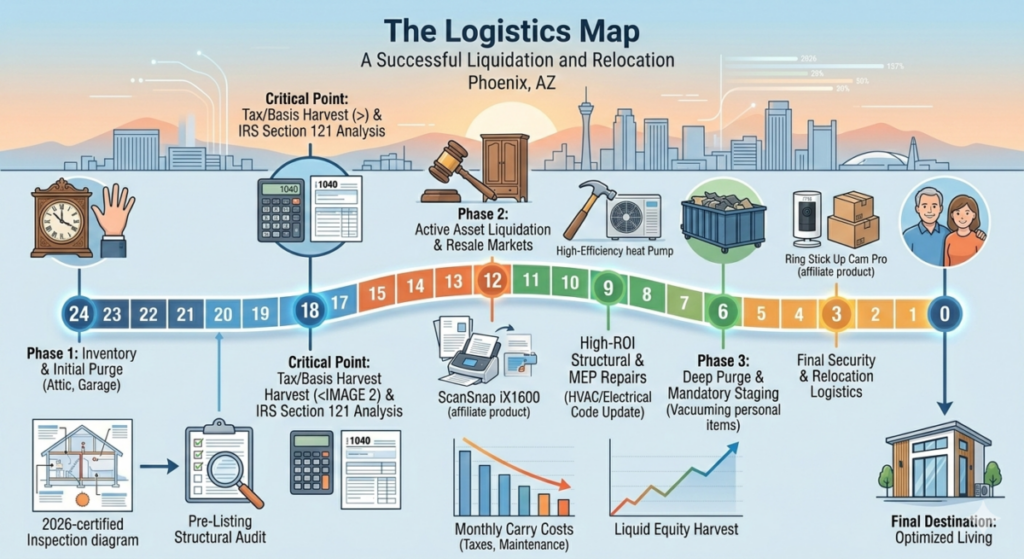

Downsizing Costs – The 24-Month Liquidation Timeline

You didn’t accumulate this junk in a weekend: you aren’t getting rid of it in one. I’ve seen families try to clean out a 3,000-square-foot house in three days. They end up throwing away $10,000 in sellable assets and paying $5,000 for emergency dumpsters. That is a $15,000 swing in the wrong direction. We do this in phases to ensure you extract every dollar of value from your contents.

Months 12 to 18 are for the Invisible Purge. This is when you hit the attic, the crawlspace, and the back of the garage. These are the areas that don’t affect your daily life but carry the heaviest psychological weight. Use a First-Principles filter: if an object has not been touched in 36 months and does not have a verified appraisal value over $500, it is garbage. Period. No, your kids do not want your 1994 Encyclopedia Britannica set. They don’t even want your fine china. Sell it now while there is still a dwindling market of collectors who use legacy auction sites. In 2026, the market for physical media and vintage housewares is highly volatile: waiting an extra year could mean the difference between a $2,000 estate sale check and a $500 junk hauling bill.

Months 18 to 12 involve the Utility Audit. This is where we look at your furniture. Most “senior” furniture is oversized, heavy, and built for a different era of architecture. It won’t fit in a modern luxury condo or an ADU. We begin listing these items on secondary markets now. In 2026, the resale market for brown furniture is at an all-time low, so you need time to find the one buyer who actually wants a 200-pound oak armoire. You are also auditing your lifestyle: do you really need a lawnmower if your next home has a condo association? Sell the equipment while it still runs and before the 2026 carbon-tax regulations on small gas engines make them harder to offload.

Technical Deep Dive: 2026 Tax Logic and IRC Section 121

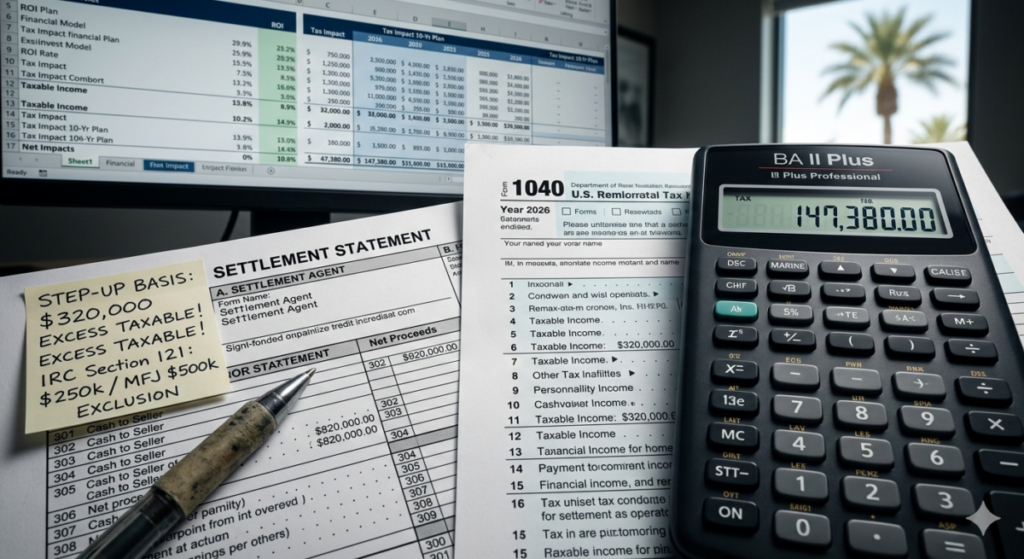

The most important part of your 24-month plan is the timing of your Capital Gains Harvest. Under IRC Section 121, as of 2026, you can still exclude up to $250,000 (single) or $500,000 (married filing jointly) of gain from the sale of your primary residence. However, if you have lived in your home for 40 years, your cost basis is likely floor-level. If you bought for $80,000 in 1986 and sell for $900,000 in 2026, you are looking at an $820,000 gain. Even with the $500,000 exclusion, you have $320,000 in taxable gains. This is where most people lose their shirts.

In 2026, the effective tax rate on that excess can exceed 20% when you factor in the Net Investment Income Tax (NIIT) and state-level levies. This is why we track every single capital improvement you’ve made since you bought the place. That new roof in 2012? It adds to your basis. That kitchen remodel in 2004? Basis. The 24-month window is for your CPA to hunt down these receipts. If you cannot prove the expenditure, the IRS will not grant the basis increase. I have seen homeowners save $40,000 in taxes just by finding a folder of old contractor invoices. Furthermore, we must look at Step-up in Basis rules. If one spouse passes away, in many states, the surviving spouse gets a “step-up” on at least half the home’s value. This is a cold, mathematical reality that influences whether you sell in 2026 or 2027. This isn’t “paperwork”: it is a high-yield investment of your time. Don’t let the government take your equity because you were too lazy to find a 20-year-old receipt for a deck installation.

We also need to evaluate Section 1031 logic for any partial rental use. If you have been renting out your basement or a room, that portion of the home does not qualify for the Section 121 exclusion. You may need to perform a Deferred Exchange into a smaller rental property to protect that portion of your equity. In 2026, the IRS has increased audit rates for “mixed-use” primary residences. The 24-month plan allows you to “clean up” your occupancy records to ensure you qualify for the maximum possible tax shield. Neglecting this technicality is effectively handing a $30,000 check to the Treasury for no reason.

2026 Downsizing Cost Transparency: Moving and Liquidation

The cost of labor has spiraled. In 2026, a full-service move is no longer a luxury: it is a significant capital expenditure that must be budgeted like a renovation. You need to decide if you are paying with your time or your equity. Below is the breakdown of what it actually costs to move a standard 3-bedroom home in the current market, including the hidden 2026 Environmental Fees.

2026 Downsizing Cost Table: Labor vs. Materials

| Service Category | Low-End (DIY/Basic) | High-End (Full Pro) | 2026 Risk Factor |

|---|---|---|---|

| Estate Liquidation / Junk Hauling | $1,200 (Dumpster + DIY) | $6,500 (White Glove Clean-out) | Landfill fees up 15% due to sorting laws. |

| Professional Packing/Moving | $3,500 (Truck Rental + Friends) | $14,500 (Full Pack/Unpack) | Fuel surcharges apply to distances > 50 miles. |

| Home Staging & Prep | $600 (Deep Clean Only) | $8,800 (Furniture Rental/Design) | Virtual staging is cheaper but fails in-person. |

| Legal & Closing Prep | $1,500 (Standard Title) | $4,800 (Estate Trust Integration) | New 2026 Title Regulations regarding ID theft. |

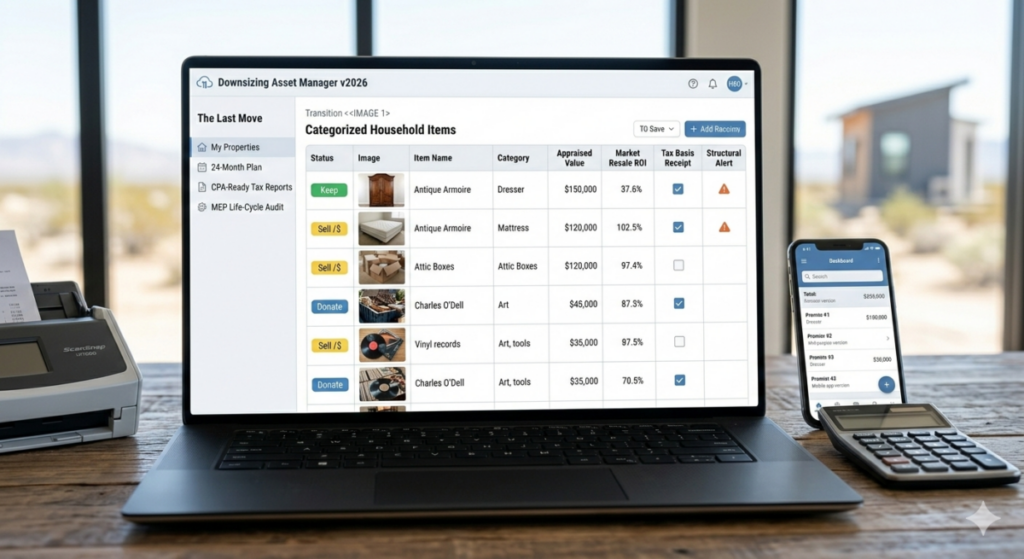

Affiliate Product Comparison: The Liquidation Toolkit

| Product | Use Case | Efficiency Rating |

|---|---|---|

| ScanSnap iX1600 | Digitizing 40 years of tax receipts and basis records instantly. | 9.8/10 |

| Dymo LetraTag 200B | Labeling boxes for Keep, Sell, and Donate during the 24-month purge. | 8.5/10 |

| Ring Stick Up Cam Pro | Monitoring your home during the “vacant staging” period after moving. | 9.2/10 |

Financial Trajectory: The 10-Year Downsizing ROI

Why do we do this? Is it just to live in a smaller place? No. It’s to avoid the Maintenance Trap. If you stay in your 4,000-square-foot home, your annual maintenance, insurance, and tax carry is likely 3.5% of the home’s value in 2026. On a $1,000,000 home, that is $35,000 a year. Over 10 years, that is $350,000—and that’s if nothing major breaks. If you need a new roof or HVAC, add another $50,000.

By downsizing to a $600,000 highly efficient home or luxury apartment, you reduce that carry to 1.5% or $9,000. You also harvest $400,000 in cash. If you invest that $400,000 at a conservative 5.5% return (common for 2026 municipal bonds or high-yield vehicles), you generate $22,000 in annual income. The swing between paying $35,000 and earning $22,000 is a $57,000 annual net-worth pivot. Over 10 years, downsizing isn’t just a move: it is a $570,000 financial engine for your lifestyle and legacy. This is first-principles investing. You are trading a static, depreciating physical asset for a liquid, appreciating financial asset. It is the difference between worrying about property taxes and booking a 3-month cruise with the interest alone.

Technical Deep Dive: ROI Calculations and Opportunity Cost

To truly understand the Downsizing ROI, we must look at the Marginal Utility of Square Footage. In your 60s, you likely use 20% of your home 80% of the time. You live in the kitchen, the primary bedroom, and the living room. The “dead rooms”—guest bedrooms that are used twice a year, formal dining rooms, and finished basements—still require climate control (HVAC cycles) and property tax allocations. In 2026, energy costs have stabilized at 25% higher than 2022 levels. Heating a room you don’t enter is a mathematical absurdity. You are literally burning cash to keep dust warm.

Furthermore, the opportunity cost of the equity trapped in a large home is staggering. If your $1M home appreciates at 3% per year, you make $30,000 in paper wealth. But if you downsize, take $40,000 in cash, and invest it in a diversified REIT or dividend-aristocrat portfolio yielding 7% (total return), you are significantly outperforming the residential real estate market without the risk of a roof leak or a basement flood. We also have to account for the Age-In-Place Modification Cost. To make a traditional two-story home safe for a 75-year-old involves installing chair lifts ($5k-$10k) or walk-in tubs ($15k). Moving to a single-level “right-sized” home eliminates these sunk costs entirely. You aren’t just saving money: you are avoiding future capital expenditures that have zero resale ROI. In 2026, a buyer won’t pay extra for your walk-in tub: they’ll likely ask for a credit to remove it. You are effectively paying twice for a feature that devalues your asset.

Finally, we calculate the Property Tax Variance. In 2026, many municipalities have implemented Ad Valorem reassessments that penalize large single-family homes to encourage density. By moving to a smaller footprint, you may move into a lower tax tier or qualify for senior exemptions that are capped at lower valuations. A $5,000 annual reduction in property taxes is the equivalent of adding $100,000 to your investment portfolio at a 5% yield. This is the logic of Asset Allocation: you are moving wealth from a high-tax environment to a low-tax environment while maintaining your quality of life.

The “Hard Truth” About Your Heirs and Assets

I’ve handled countless transactions where the children are left to clean up the “Last Move.” It is a nightmare of logistics and grief. They don’t want your stuff. They want your memories and your money. By executing this 24-month plan yourself, you are giving them a massive gift. You are liquidating the physical burden while you still have the cognitive and physical energy to manage the logistics. In 2026, professional Estate Remediation companies charge $150 per hour per person. If you leave a house full of junk, your estate will pay $20,000 to clear it before it can even hit the market. That is money that could have gone to your grandkids’ college funds or a family vacation.

I once worked with a seller who had 4,000 vinyl records. He spent 18 months selling them individually on Discogs. He turned “junk” into $22,000 in cash. If he had died, his kids would have called a hauler, paid $500 to take them away, and the hauler would have made the $22,000. Be the guy who makes the $22,000. Don’t be the guy who leaves a bill for his children. This logic applies to everything: the tools in the garage, the hobby equipment in the basement, and the excessive kitchen gadgets. Liquidate now, while you can control the price and the destination of the assets. In 2026, the market for legacy goods is shifting to digital platforms that require time to master. Start early.

Actionable Checklist: The 24-Month Master Plan

- Month 24: Hire a 2026-certified home inspector for a Pre-Listing Structural Audit. Identify every MEP failure point and structural risk before they become negotiation chips for a buyer. Pay special attention to the Foundation Physics and soil compaction around the perimeter.

- Month 22: Create a Digital Asset Ledger. Use a scanning tool to digitize every home improvement receipt from the last 30 years to maximize your tax basis under IRC Section 121. This single step can save $10,000+ in taxes.

- Month 20: The Storage Unit Rule. If it is in a box in the garage, it goes. Rent a dumpster for one weekend and be ruthless. If you haven’t seen it since 2010, it is not a “memory”: it is a fire hazard.

- Month 18: Appraise the High-Value Outliers. Hire a professional for any art, jewelry, or rare collectibles. Do not trust eBay “asking prices”: get a certified 2026 appraisal for liquidation value so you know your floor price.

- Month 15: The Furniture Draft. Measure your new target square footage. If a piece of furniture doesn’t fit the 2026 minimalist aesthetic or physical footprint, list it on Facebook Marketplace or specialized estate sites immediately. Large dining sets are the first to go.

- Month 12: Interview three Real Estate Investment Experts (not just “agents”). You want someone who understands Equity Extraction Strategy, not someone who just wants to host an open house and eat your cookies.

- Month 9: Execute High-ROI Repairs. Fix the structural issues identified in Month 24. This is the “Bone-Deep” prep that prevents deal-killers. Replace that 20-year-old water heater now so it’s a “new feature” on the listing.

- Month 6: The Final Cleanse. Your home should now look like a high-end hotel. No personal photos, no clutter, no “you.” This is when you transition from “Homeowner” to Asset Manager. You are selling a product, not a lifestyle.

- Month 3: Lock in your 2026 moving contract. Secure your dates and verify the fuel surcharge caps to avoid last-minute price gouging. Moving in 2026 requires more lead time due to labor shortages in the logistics sector.

- Closing Day: Finalize the deposit strategy with your financial advisor. Ensure your equity starts working the minute it leaves the escrow account. Transfer funds directly into a high-yield vehicle to start offsetting your new (and lower) living expenses.

Internal Resources

- Learn how to calculate your 2026 Home Maintenance Budget to see what your current house is actually costing you in real dollars.

- Check out our guide on ADU Construction Costs in 2026 if you are considering building a small unit on a family member’s property.

- Read our analysis of The Best States for Retirement Taxes in 2026 before you pick your final destination.

- ALL COMING SOON

Summary

Downsizing costs. Downsizing is the ultimate First-Principles move for anyone over 60. You are trading a high-maintenance physical liability for a high-liquidity financial asset. By starting 24 months out, you avoid the emotional and financial panic-tax that destroys most senior moves. In 2026, the winners are those who treat their home like a business and their move like a strategic exit. Don’t let your house own you: own the move. You’ve spent decades building this equity: don’t let a poor timeline or lack of technical prep give it away to a savvy buyer or the tax man. Move with purpose, move with logic, and make this your most profitable transaction yet.

Bio: Charles O’Dell

Charles O’Dell is the owner of HousingAfter60.com and a veteran real estate investor with over 23 years of experience. Having flipped more than 100 properties and facilitated hundreds of transactions, Charles specializes in helping homeowners over 60 maximize their net worth through ruthless equity extraction and logical downsizing. He ignores the “fluff” of real estate and focuses entirely on the bottom line: ensuring your last move is your best investment.

Charles O’Dell has flipped 100+ properties and managed 500+ senior transitions over 23 years.