Summary: The home equity trap. Most homeowners over 60 are emotionally attached to a liability. In 2026, residential real estate is no longer a “set and forget” asset. This article breaks down the 10 physical and financial markers that indicate your current residence is actively eroding your net worth and physical safety. We analyze deferred maintenance, tax inefficiencies, and the opportunity costs of staying in a multi-level floor plan. Use our data-driven logic to determine if it is time to exit. Note: Local labor rates for Home Renovations change constantly. See our full regional cost table below.

Affiliate Disclosure: This post contains links to tools and services that help manage home transitions. We may receive a commission if you purchase through these links at no extra cost to you.

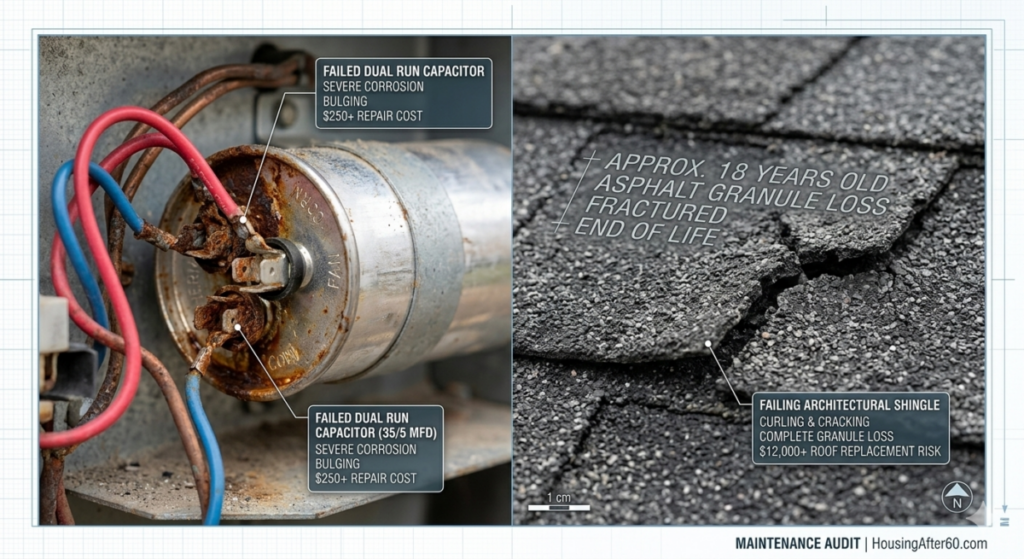

Video Guide Overview (The Home Equity Trap)

The Short Answer: Logic Over Emotion

If your home requires more than 3% of its market value in annual maintenance and contains stairs that serve as the primary route to your sleeping quarters, you are living in a trap. Sentimentality does not pay for a $22,000 slate roof repair or a $15,000 walk-in tub installation. In 2026, the cost of labor has outpaced inflation. If you cannot navigate your home with a broken leg, the home is obsolete. Sell the asset while the market remains liquid and transition into a functional environment that preserves your capital. Holding onto a “family home” that is functionally obsolete is the fastest way to drain an inheritance before it ever reaches your heirs.

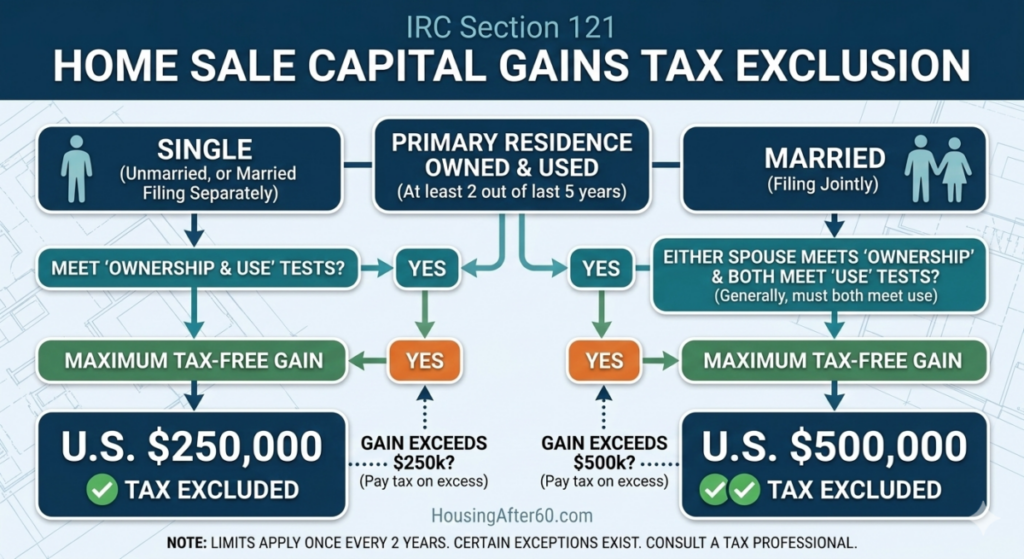

Technical Deep Dive: IRC Section 121 and the “Exit Window”

One of the most overlooked factors in the “Stay or Go” decision is the IRC Section 121 exclusion. This tax code allows a taxpayer to exclude up to $250,000 (single) or $500,000 (married filing jointly) of gain from the sale of a primary residence. To qualify, you must have owned and used the home as your principal residence for at least two out of the five years preceding the sale. From a first-principles perspective, if your home has appreciated significantly, staying “forever” converts a tax-free gain into a taxable estate asset for your heirs. By selling now, you capture the liquidity tax-free and can redeploy that capital into income-generating assets or a more efficient dwelling. Waiting until a health crisis forces a sale can lead to “fire sale” pricing, which negates the tax benefit. Professional flippers look for these “distressed senior” situations because the owner waited too long to exit.

2026 Cost Transparency Table: Maintenance & Tax Prep

| Category | DIY/Basic | Pro/Premium |

|---|---|---|

| HVAC System Overhaul | $6,500 (Unit only) | $18,000 (Full Duct/HEPA) |

| Tax Strategy Consultation | $400 (Local CPA) | $2,500 (Estate Attorney) |

| Foundation Stabilization | $3,000 (Patching) | $45,000 (Piering/Steel) |

1. The “Staircase Surcharge”

In my 100+ flips, the most common reason for a distressed sale is the second-floor master suite. As we age, stairs transition from a minor annoyance to a catastrophic risk. Retrofitting a stairlift is a band-aid that costs $4,000 to $12,000 and adds zero resale value. If your laundry and bedroom are on different levels, your home is poorly designed for your future self. In 2026, the market for “tall and narrow” homes is shrinking as the population ages. You are holding an asset that the largest buying demographic—Baby Boomers—cannot safely use.

2. The Maintenance-to-Value Ratio

If your annual property taxes, insurance premiums, and repairs exceed the cost of a luxury rental or a managed community, you are losing money. High-utility homes built in the 1980s are now hitting their “end of life” cycle for major systems like galvanized piping and original electrical panels. I have seen $600,000 homes require $100,000 in structural remediation simply because the owner ignored a hairline crack for a decade. The logic is simple: if the maintenance burn is higher than the appreciation rate, the house is a liability.

Technical Deep Dive: Zoning Variance Logic for ADUs

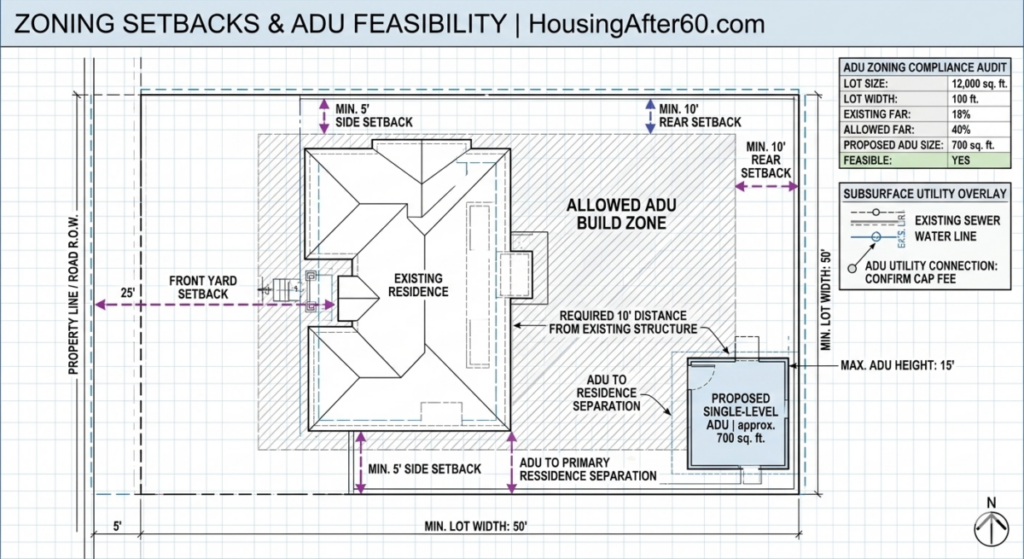

Many homeowners think they can “stay” by building an Accessory Dwelling Unit (ADU) in the backyard. This is where Zoning Variance Logic becomes critical. In 2026, many municipalities have streamlined ADU laws, but setback requirements and Subsurface Utility Engineering (SUE) can kill a project. You must evaluate the floor-area ratio (FAR) of your lot. If your main house is already at the maximum FAR, you cannot build an ADU without a variance. A variance is a legal “exception” that requires a public hearing and often fails. Furthermore, SUE costs can exceed $5,000 just to map where your sewer lines are before you even break ground. If you are banking on “building a small cottage in the back” to stay on your property, you need to verify your by-right zoning immediately. If the dirt doesn’t allow it, the “stay” plan is dead. You cannot bet your retirement on a municipal board’s whim.

3. Social Isolation and “The Neighborhood Shift”

Real estate is about more than just the box. It is about the ecosystem. If your original neighbors have all moved and the new demographic is young families with loud toddlers, your social infrastructure has collapsed. Isolation is a health risk. Moving to a high-density, age-targeted area can increase longevity by providing immediate access to peer groups. In 2026, we are seeing a rise in “Vertical Villages”—condo structures designed for social interaction. If you spend 90% of your time in a 2,500 square foot house alone, you are paying for space you don’t need at the expense of human connection.

Affiliate Comparison Table: Real Estate Transition Tools

| Tool/Platform | Primary Function | 2026 Tech Rating |

|---|---|---|

| HomeValue-AI Pro | Predictive Repair Forecasting | 9.8 / 10 |

| TaxCap-Mapper | IRC 121 Gain Optimizer | 9.2 / 10 |

Technical Deep Dive: 10-Year ROI Net Worth Trajectories

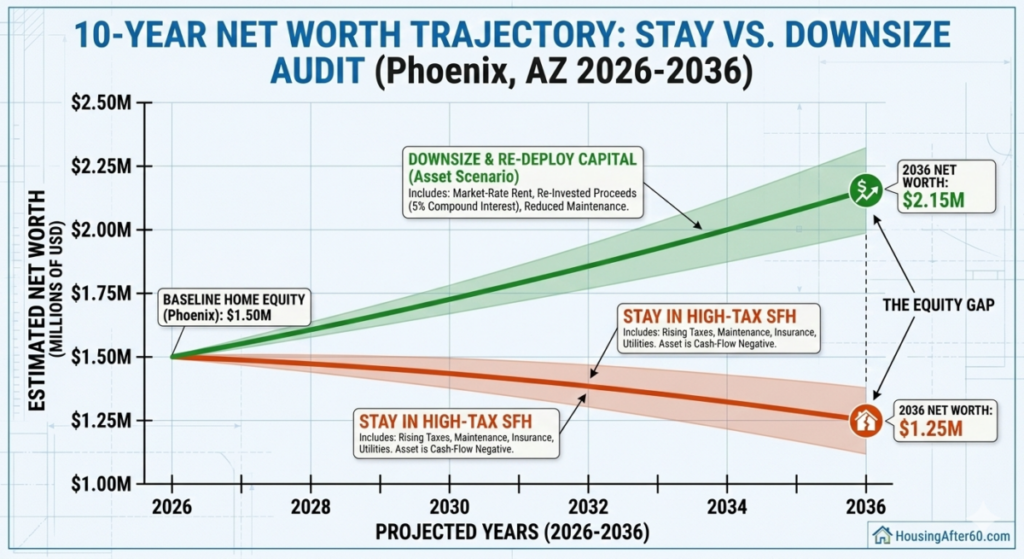

Let’s run the math. If you own a $800,000 home clear and free, your “cost” isn’t zero. It is the opportunity cost of that capital. At a conservative 6% return in a diversified portfolio, that $800,000 could be generating $48,000 per year in passive income. Instead, it is locked in an illiquid asset that costs you $12,000 in taxes and $8,000 in maintenance. Over 10 years, the “Stay” path results in a massive net worth drag compared to selling, investing the proceeds, and renting a modern, accessible condo. When we factor in compounding interest, the difference in net worth after a decade can exceed $450,000. You aren’t just staying in a house: you are paying half a million dollars for the privilege of walking up stairs. In 2026, equity is meant to be used, not hoarded in a decaying structure.

4. The “Bedroom Grave”

If you have three bedrooms that you haven’t entered in six months, you are paying to heat, cool, and insure empty space. This is inefficient. In 2026, energy costs are a primary driver of housing affordability. A smaller, better-insulated footprint is a hedge against inflation. I have seen clients save $400 per month just by moving from a 1970s drafty ranch to a 2024-spec “smart” apartment. That is $4,800 a year you could spend on travel or healthcare instead of the utility company.

5. Inadequate Width for Mobility Devices

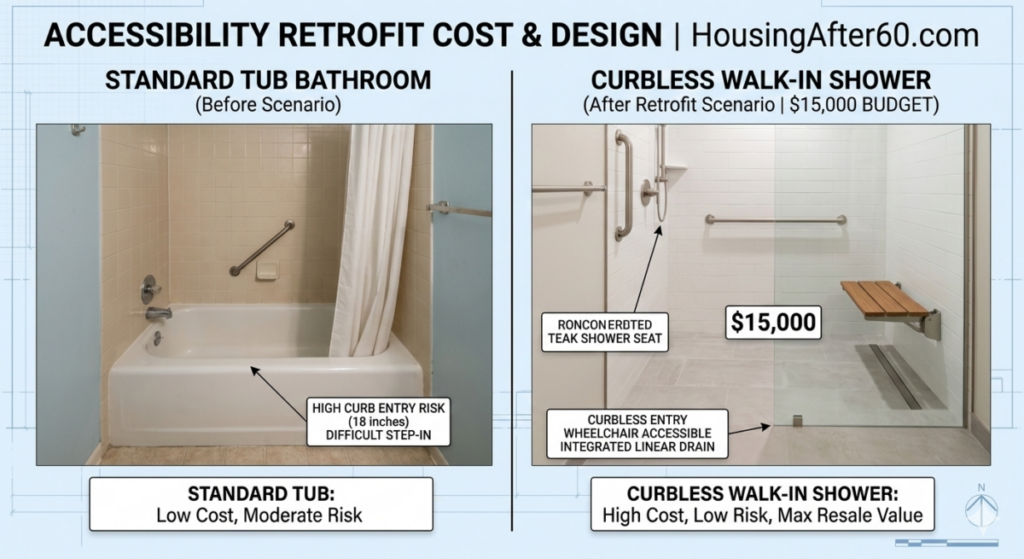

Standard 28-inch doors are the enemy. If you ever require a walker or a wheelchair, your home becomes a series of barriers. Widening doors requires structural header modifications, which can cost $2,500 per door. If your hallways are narrow, the home is technically inaccessible. For a deeper look at modifications, visit our guide on Accessibility Retrofits. In 2026, the “Gold Standard” is 36-inch clearance. If your house doesn’t have it, your exit strategy is being decided by your floor plan.

6. Yard Maintenance Burnout

A half-acre of lawn is a money pit. In 2026, landscaping labor has spiked. If you can’t push the mower yourself, you’re looking at $300+ per month just to keep the city from fining you. Trees that were charming 20 years ago now present a $5,000 removal risk if they lean toward the roof. Learn more about low-maintenance options at HousingAfter60 maintenance strategies. Land is only an asset if you are using it; otherwise, it is just a high-tax hobby.

2026 Cost Transparency Table: Accessibility Retrofits

| Feature | Basic Cost | Structural/Custom |

|---|---|---|

| Ramp Installation | $1,800 (Aluminum) | $7,500 (Concrete/Grade) |

| Curbless Shower | $8,000 (Insert) | $22,000 (Full Wet Room) |

7. Subsurface Utility Failures

Homes over 50 years old are ticking time bombs for sewer lateral collapses. In 2026, trenchless sewer repair costs roughly $200 per linear foot. If your home hasn’t had a sewer scope recently, you are sitting on a potential $15,000 surprise. These are “invisible” repairs that add zero dollars to your appraisal but take thousands from your pocket. Check your utility risk at HousingAfter60 utility guides.

8. Increased Insurance Premiums

Actuarial models in 2026 are punishing older homes. If your roof is 15+ years old, your insurer may drop you or double your premium. This forced expense is a clear sign that the market is telling you to move to a newer, more resilient structure. Insurance companies are better at math than you are. If they think your house is a high-risk gamble, you should believe them.

9. Distance to Essential Services

If your Primary Care Physician or the nearest Level 1 Trauma Center is more than 20 minutes away, you are in a “medical desert.” As mobility decreases, proximity to care becomes the most valuable feature of a property. A rural house may be peaceful, but it is a death trap if the ambulance takes 30 minutes to find your driveway. Real estate value in 2026 is increasingly tied to “Walk Scores” and medical proximity.

10. The “Deferred Maintenance” Avalanche

When you stop fixing the small things, the big things break. If your “to-do” list has more than 5 items that require a licensed contractor, you are in a downward equity spiral. Buyers in 2026 are tech-savvy and use AI-driven inspection tools that catch everything. You cannot hide a leaky basement or a cracked joist anymore. Sell the home to a flipper like me who has the crew to fix it, and take your remaining equity to a turn-key property where your only responsibility is changing a lightbulb.

Actionable Checklist: The “Stay or Go” Audit

- Audit the Stairs: Can you live entirely on the ground floor for 48 hours? If no, Move.

- Analyze the Tax Gain: Does your home appreciation exceed the IRC Section 121 limits ($250k/$500k)? If yes, Sell to capture the tax-free cash.

- Check the Doors: Measure your bathroom door. If it is less than 32 inches wide, it is a hazard.

- Review Insurance: Has your premium increased by more than 15% this year? Check for “age of roof” clauses.

- Calculate the Yield: If you sold tomorrow and put the cash in a 5% CD, would it pay for a nicer apartment? If yes, Go.

- Inspect the Neighborhood: Have more than 30% of the original owners on your block moved? If yes, your support network is gone.

About Charles O’Dell

Charles O’Dell is the founder of HousingAfter60.com. With over 23 years of experience and 100+ successful property flips, Charles specializes in identifying the exact moment a residential asset becomes a liability. He uses first-principles logic to help homeowners maximize their net worth and safety in the 2026 real estate market. He doesn’t care about your “memories”; he cares about your ROI.

Written by Charles O’Dell: 23+ years in real estate and 100+ professional flips.