| Article Summary |

|---|

| I have flipped over 100 houses: and I have seen equity disappear faster than a free pizza at a frat house. In 2026: reverse mortgages are the hot “solution” for cash-strapped seniors. They promise tax-free cash without monthly payments. But there is no such thing as a free lunch. We break down the massive upfront fees: the compounding interest traps: and the 2026 FHA rules you must know. If you want to keep your house: read the math first. Note: Local labor rates for home maintenance and appraisal fees change constantly. See our full regional cost table below. |

Introduction: Why Reverse Mortgages Are Getting Attention Again

Welcome to 2026. If you have looked at your grocery bill lately: you know that “fixed income” feels more like a “broken income.” Retirement pressure is at an all-time high. While your bank account might look a bit thin: your house is likely sitting on a mountain of equity. Home prices have stayed stubbornly high: making many retirees “house-rich” but “cash-poor.”

Lenders know this. They are hitting your mailbox and TV screen with aggressive ads. They make it sound like the government is just handing out checks to anyone over 62. It sounds like a dream: stay in your home: get paid: and never write a mortgage check again. But as a guy who has spent two decades looking at the “bottom line” of property deals: I am here to tell you that the debt grows like a weed in a rainy July.

The purpose of this guide is simple. I want to strip away the emotional marketing and give you the cold: hard logic. We will look at why these loans are popular: how they actually work: and why your heirs might end up with nothing but a “Thank You” note if you aren’t careful.

Video Guide Overview

Affiliate Disclosure

I value transparency. Some of the links in this article are affiliate links. This means if you click them and buy a product: I might get a small commission. This helps keep the lights on at HousingAfter60.com so I can keep telling you the truth about real estate. I only recommend tools I would use on my own flips.

The “Short” Answer

A reverse mortgage is a loan for homeowners aged 62 and older that requires no monthly mortgage payments. Instead: the lender pays you. The loan is eventually repaid when you sell the home: move out: or pass away. While it provides immediate cash flow: it is one of the most expensive ways to borrow money due to high upfront fees and compounding interest that eats your equity. In 2026: this tool is best for those who have no heirs and intend to die in their home. For everyone else: it requires extreme caution and a firm understanding of the 2% initial mortgage insurance premiums.

Technical Deep Dive: The 2026 Interest Rate Environment

To understand the 2026 reverse mortgage: you have to understand the cost of money. In the current economic climate: interest rates have stabilized: but they are significantly higher than the “free money” era of the early 2020s. For a Home Equity Conversion Mortgage (HECM): your interest rate is composed of a fixed margin plus an index (usually the 10-year Treasury or SOFR).

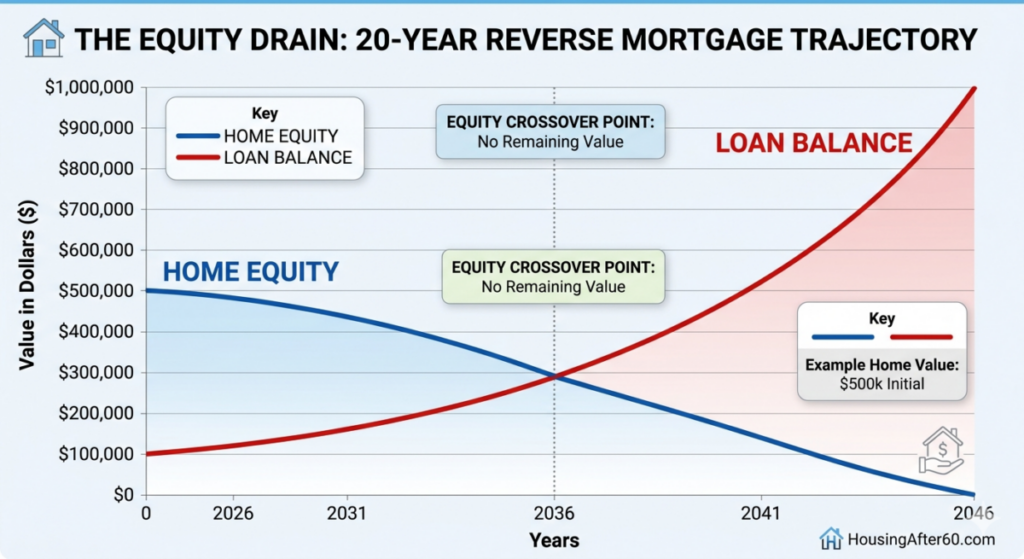

When rates are 6% or 7%: the compounding effect is brutal. Because you are not making monthly payments: that interest is added to your loan balance every single month. This is “negative amortization.” On a $400,000 loan: a 7% interest rate adds $28,000 to your debt in just the first year. By year ten: you aren’t just paying interest on the original loan: you are paying interest on the interest. From a first-principles perspective: you are selling your home to the bank in slow motion. If your home appreciation doesn’t outpace this compounding debt: you are effectively liquidating your estate while you sleep.

What Is a Reverse Mortgage?

Think of a traditional mortgage as a mountain you are climbing down. Every payment you make brings the balance closer to zero. A reverse mortgage is the opposite: it is a mountain you are climbing up. You start with a balance: and it grows every month.

The most common type is the HECM: which is backed by the FHA. You can take the money as a lump sum: a monthly check: or a line of credit. The coolest part of the line of credit? The unused portion actually grows over time: giving you more borrowing power later. But remember: you still own the home. That means you are still the one who has to fix the leaky roof and pay the taxman. If you fail to maintain the property or miss a tax payment: the bank can take the house just like a regular foreclosure.

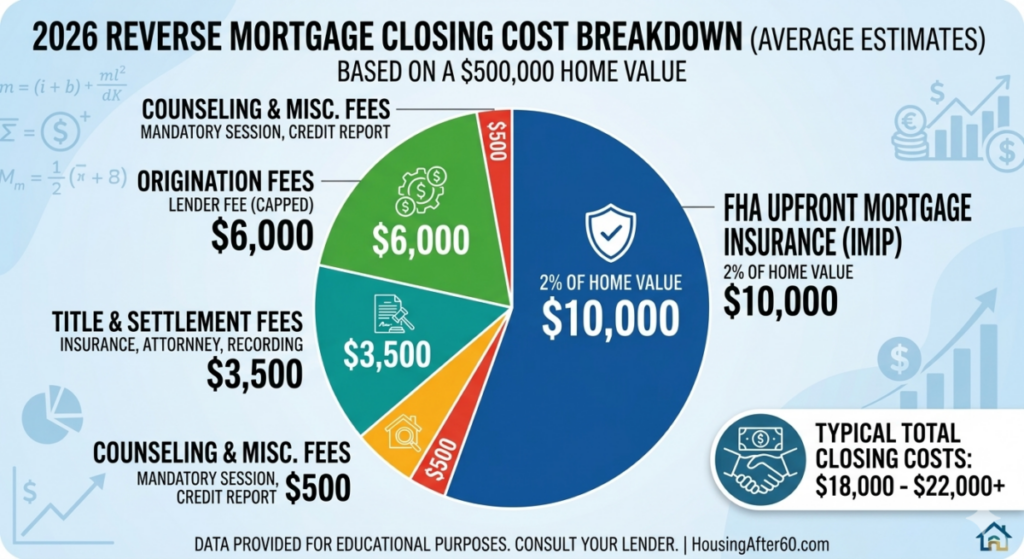

| Expense Category | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Origination Fee | $2,500 | $6,000 (Capped) |

| Appraisal & Inspection | $600 | $1,200 |

| Mortgage Insurance (IMIP) | 2% of Home Value | 2% of Home Value |

| **Total Upfront Costs** | **$13,100 (on $500k home)** | **$20,000+** |

Technical Deep Dive: Zoning and Property Standards

Not every house qualifies for an FHA reverse mortgage. In 2026: HUD has tightened the screws on property standards. Your “charming” fixer-upper might be a deal-breaker. To qualify: the home must be your primary residence and meet strict safety codes. I have seen loans denied because of peeling lead paint or a deck that lacked a railing.

Furthermore: zoning matters. If your property is zoned for mixed-use or is a non-warrantable condo: you are going to hit a wall. Lenders want “marketable” collateral. They are essentially buying your house on an installment plan: and they don’t want to be stuck with a property that has legal hurdles or structural rot. If you are planning to use a reverse mortgage: your first step is a “pre-inspection” to ensure you don’t waste $1,000 on a mandatory appraisal that fails. In 2026: expect appraisers to be more scrutinizing about “deferred maintenance” than ever before.

Who Typically Uses Reverse Mortgages

The typical candidate is someone like my neighbor: let’s call him “Bob.” Bob is 72: his pension hasn’t kept up with inflation: and his roof needs $15,000 in work. He has $600,000 in equity but only $10,000 in the bank. For Bob: the reverse mortgage is an emergency exit. It allows him to fix the roof and breathe easier without having to move to a smaller apartment.

The Good: Real Advantages of Reverse Mortgages

I am not all gloom and doom. There are times when this math actually works.

- Cash Flow is King: This is the primary driver for most retirees. If your fixed income is being strangled by inflation, a reverse mortgage can eliminate a monthly mortgage payment (e.g., $2,000/month). This instantly increases your monthly “disposable” income without you having to move or find a job.

- Non-Recourse Protection: This is a massive safety net provided by the FHA. Because HECMs are non-recourse loans, you (or your heirs) will never owe more than what the home is worth at the time of sale. If the market crashes and your loan balance is $500,000 but the house sells for $400,000, the FHA covers the $100,000 gap. You are off the hook.

- Strategic Social Security Timing: If you are 62 and short on cash, taking a reverse mortgage can act as a “bridge” that allows you to wait until age 70 to claim Social Security. Since your benefit increases by roughly 8% for every year you delay, the long-term increase in your government check may actually outpace the cost of the loan interest.

- Tax-Free Proceeds: According to the IRS, money from a reverse mortgage is considered a loan advance, not income. This means the cash you receive is generally tax-free and typically does not affect your Social Security or Medicare benefits (though it can impact needs-based programs like Medicaid if not managed correctly).

- Line of Credit Growth: If you choose the “Line of Credit” option and don’t spend the money immediately, the unused portion grows over time. In a high-interest environment like 2026, this growth rate is even higher, meaning your future borrowing power increases the longer you wait to touch the money.

| Affiliate Product | Why You Need It | Estimated Price |

|---|---|---|

| Home Equity Planner Pro | Software to model 20-year equity depletion. | $49.00 |

| Safe-T-Step Ladder | Maintain your home safely to avoid FHA violations. | $189.00 |

| Digital Document Fire Safe | Keep your original loan docs and deeds secure. | $120.00 |

Technical Deep Dive: ROI and Opportunity Cost

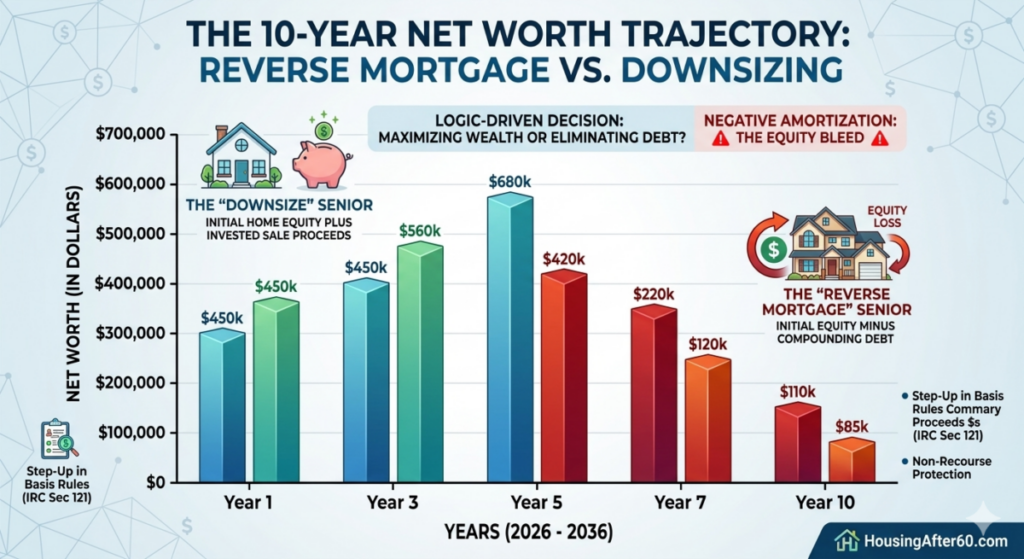

Let’s talk about opportunity cost. If you take $100,000 out of your home via a reverse mortgage: what are you doing with it? If you are using it to pay off a 24% credit card: you are a financial genius. You are swapping high-interest toxic debt for lower-interest (though still compounding) mortgage debt.

However: if you take that money and put it in a savings account earning 4%: while your reverse mortgage costs 7%: you are losing 3% every year on every dollar. This is “negative carry.” In 10 years: that $100,000 has cost you a fortune in lost net worth. I always tell my clients to look at the “10-year net worth trajectory.” If the goal is to maximize your total wealth: a reverse mortgage is rarely the winner compared to downsizing. Downsizing allows you to capture your equity and invest it: whereas a reverse mortgage allows you to spend it while paying interest for the privilege. From a first-principles perspective: the interest expense on an HECM is the price of your independence: but it is a price that doubles every decade at current rates.

The Bad: The Major Drawbacks

The biggest “Bad” is the cost of entry. Imagine going to a restaurant and the waiter tells you it costs $15,000 just to sit down. That is a reverse mortgage. The Initial Mortgage Insurance Premium (IMIP) is 2% of your home’s appraised value. On a $600,000 house: you are out $12,000 before you even get your first check.

Then there is the maintenance trap. You must keep the house in “good repair.” If a lender decides your house is falling apart: they can call the loan due. I’ve seen it happen. They send an inspector: find a hole in the roof: and suddenly you are in default. It is a ruthless business model. You are effectively renting your own home from the bank: and the rent is paid in the form of your remaining equity.

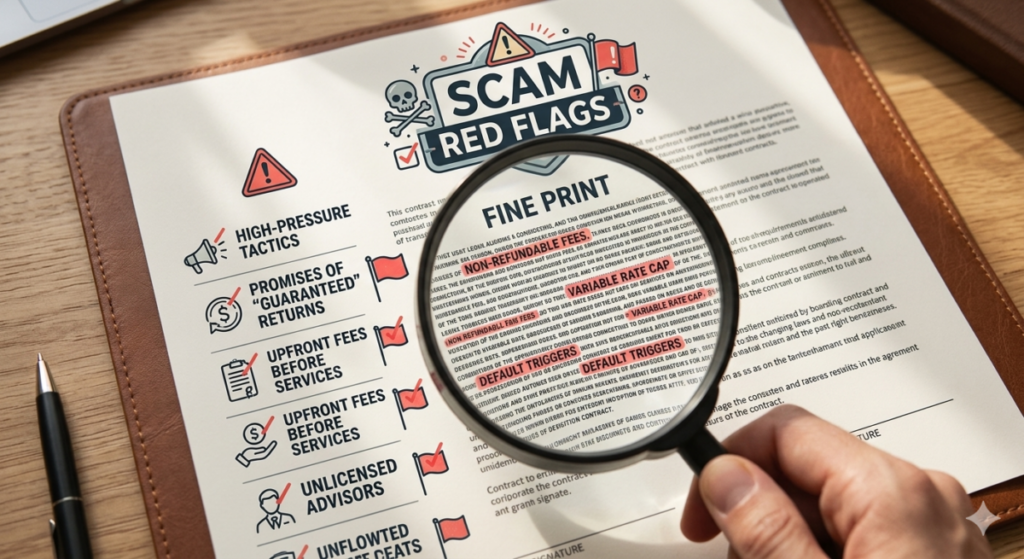

The Ugly: Common Reverse Mortgage Scams

Scammers love reverse mortgages because that is where the big money is. One common scam involves “Free Home Repairs.” A contractor tells you they can fix your house for free by helping you get a reverse mortgage. They do the work (poorly): take the lump sum: and disappear: leaving you with a massive loan balance and a leaky roof.

Another one is the “Investment Advisor” who wants you to take a reverse mortgage to buy a “guaranteed” annuity. Spoiler alert: the annuity pays 3%: and the loan costs 7%. The only one making money is the advisor’s commission. If anyone pressures you to sign a document “today”: run. Fast. Your equity is your lifeblood: don’t let a vampire in a suit talk you into a “guaranteed” loss.

Technical Deep Dive: IRC Section 121 and Heir Logic

One of the most complex areas of the reverse mortgage is the tax implication for heirs. Under IRC Section 121: you can exclude up to $250,000 ($500,000 for couples) of capital gains when you sell your primary residence. When you die: your heirs get a “step-up in basis” to the current market value.

However: if you have a reverse mortgage: your heirs don’t just inherit a house: they inherit a debt that is growing. If the debt is 95% of the home’s value: the “step-up in basis” is practically useless because there is no equity left to protect. They have to decide within 30 days of your death whether they want to keep the house by paying off the loan (usually 95% of the appraised value) or walk away. This creates a massive logistical burden during a time of grief. From a technical estate planning perspective: a reverse mortgage is an “equity-eating machine” that neutralizes the benefits of the step-up in basis. If you want your children to inherit the family home: a reverse mortgage is the quickest way to ensure they never do.

Reverse Mortgage Rules in 2026

The rules haven’t gotten easier. To get a loan in 2026, you must follow these specific steps and meet these updated federal criteria:

- Attend Mandatory HUD Counseling: You must complete a 60-to-90-minute session with a HUD-approved counselor. This is not optional. They will provide an “impartial” look at your finances and ensure you aren’t being coerced. The certificate you receive is valid for 180 days.

- Pass the 2026 Financial Assessment: Unlike the “old days,” lenders now perform a deep dive into your credit history and “residual income.” They need to prove you have enough cash left over every month (after paying the mortgage) to cover food, utilities, and medicine.

- Verify the 2026 Lending Limit: For 2026, the FHA HECM maximum claim amount has been increased to $1,249,125. If your home is worth more than this, the bank will only calculate your loan based on this cap. For high-value estates, you may need to look at “Jumbo” private reverse mortgages instead.

- Clear the Life Expectancy Set-Aside (LESA): If your credit history shows missed tax or insurance payments in the last 24 months, the lender will likely require a LESA. This means a portion of your loan proceeds is “locked away” in a separate account specifically to pay your property taxes and insurance for you.

- The “Occupancy” Certification: You must sign an annual certification proving the home is still your primary residence. In 2026, HUD has increased monitoring on this; if you are away for more than 12 consecutive months (even for a hospital stay), the loan is triggered due and payable.

- Meet FHA Property Standards: Your home must pass an FHA appraisal. In 2026, this means no peeling lead-based paint, no structural rot, and no “safety hazards” like missing handrails. If the house fails, you must use part of the loan proceeds to fix it immediately or the loan won’t close.

What Happens to the House After the Owner Dies?

Your kids won’t be kicked out on the street the next day: but the clock starts ticking. Usually: the lender gives heirs 6 months to either sell the house or refinance the debt. If they can’t: the bank forecloses. This is why I tell people: if you want to leave a legacy: a reverse mortgage is your enemy. If you want to spend your last dime on a cruise and leave the bank with the keys: then you are using first-principles logic correctly. The bank is not your friend: they are an investor in your longevity. The longer you live: the more they make.

Situations Where Reverse Mortgages Might Make Sense

If you are 85 years old: have no children: and want to stay in your home until the end: the math is great. You likely won’t outlive the equity. It also works as a “standby” line of credit. You can open the loan: pay the upfront fees: and then never touch the money unless there is a true emergency. Since interest only accumulates on the money you actually spend: an untouched line of credit can be a powerful insurance policy.

Situations Where Reverse Mortgages Are Usually a Bad Idea

If you plan to move in three years: don’t do it. The $15,000 in upfront fees will make your “cost of money” about 50% for those three years. It is also a terrible idea if you have a younger spouse who is not on the loan. If the older spouse dies: the younger one could be forced out of the house. Always: always make sure both spouses are “borrowers” on the contract.

Safer Alternatives to Consider

Before you sign your life away to a compounding interest machine, consider these logic-driven alternatives that preserve more of your net worth:

- The “Right-Size” Strategy (Downsizing): This is the ultimate first-principles move. If you sell your $650,000 family home and buy a $400,000 modern condo, you net $250,000 in cash. Unlike a reverse mortgage, this money is truly yours—there is no interest compounding against it, and your monthly utility and maintenance costs will likely drop by 30% or more.

- 2026 Property Tax Deferral Programs: Many states and counties have significantly expanded “Senior Tax Freezes” or deferral programs in 2026. These allow you to delay paying property taxes until the home is sold. Since property taxes often make up 25% of a senior’s housing cost, this provides immediate cash flow relief without the $15,000 upfront fees of an HECM.

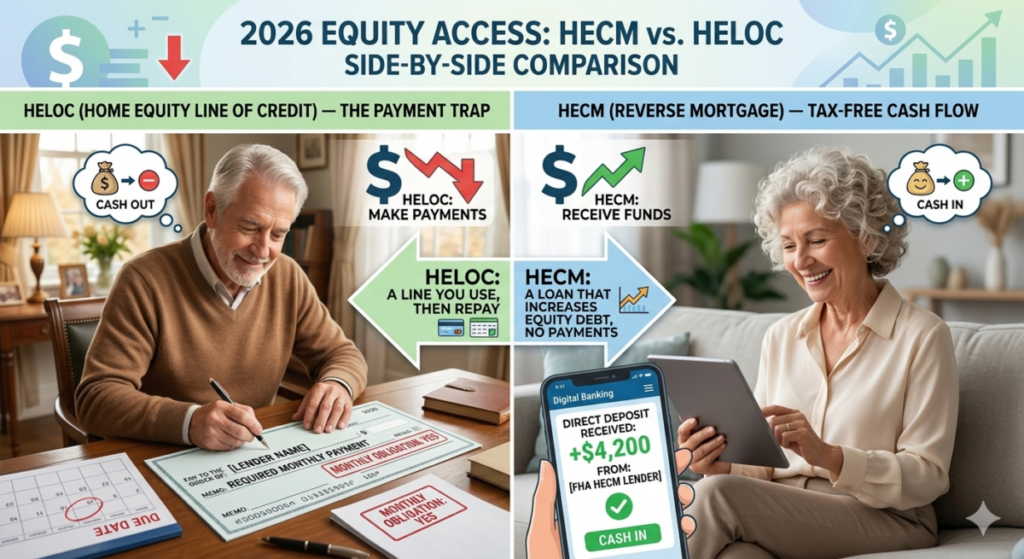

- Standard HELOC (Home Equity Line of Credit): If you still have a steady income or a solid pension, a HELOC is much cheaper to set up (often costing less than $500 in 2026). You only pay interest on what you actually borrow. The catch? You must make monthly payments. If you can handle the payment, you save tens of thousands in compounding interest compared to a reverse mortgage.

- Intra-Family Loans (The “Private” Reverse Mortgage): If you have heirs who want the house, have a blunt conversation with them. They can “loan” you the monthly income you need in exchange for a larger share of the home’s eventual sale price. This keeps the interest “in the family” rather than handing it to a bank.

- The 2026 “House-Hacking” Move: With the 2026 housing shortage still in full swing, renting out a room or a finished basement can generate $800 to $1,200 in monthly income. This is “active” equity—it solves your cash flow problem without touching your home’s title or incurring a penny of debt.

How to Evaluate a Reverse Mortgage Safely: Your Checklist

Don’t let the glossy brochures fool you. Evaluating a reverse mortgage requires a cold, first-principles approach to your net worth. Use this checklist to ensure you aren’t being taken for a ride:

- Verify the 2026 Lending Limit: Check your home’s value against the 2026 FHA HECM limit of $1,249,125. If your home is worth $1.5 million, remember that the bank will ignore every penny above that cap when calculating your cash.

- Request the “Total Cost of Loan” (TALC) Rate: Every lender is required to provide a TALC disclosure. This shows the annual average cost of the loan, including all those upfront fees and compounding interest. If the TALC is over 10%, you are likely overpaying.

- Identify Your “Heir Strategy”: Have a blunt conversation with your family. If your children want to keep the house, a reverse mortgage is a massive hurdle. Heirs must pay off the loan (or 95% of the appraised value) within 6 to 12 months of your passing. Do they have the cash or credit to do that?

- Check the “Margin” on Variable Rates: Most 2026 reverse mortgages are variable. Ask the lender: “What is the margin?” If the index (like SOFR) is 5% and the margin is 3%, your total rate is 8%. You want the lowest margin possible to slow the “equity bleed.”

- Audit Your “Required Repairs”: Before you pay for an appraisal, walk your property. Fix peeling paint, sagging gutters, or broken windows now. FHA appraisers in 2026 are strict; they will hold back your funds in a “repair set-aside” if the house isn’t up to code.

- Interview Three HUD Counselors: Don’t just go with the counselor the lender recommends. Find your own through the HUD website. Ask them specifically about the Life Expectancy Set-Aside (LESA) and whether your credit history will trigger one.

- Run a “10-Year Equity Projection”: Ask the lender for a table showing your estimated home equity in 2036. If the table shows “Zero Equity” by year 10, you are effectively choosing to spend your entire legacy during your lifetime.

Final Thoughts: A Powerful Tool — But Not for Everyone

Look: I have been in this game a long time. I have seen reverse mortgages save people from bankruptcy: and I have seen them leave families with nothing. It is a tool: like a hammer. You can build a house with it: or you can smash your thumb.

In 2026: the math is harder because of higher rates. If you need more info: check out our guide on 2026 Downsizing Strategies or read about Senior Property Tax Relief. For more on the technical side: see our Equity Protection Plans.

Final Takeaway: Never treat a reverse mortgage as “free money.” It is a debt that compounds. If you don’t understand the math: don’t sign the paper.

About the Author: Charles O’Dell

Prior to 23 years of experience and 100+ successful property flips, Charles was a practicing CPA and financial advisor. Charles O’Dell is the founder of HousingAfter60.com. Charles focuses on the financial mechanics of aging in place. He cuts through the emotional noise to help retirees make logic-driven decisions about their largest asset—their home. He holds a firm belief that equity is the only thing standing between a comfortable retirement and the mercy of the state.

Written by Charles O’Dell: 23+ years of real estate experience and 100+ successful property flips.