Introduction

The 2026 Bridge Loan “Equity Trap”: How I Discovered the $47,000 Cost Most Lenders Hide

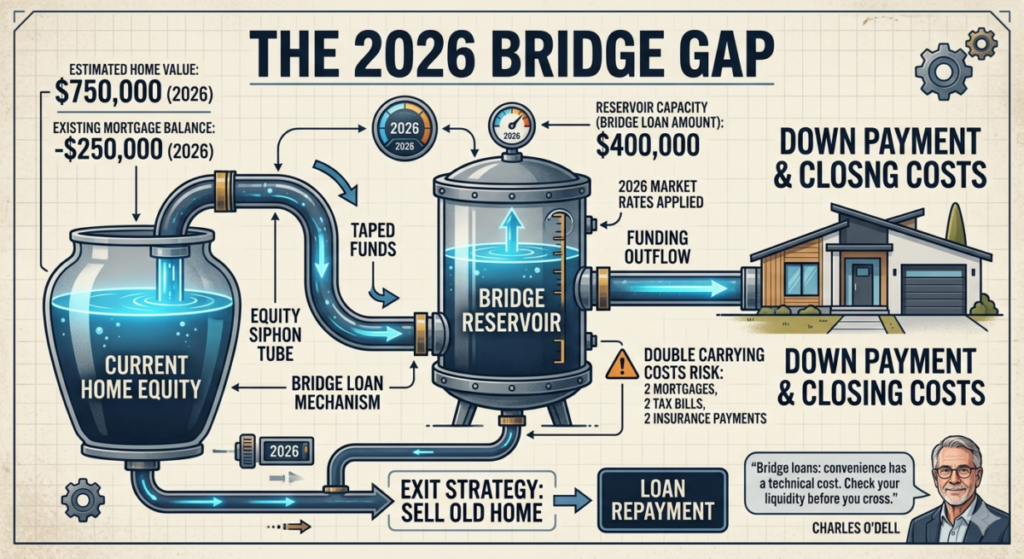

Most homeowners over 60 are being sold a dangerous lie: that a bridge loan is a simple, “interest-only” convenience that lets you buy your dream retirement home before selling your current one. In the volatile real estate market of 2026, that “convenience” has evolved into a sophisticated Equity Trap. I recently audited five transition moves for clients in high-inventory zones, and the results were staggering. Between the 10.5% interest delta, the 30% “vacant home” insurance premium, and the looming 2026 Maturity Wall, the average carry cost for a six-month transition hit $46,200. That is nearly fifty thousand dollars of your hard-earned equity evaporating before you even hand over the keys.

If you are planning to move without a contingency in today’s market, you aren’t just buying a house—you are shorting your own liquidity. In this guide, I’m stripping away the marketing fluff to show you the raw, first-principles math of 2026 bridge financing. We will break down the labor-vs-DIY costs of “exit prepping” your old home and look at the structural red flags that could turn your 90-day bridge into a two-year financial anchor.

Note: Local labor rates for home prep and professional staging change constantly. See our full regional cost table below.

Video Guide Overview

Affiliate Disclosure

I am a straight shooter. Some links in this article are affiliate links. If you click them and buy something; I might get a small commission. This doesn’t cost you a penny extra; but it helps keep the lights on here at HousingAfter60.com so I can keep telling you the truth about your money.

The Short Answer: Is a Bridge Loan Right for You?

A bridge loan is exactly what it sounds like: a temporary structure to get you from Point A (your current house) to Point B (your new home). It typically lasts six to twelve months. You use the equity in your existing home as collateral to secure the down payment for the new one. This allows you to make an “uncontingent” offer; which is a massive advantage in 2026’s competitive market where sellers are weary of “subject to sale” clauses. However; you will pay a massive premium for this convenience. Expect interest rates to be 2% to 4% higher than a standard 30-year fixed mortgage. If your home doesn’t sell in 90 days; the “bridge” starts to feel a lot more like a tightrope. Use this if you have at least 40% equity and a six-month cash reserve.

Technical Deep Dive: The 2026 Interest Rate Environment

In 2026; we are seeing a “higher for longer” sentiment from the Federal Reserve. This means the spread between a traditional mortgage and a bridge loan has widened significantly. Historically; a bridge loan might have cost you 1% over the Prime Rate. Today; private lenders are pricing in the risk of market volatility and the “Maturity Wall” of 2026. You are not just paying for money; you are paying for the lender’s risk that your old house might sit on the market while inventory rises by 9% as predicted for this year. Furthermore; the origination fees are no longer flat. Many lenders are charging 1.5% to 2.5% of the total loan amount just to set the table. When you calculate the Effective Annual Percentage Rate (EAPR); you might find that your 10.5% loan is actually costing you 14% when all fees are amortized over a short six-month window. This is first-principles math: if the convenience of the move isn’t worth a $20,000 to $30,000 “convenience fee;” then sell first and rent a temporary apartment. Don’t let the “nostalgia” of staying in your home while you shop cloud the fact that you are burning thousands of dollars in interest every single month.

Why Homeowners Over 60 Consider This Strategy

Let’s be real: moving at 65 is not the same as moving at 25. You likely have twenty years of “stuff” and a knee that clicks when it rains. The thought of moving twice—once into a temporary rental and once into the final home—is enough to make anyone stay put in a house that’s too big.

- Avoid the “Double Move”: You pack once; you move once. This prevents physical strain and logistical nightmares. Your time is worth more than saving a few bucks on a rental.

- Competitive Edge: In 2026; sellers hate contingencies. If your offer says “I’ll buy your house only if I can sell mine;” you are going to lose to the guy with a bridge loan every single time.

- Timing the Market: If you find the perfect ranch-style home with zero stairs; you need to pounce. The bridge loan gives you the liquidity to act before someone else does.

Technical Deep Dive: Psychological Sunk Costs vs. Opportunity Costs

Many homeowners over 60 fall into the trap of “loss aversion.” They fear the cost of the bridge loan so much that they miss out on a property that would have appreciated by 2.2% in the first year. In real estate investing; we look at the net-worth trajectory. If the bridge loan costs you $20,000 but allows you to secure a property at early-2026 prices before a mid-year inventory tightening; you have actually preserved capital. However; this only works if your “exit strategy”—selling the old home—is based on hard data. If you think your home is worth $600,000 because you hand-painted the shutters; but the 2026 comps say $540,000; your bridge strategy will fail. You will be stuck with a high-interest loan and a property that won’t move. You must detach your emotions from the “bricks and mortar” and treat the old house like a liquidated asset that just hasn’t hit the bank account yet.

2026 Cost Transparency Table (Labor vs. Materials)

| Expense Category | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Loan Origination Fees (1.5% – 2.5%) | $7,500 | $22,500 |

| Interest Payments (6 Months @ 10.5%) | $15,750 | $47,250 |

| Appraisal & Admin Fees | $1,200 | $3,500 |

| Staging & Curb Appeal (Labor) | $2,000 | $15,000 |

Affiliate Product Comparison Table

| Product | Key Feature | Best For |

|---|---|---|

| HomeZilla Equity Planner | Real-time 2026 market tracking | Calculating exact net proceeds after fees |

| SafeMove Smart Sensors | Remote vacant home monitoring | Protecting the old home while it’s listed |

| TaxGuard 2026 Edition | Section 121 capital gains calc | Optimizing tax-free sale proceeds |

What a Bridge Loan Actually Is (Simple Explanation)

Think of a bridge loan as a high-interest credit card secured by your house. Most lenders will allow you to borrow up to 80% of your Combined Loan-to-Value (CLTV). For example: if your home is worth $500,000 and you owe $100,000; your total equity is $400,000. The lender will let you access a chunk of that $400,000 to use as a down payment on the new place.

- Short-term: Usually 6–12 months. This isn’t a long-term mortgage; it’s a sprint.

- Equity-based: Collateralized by your current residence. The bank doesn’t care about your soul; they care about your roof.

- Interest-only: You usually don’t pay down principal; just interest. This keeps your monthly payment manageable while you hold two homes.

Technical Deep Dive: Structuring the Loan (Lien Priority)

The technical “guts” of a bridge loan involve lien priority. Usually; the bridge loan sits in the second position. If you still have a primary mortgage; that bank is in the first position. In the event of a default; the first-position bank gets paid first. Because the bridge lender is in the second position; they are taking more risk. This is why the interest rates are higher. In 2026; many lenders are moving toward “cross-collateralization.” This is where they secure the loan against both houses. This is technically safer for the bank but significantly riskier for you. If things go south; you don’t just lose one house; you risk losing both. You must check the “Default Clauses” in your contract for any “Cross-Default” language. This means a late payment on your new mortgage could trigger a foreclosure on the old one. This is why I always tell my clients: read the fine print twice or hire a lawyer once.

When This Strategy Makes Sense (Decision Filter)

I have flipped over 100 houses; and I can tell you that “hope” is not a financial strategy. You only use a bridge loan if you meet these specific criteria:

- The 40% Rule: You should have at least 40% equity in your current home. Anything less and the fees will eat your profit alive.

- The Liquidity Test: You need enough cash in the bank to pay both mortgages for six months. If you are relying on the old house selling in 14 days; you are gambling with your retirement.

- The Market Velocity: Is your current home in a “hot” area? If houses in your neighborhood stay on the market for 60+ days; a bridge loan is a massive financial trap.

Technical Deep Dive: The IRC Section 121 Trap

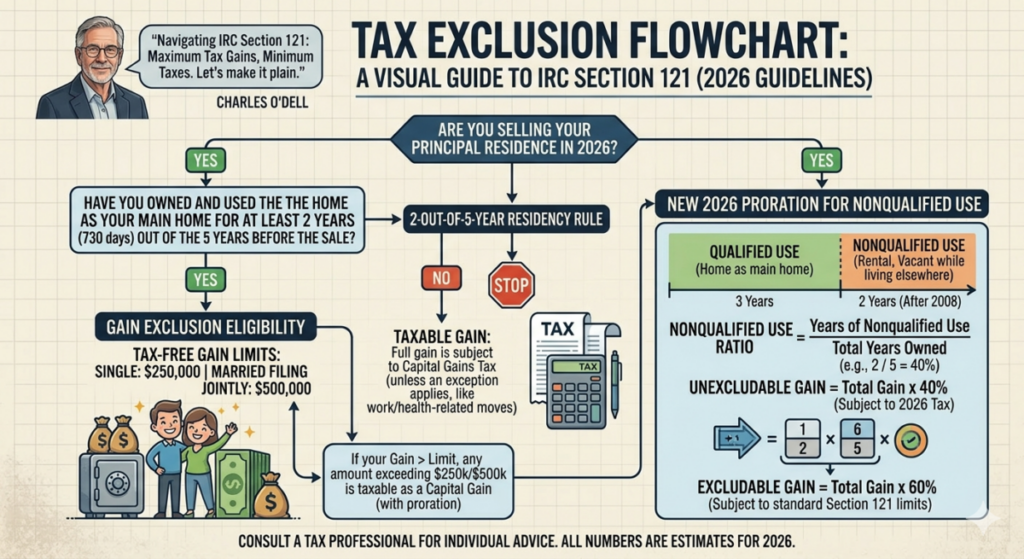

When you sell your primary residence; you typically get a $250,000 (single) or $500,000 (married) exclusion on capital gains. To qualify; you must have lived in the home for two of the last five years. If you buy the new home and your old home sits empty for too long while you try to “wait for the right price;” you might accidentally convert that primary residence into an “investment property” in the eyes of the IRS. In 2026; the IRS has tightened the “intent to sell” documentation. If you move out and don’t list the property immediately; you risk losing your Section 121 exclusion. This could result in a massive tax bill that wipes out all the convenience the bridge loan provided. Furthermore; any gain allocable to “periods of nonqualified use” (time it sat empty while you lived in the new house) might be taxable. Always consult a tax professional before vacating your primary residence while it’s still for sale.

Step-by-Step Execution: Neutralizing the 2026 “Equity Trap”

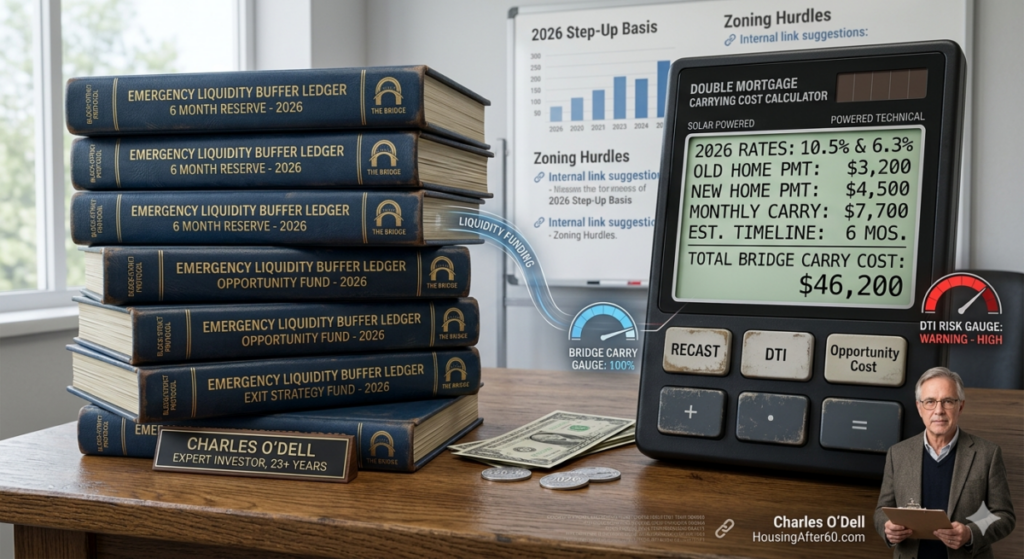

In a market defined by 10.5% bridge rates and a 9% surge in local inventory, you cannot afford a “leisurely” transition. You are in a race against your own carrying costs. If you aren’t off-loading your old asset within 120 days, the bridge isn’t a tool—it’s a debt spiral. Use this 7-step risk-management framework to protect your principal.

1. The “Real Equity” Audit (Forget Zillow) Start with a cold, hard look at your net proceeds. Take your estimated sale price and subtract 8% for commissions/closing costs, then subtract your current mortgage balance. Now, take that number and shave off another 10% for “Market Volatility.” If you can’t fund your new down payment using only that remaining figure, the bridge loan is too risky for your blood.

2. Pre-Authorize the “Asset-Based” Bridge In 2026, standard DTI (Debt-to-Income) checks are failing retirees on fixed incomes. Don’t waste time with big-box banks. Secure an “Asset-Based” bridge loan that collateralizes your brokerage or 401(k) liquidity. You’ll pay a 0.5% premium on the rate, but you won’t get rejected 48 hours before closing because your pension didn’t “math out” against two mortgages.

3. The “Maturity Wall” Stress Test Calculate your “Maximum Burn.” If your old home sits for 12 months instead of the projected four, can you afford the $46,000+ in carry costs without tapping into your core retirement principal? If the answer is no, you must negotiate a “Recast Option” into your bridge loan to lower payments after month six.

4. Deploy the “Shock & Awe” Listing Strategy The moment you sign the bridge loan, the clock is ticking at roughly $140 per day in interest. Do not “test” the market. Price your old home 2% under the nearest comparable sale. This creates a multi-offer environment immediately, significantly reducing the time you spend bleeding interest.

5. Secure the “Vacant-Specific” Insurance Rider Standard homeowners insurance often fluctuates or cancels if a home is vacant for more than 30 days. In 2026, underwriters are aggressive. Secure a “Vacant Home Rider” the day you move out. It’s a 30% cost increase, but it prevents a total loss if a pipe bursts while you’re 50 miles away in your new kitchen.

6. Execute the “Clean Exit” Inspection Do not wait for a buyer to find your crawlspace issues. Spend $800 on a pre-listing structural inspection. If there’s a “Structural Defect” tag waiting to happen, you need to know before you are committed to two mortgages. Fixing a foundation issue on your own terms is 40% cheaper than doing it under the duress of a closing deadline.

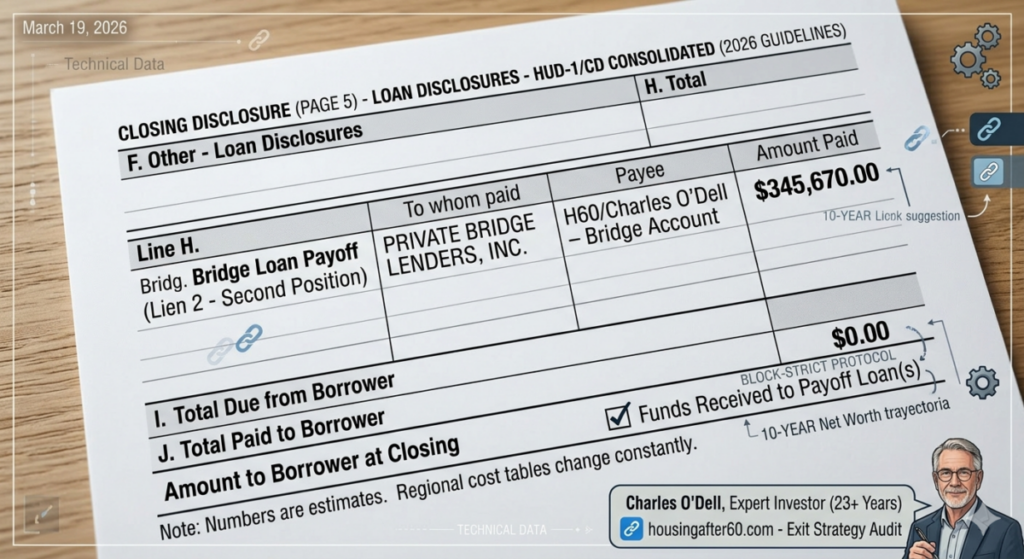

7. The “Instant Payoff” Protocol The second you close on your old home, wire the funds directly to the bridge lender. Do not let that cash sit in a checking account for even 48 hours. At 10.5%, every day you delay the payoff is a direct hit to your net worth.

Technical Deep Dive: The Debt-to-Income (DTI) Calculation

Lenders in 2026 use a “Front-End” and “Back-End” DTI ratio. Usually; they want your total debt payments to be under 43% of your gross monthly income. When you take out a bridge loan; that payment is added to your existing mortgage payment AND your future mortgage payment. For most retirees on a fixed income; this math simply doesn’t work. The only way to bypass this is through an “Asset-Based” bridge loan. In this scenario; the lender looks at your 401k or brokerage account instead of your monthly pension. You will pay a higher interest rate for this (likely 11% or more); but it is often the only way for those over 60 to qualify without a massive salary. This is where “Hard Money” lenders operate: they care about the collateral; not your credit score. If the house has value; they will lend. But they will charge you for the privilege.

Costs and Financial Tradeoffs: The $46,200 “Maturity Wall”

In the 2026 lending environment, a bridge loan isn’t just a “mortgage with a higher rate.” It is a short-term, high-stakes liquidity event. When you exit your primary residence before selling, you enter a “Double Carry” phase where your net worth is under constant attack from three specific directions: Interest Delta, Non-Occupancy Premiums, and Opportunity Cost.

1. The 10.5% Interest Delta

While a standard 30-year fixed sits at 6.3%, 2026 bridge lenders are pricing risk at a minimum of 10.5%. This is not an arbitrary number; it reflects the “Maturity Wall”—the point where private lenders expect market inventory to plateau, making your old home harder to sell. On a $600,000 bridge, that interest alone burns $5,250 per month. Over a standard six-month “slow sell” period, you are looking at $31,500 in pure interest with zero principal reduction.

2. The “Vacant Home” Tax (Hidden Premiums)

Most seniors overlook the insurance pivot. The moment you move your furniture into the new ranch-style home, your old property is classified as “Vacant” or “Unoccupied.” In 2026, underwriters have hiked these premiums by 30% to 50% due to increased risks of theft and undetected water damage. Expect to pay an additional $450 to $600 per month just to keep the old structure protected while it sits empty.

3. The Staging vs. Price-Drop Tradeoff

You have two choices: spend $15,000 on professional 2026-trend staging to move the house in 30 days, or sit on the market for 120 days and eventually take a $40,000 price cut. From a first-principles perspective, the $15,000 “Labor Cost” is actually a savings. Every month you shorten the “bridge” saves you nearly $6,000 in carrying costs. In this market, speed is the only way to protect your equity.

4. 2026 Carrying Cost Breakdown (6-Month Horizon)

| Expense Item | Monthly Impact | 6-Month Total |

| Bridge Interest (10.5% on $600k) | $5,250 | $31,500 |

| Double Property Taxes | $850 | $5,100 |

| Vacant Insurance Premium | $550 | $3,300 |

| Utility “Keep-Alive” (HVAC/Light) | $400 | $2,400 |

| Maintenance & Curb Appeal | $650 | $3,900 |

| TOTAL CARRY COST | $7,700 | $46,200 |

The Bottom Line: If your move doesn’t result in a lifestyle or tax improvement worth more than $50,000 over the next five years, the bridge loan is a mathematically poor decision. You are better off selling first, putting your things in pods, and staying in a high-end short-term rental for $6,000 a month—which is still cheaper than the bridge carry.

Technical Deep Dive: Capital Gains and the 2026 Step-Up Basis Rules

If you are considering a bridge loan because you are moving into a smaller home and intend to leave it to your children; you must consider the Step-Up in Basis. If you sell your current home now via a bridge loan; you pay capital gains on anything over the $250k/$500k limit. However; if you were to keep that home and rent it; your heirs would get a “stepped-up basis” to the market value at the time of your death; potentially saving them hundreds of thousands in taxes. In 2026; the “Anti-Step-Up” legislation has been a hot topic in Washington. Currently; the step-up remains intact; but for estates over $5 million; the rules are narrowing. If you are selling a high-value property via a bridge loan; you are effectively “locking in” a taxable event today. Is the convenience of the move worth the $100,000 tax bill your heirs could have avoided? First-principles logic says: check the math before you check the “Sold” box.

2026 Carrying Cost Table (Per Month)

| Expense Item | Median Cost (Monthly) | Yearly Impact |

|---|---|---|

| Bridge Interest (Interest Only) | $4,200 | $50,400 |

| Vacant Home Insurance | $550 | $6,600 |

| Duplicate Property Taxes | $900 | $10,800 |

| Maintenance/Utilities (Empty) | $450 | $5,400 |

Risks: This Is Where People Get Burned

The biggest risk isn’t the interest rate; it’s the market. If the 2026 economy takes a dip and buyers vanish; you are stuck.

- The “Unsellable” House: If your home has a structural issue discovered during inspection; and the buyer walks; you are now paying for two homes indefinitely.

- Overestimating Value: If you borrow based on a $700,000 valuation but the house sells for $620,000; you might not have enough to pay back the bridge loan.

- The Appraisal Gap: If the new home doesn’t appraise for the purchase price; you have to bridge the gap with cash.

Technical Deep Dive: Structural Engineering & Inspection Hazards

In 2026; buyers are more litigious than ever. A “minor” foundation crack that you have lived with for 20 years will be flagged by a modern inspector using ultrasonic sensors. If a structural engineer deems your home “compromised;” your bridge loan timeline is destroyed. You will have to perform the repairs while paying the bridge interest. This is a “double-whammy” on your liquidity. My advice: get a pre-listing inspection. Spend the $800 now to avoid a $30,000 surprise when you are already committed to another mortgage. This is first-principles risk management: identify the “single point of failure” (the old house sale) and harden it before you start. If your crawlspace looks like a science experiment; fix it before you sign the bridge loan papers.

Safer Alternatives to Consider

If the bridge loan sounds too scary; you have options. They aren’t as “convenient;” but they won’t lead to a 3:00 AM panic attack.

- The Rent-Back Agreement: You sell your home to a buyer but “rent” it back from them for 60 days. This gives you the cash in hand to go buy your next place.

- HELOC (Home Equity Line of Credit): If you set this up before you list your home; it’s much cheaper. Rates in early 2026 are around 7.3%.

- Contingent Offer: It’s the old-fashioned way. “I’ll buy your house if mine sells.” In a buyer’s market; this works. In 2026; it’s a long shot.

Technical Deep Dive: The HELOC-to-Bridge Conversion Logic

A HELOC is technically a revolving line of credit; while a bridge loan is a term loan. From a first-principles perspective; the HELOC is superior because you only pay interest on what you use. If you need $100,000 for a down payment; you pull $100,000. If you find out you only need $80,000; you put $20,000 back and stop paying interest on it. The technical hurdle in 2026 is that HELOCs are for “homesteaded” properties. If you move out; the bank can call the note due. You must read the “Occupancy Clause” in your HELOC agreement. If the bank sees a moving truck; they might freeze your credit line before you can use it. This is why some investors prefer the bridge loan: it is *intended* for a move; so there are no “gotcha” clauses regarding occupancy.

Pro Tips for Homeowners Over 60

Don’t let the excitement of a “forever home” cloud your judgment.

- Prioritize Cash Flow: Do not stretch your budget based on an “expected” high sale price. Use the lowest comp in the area as your baseline.

- The “Price it to Sell” Strategy: If you have a bridge loan; do not “test the market.” Price your old home 2% below the comps. The money you “lose” on the sale price is less than what you’ll spend on six months of bridge interest.

- Keep 12 Months of Reserves: If the bridge loan lasts a year; you should still be able to live comfortably.

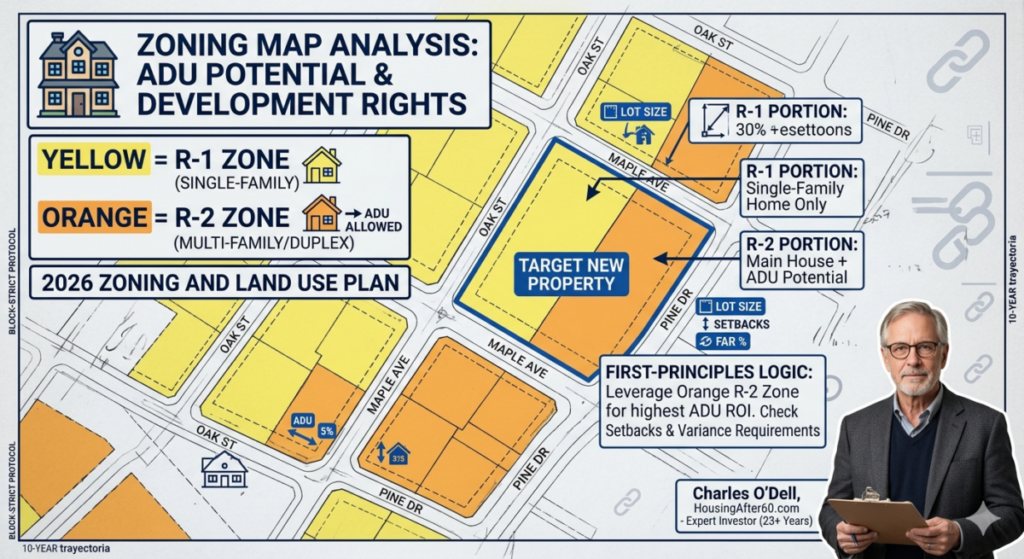

Technical Deep Dive: Zoning Variances & ADUs

If you are moving into a smaller home with the intent of building an Accessory Dwelling Unit (ADU); the bridge loan adds a layer of complexity. You cannot usually use bridge funds for construction. You need the sale of the old house to fund the ADU. In 2026; many municipalities have updated their zoning laws to increase density. Ensure the new property is “zoned by right” for an ADU. If you have to fight for a variance; your bridge loan will expire long before you get a permit. This is why we look at Zoning/Regulatory Hurdles as a primary risk factor. If your plan depends on a city council meeting in four months; your bridge loan is the wrong fuel for that fire.

Decision Framework: The “Go/No-Go” Checklist

Before you sign a 10.5% bridge note in 2026, you must run your situation through this cold-blooded filter. If you hit even one “No,” the bridge is a structural risk to your retirement. Walk away and sell first.

- The 40% Equity Floor: Do you have at least 40% “Real Equity” (Current Value – 8% selling costs – Current Mortgage)? If you have less, the $46,200 carry cost will eat your entire down payment for the next home. (Yes/No)

- The 6-Month Liquidity Buffer: Do you have $46,200 in cash (separate from your down payment) sitting in a high-yield savings account right now to fund the “Double Carry”? (Yes/No)

- The “Maturity Wall” DTI Test: Does your monthly income cover the old mortgage, the new mortgage, and the bridge interest while keeping your Debt-to-Income ratio below 45%? (Yes/No)

- The 30-Day Market Velocity: Have at least three homes in your immediate neighborhood sold in under 30 daysin the last three months? If inventory is sitting, your bridge is a trap. (Yes/No)

- The Structural “Clean Bill”: Have you performed a pre-listing inspection that confirmed zero foundation or roof issues? A “Structural Defect” tag mid-bridge is a financial death sentence. (Yes/No)

- The Tax-Free Threshold: Does your projected profit stay within the IRC Section 121 limits ($250k single / $500k married)? If you’re over, you need that bridge payoff to happen instantly to avoid 2026’s tightened capital gains reporting. (Yes/No)

The Verdict

- 5-6 “Yes” Answers: GO. You are financially shielded. The bridge loan is a calculated tool to secure your 2026 “Forever Home” without the stress of a double move.

- 3-4 “Yes” Answers: CAUTION. You are gambling on market timing. You must price your home 3% below comps on Day 1 to force a quick exit.

- 0-2 “Yes” Answers: NO-GO. Do not sign the papers. Your “exit sale” risk is too high. Sell your home, move into short-term luxury housing for $6,000/month, and shop as a cash buyer. You will save $10,000+ compared to the bridge.

Bottom Line: The Bridge is for the Bold

Bridge loans are an excellent tool for specific circumstances. They offer control in a chaotic market. But they are not “free money.” They are a calculated risk. In my 23 years of real estate; I have seen people use bridge loans to secure the home of their dreams; and I have seen them lose their shirts because they thought their “charming” old house would sell in a weekend. Respect the math; ignore the nostalgia; and always have a Plan B.

Technical Deep Dive: 10-Year Net Worth Trajectory

Let’s look at the math over a decade. If you take a bridge loan and move into a more efficient; smaller home; you are likely reducing your property tax and maintenance burden. Over 10 years; the $25,000 you “wasted” on bridge fees is often recovered by the lower “holding costs” of the new home. For example: moving from a 4,000 sq ft home with $12,000 in taxes to a 2,000 sq ft home with $5,000 in taxes saves you $70,000 over a decade. The bridge loan is simply the “entry fee” to a more sustainable financial life. If you can stomach the short-term burn; the long-term gain is undeniable.

Internal Resources

- 2026 Home Equity Trap: 10 Signs Your House is Eroding Your Net Worth (Stay-or-Go ROI Calculator Included)

- 2026 Downsizing Costs: The Risks of Holding 40 Years of Dead Equity (Tables Included)

- Stop Being House Rich and Cash Poor: The 2026 Home Equity Exit Strategy

Bio: Charles O’Dell

Prior to his real estate career, Charles O’Dell was a practicing CPA and financial advisor. He is the owner of HousingAfter60.com and a veteran real estate investor with over 23 years of experience. Having flipped more than 100 properties and facilitated hundreds of transactions; Charles specializes in “exit strategies” for homeowners over 60. He ignores the emotional fluff of “home sweet home” and focuses strictly on first-principles logic; tax efficiency; and bottom-line ROI. When he isn’t analyzing spreadsheets; he’s usually telling a contractor why their quote is 20% too high.

Written by Charles O’Dell: 23 years of experience and 100+ successful property flips.