Article Summary: Owning a condo after 60 isn’t “maintenance-free”: it is “responsibility-shifted.” While you stop mowing lawns, you start funding massive commercial-grade roof projects and elevator overhauls. To find the true Total Cost of Ownership (TCO) in 2026, you must calculate the mortgage, HOA dues, special assessment risk, and internal maintenance reserves. Most buyers ignore the fact that HOA fees historically outpace inflation by 3% annually. This guide provides the hard math to ensure your retirement isn’t derailed by a poorly managed building.

Condo Trap

The “Short” Answer

Is a Condo Actually Cheaper? In 2026, the short answer is: No, it is rarely “cheaper” than a well-maintained house; it is simply more predictable until it isn’t. While you save on individual line items like landscaping, roofing, and exterior painting, you trade those for monthly HOA dues that typically increase by 3% to 7% annually. The “real” cost of a condo includes your mortgage, taxes, insurance, and a mandatory 1% maintenance reserve for interior repairs.

The “deal-breaker” cost is the Special Assessment. If the building’s reserve fund is under 50% funded, you are effectively sitting on a debt bomb. A condo is a winning move if you value lifestyle and time over total control and equity growth. However, if your goal is the lowest possible monthly burn rate, a condo with high amenities and aging infrastructure is a financial trap. Calculate your TCO by adding a 15% “Risk Buffer” to the advertised monthly fees.

Affiliate Disclosure: I’m a straight shooter. To keep the lights on here at HousingAfter60.com and continue providing deep-dive data, some of the links in this article are affiliate links. This means if you click one and buy a tool or service I recommend, I might earn a small commission at no extra cost to you. I only recommend hardware and tech that I’ve personally vetted in the field or used in my own 100+ property flips. My reputation is worth more than a referral fee, so if it’s on this list, it’s because it actually works.

Note: Local labor rates for Condo Maintenance change constantly. See our full regional cost table below.

I. Condo Trap: Why Condo Costs Are Often Misunderstood

I have spent over two decades in the real estate trenches. I have flipped houses that were falling down and managed condos that looked like five-star resorts on the outside but were financial disasters on the inside. Many retirees come to me and say, “I’m tired of the yard. I want a condo so my costs are fixed and simple.”

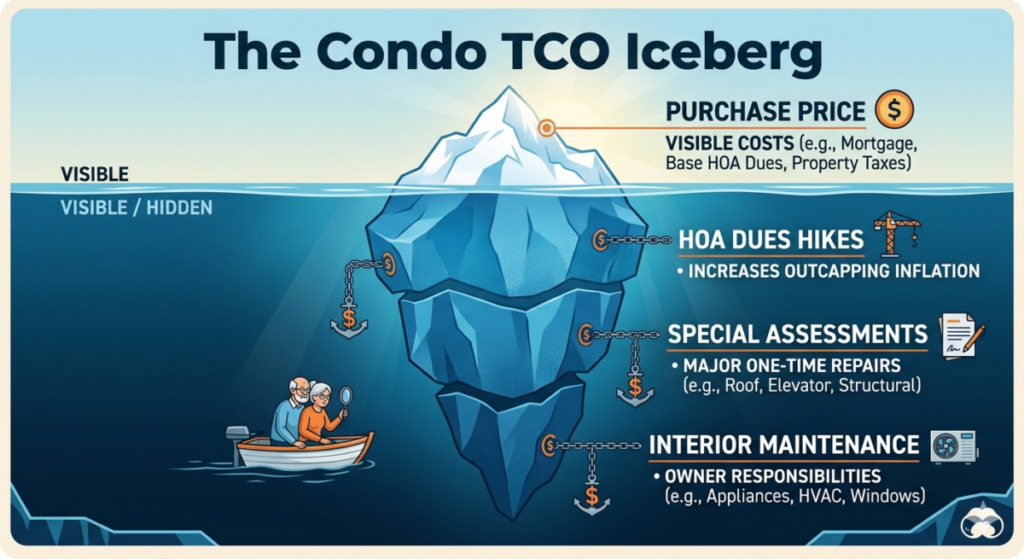

I usually laugh. Not a mean laugh; just the laugh of a man who knows that “simple” is often a marketing term for “somebody else’s problem that you are paying for.” Real estate costs are never eliminated; they are merely shifted. In a single-family home, you decide when to fix the roof. In a condo, a board of five people you might not even like decides when you are going to spend $25,000 on a new parking garage. Total Cost of Ownership (TCO) is the only metric that matters. It combines your purchase price, recurring fees, and the “ghost costs” of future repairs.

For those of us over 60, this math is vital. We are often on fixed incomes or drawing from a 401(k). We don’t have a 20-year runway to “earn back” a massive financial hit. If your condo fees double in five years—and in some parts of Florida and California, they have—your “relaxing” retirement becomes a math problem you can’t solve. We are going to use first-principles logic today to strip away the fluff and look at the raw numbers.

II. The Core Formula: What “Total Cost of Ownership” Really Includes

To calculate TCO, you can’t just look at the Zillow estimate. You need to look at four distinct buckets of money. First are the Monthly Fixed Costs: your mortgage, property taxes, and the current HOA dues. These are the easy ones. Second are the Variable Costs: utilities like electricity and the interior maintenance that the HOA doesn’t touch (like your water heater or dishwasher).

Third, and most dangerously, are the Risk-Based Costs. These are the special assessments. Think of these as the “boogeyman” of condo living. If the building needs a new chiller system for the AC and the reserve fund is empty, you get a bill. Finally, there is Opportunity Cost. If you put $400,000 cash into a condo, that money isn’t earning 5% or 7% in the market. That “lost” interest is a cost of living there.

Technical Deep Dive: 2026 Opportunity Cost Analysis

In the current 2026 economic climate, holding 100% equity in a condo has a significant Opportunity Cost of Capital (OCC). If you have $500,000 tied up in a primary residence, you are effectively “paying” the interest you aren’t earning. If a high-yield treasury is paying 4.5%, that condo is “costing” you $22,500 per year in lost income before you even pay a single HOA fee. When we compare this to renting or a leveraged mortgage, the 10-year net-worth trajectory often favors keeping some liquidity in the market rather than “parking” it in a depreciating 40-year-old building with rising fees.

III. Purchase Price Is Just the Starting Point

When you buy a condo, the bank looks at you differently than when you buy a house. They care about the building’s health just as much as your credit score. If the building has too many renters or not enough money in the bank, the loan is “non-warrantable.” This means you’ll pay a higher interest rate, often 0.5% to 1% more than a standard home loan. That adds up to thousands over a decade.

Don’t forget the HOA Transfer Fees. Some buildings charge a “capital contribution” at closing. This is basically a “welcome to the club” fee that can be two or three months of HOA dues paid upfront. It doesn’t go toward your equity; it goes into the building’s bank account to make up for the guy who didn’t pay his dues last year.

Cost Category

Low-End (DIY/Basic)

High-End (Pro/Premium)

Monthly HOA Dues

$300/mo

$1,200+/mo

Interior Maintenance Reserve

$100/mo

$450/mo

Special Assessment Buffer

$50/mo

$500/mo

Condo Insurance (HO-6)

$60/mo

$250/mo

IV. HOA Fees: The Biggest Ongoing Variable

HOA fees cover the stuff you don’t want to do: mowing the grass, cleaning the pool, and fixing the roof. However, in 2026, many HOAs are seeing double-digit increases. Why? Because the cost of raw materials (shingles, paint, concrete) and commercial labor has skyrocketed. If an HOA tells you their fees haven’t gone up in five years, run away. That means they are deferring maintenance, and a massive bill is coming for whoever owns the unit next (that’s you).

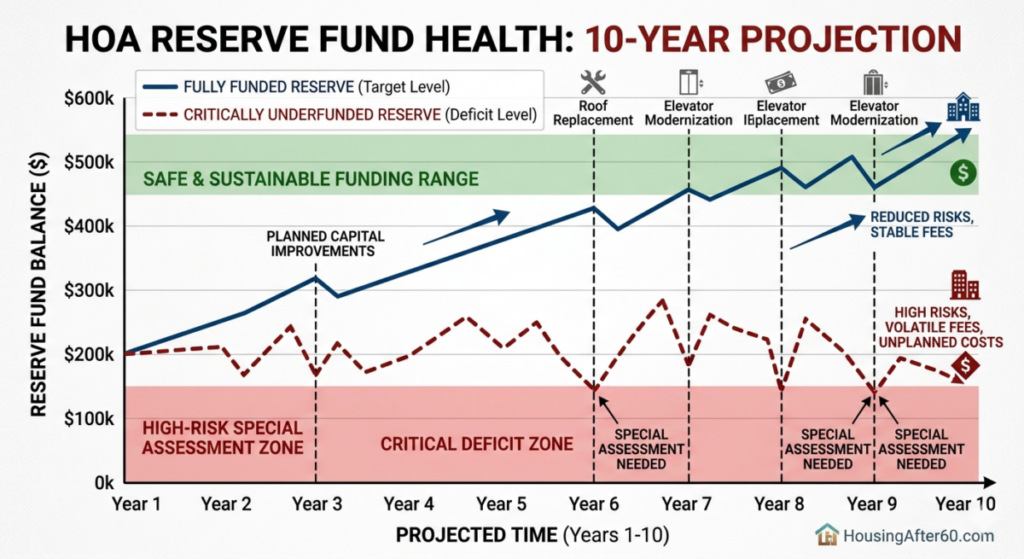

You need to check the Reserve Study. This is a professional report that predicts when the elevator will die and how much it will cost to fix. If the building needs $1 million in repairs over the next decade but only has $100,000 in the bank, guess where that other $900,000 is coming from? Your checkbook.

The Boardroom Battle

Technical Deep Dive: The Reserve Fund “Percent Funded” Logic

From a first-principles perspective, a condo association is a non-profit corporation where you are a shareholder. In 2026, “Fully Funded” (100%) is rare. Most healthy buildings sit at 70% or higher. If a building is under 30% funded, it is technically insolvent regarding its future obligations. This creates a “structural deficit.” As an investor, I look for the Cash Flow to Debt ratio of the HOA. If the association is using reserve funds to pay for daily operating expenses like landscaping, you are looking at a financial house of cards that will eventually collapse into a massive special assessment or a total loss of building insurability.

V. Special Assessments: The Cost That Breaks Budgets

A special assessment is a one-time fee charged to all owners to pay for a specific project. I’ve seen them range from $2,000 for a lobby makeover to $85,000 for structural balcony repairs. For a senior on a fixed income, an $85,000 bill is a life-altering event. It often forces a “fire sale” where the owner has to sell the unit at a massive discount just to get out from under the debt.

To predict these, you have to be a bit of a detective. Look at the windows. Are the seals blown? Look at the parking garage. Is there water dripping through the concrete? If the “bones” of the building look tired, the special assessment is already being drafted in a lawyer’s office somewhere. It’s not a matter of if; it’s a matter of when.

Punches through thick condo concrete walls for seamless Wi-Fi.

$450

VI. Insurance: More Complex Than It Looks

Condo insurance isn’t like house insurance. The building has a “Master Policy,” but that usually only covers the “studs out.” If your neighbor’s water heater leaks and ruins your $20,000 hardwood floors, the Master Policy won’t pay a dime. You need an HO-6 policy. In 2026, insurance rates for condos have climbed by 15% to 40% in many regions because the Master Policy deductibles have gone through the roof. If the building has a $100,000 deductible for wind damage, the HOA will likely assess every owner to pay that deductible if a storm hits. You need “Loss Assessment Coverage” in your personal policy to protect yourself from this.

VII. Maintenance: Not Eliminated—Just Different

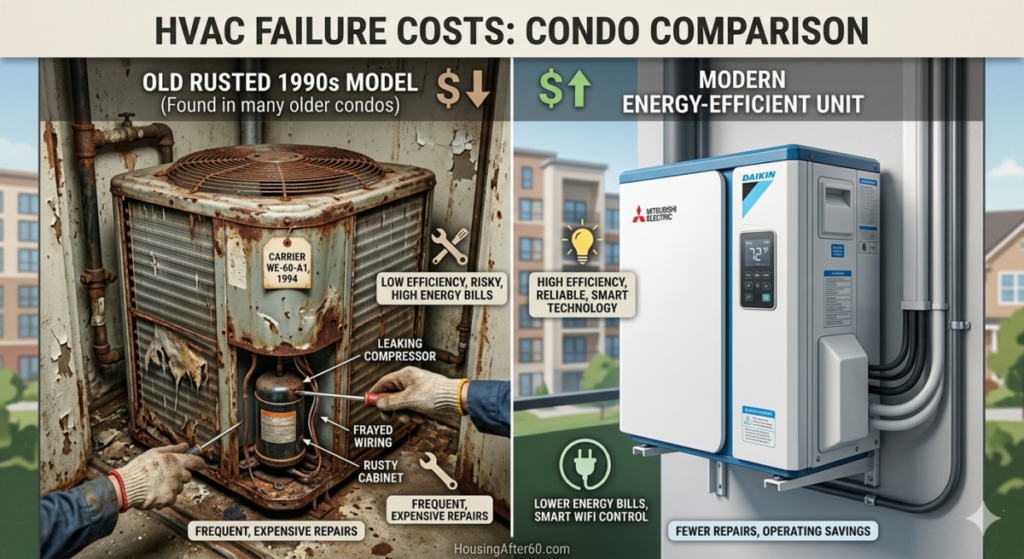

People think “condo” means “no more repairs.” Tell that to my client whose HVAC unit died in July. In a condo, your HVAC is often in a cramped closet or on a roof 20 stories up. Replacing it is more expensive than in a house because of the logistics. You might need a crane or specialized technicians who are “approved” by the HOA. You are still responsible for every pipe and wire inside your walls. If your toilet overflows and floods the three units below you, that is your financial burden, not the building’s.

HVAC Failure Costs

Technical Deep Dive: Structural Engineering & Deferred Maintenance

Under new 2026 safety mandates (following the tragic Surfside collapse in Florida years ago), structural integrity inspections are now mandatory in many states. This has changed the TCO math forever. Previously, boards could “ignore” concrete spalling or rebar corrosion to keep dues low. Now, engineers are legally required to report these issues. This creates a “Surge Cost” scenario where a 40-year-old building suddenly requires $5 million in structural reinforcement. If the building has 100 units, that is a $50,000 bill per resident. When buying, always ask: “Has the 2026 Milestone Inspection been completed and passed?” If the answer is “We’re working on it,” you are walking into a minefield.

VIII. Utilities and Services

Some condos include water and trash in the HOA fee; others don’t. In 2026, many buildings are installing individual sub-meters for water. They are tired of the little old lady in 4B paying for the family of five in 6C who takes hour-long showers. This is a good thing for low-usage seniors, but it adds another monthly bill to your TCO calculation. Also, check the building’s internet contract. Some HOAs force you to use a specific provider at a specific (often high) price.

The Reserve Study Graph

IX. Property Taxes and How They Change

Your property taxes are based on the value of your unit plus a portion of the common areas. For seniors, the good news is that many states offer Homestead Exemptions or Tax Freezes once you hit 65. However, you must apply for these; they aren’t automatic. If the condo building undergoes a massive renovation, the county might reassess the entire building’s value, causing your taxes to jump even if you didn’t touch a single thing inside your unit.

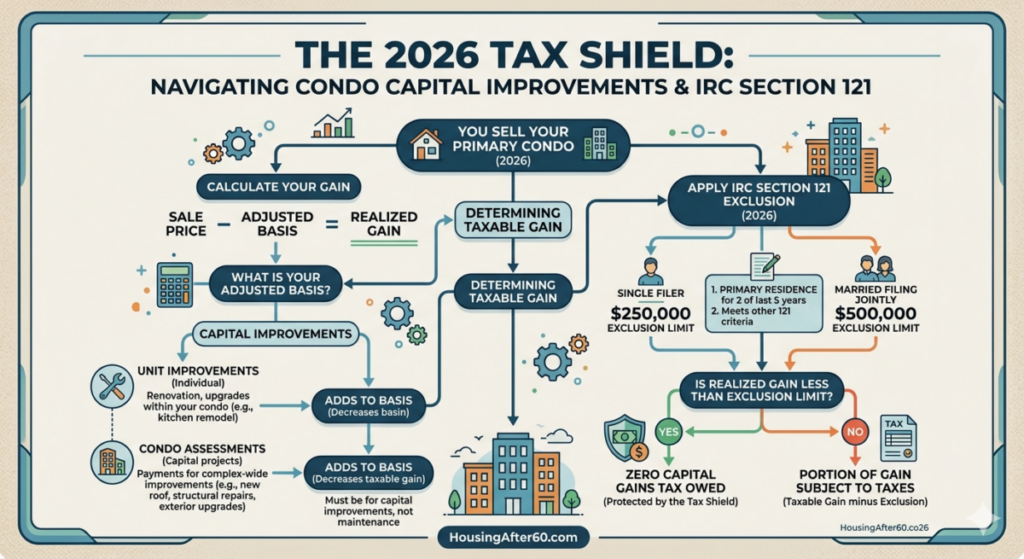

The 2026 Tax Shield

Technical Deep Dive: IRC Section 121 and Basis Adjustments

Under Internal Revenue Code Section 121, you can exclude up to $250,000 ($500,000 for married couples) of gain from the sale of your primary residence. But here is the 2026 kicker: many condo owners fail to track their Adjusted Basis. When you pay a special assessment for a capital improvement (like a new roof or structural repair), that amount is added to your cost basis. If you bought for $300k and paid $50k in assessments, your basis is $350k. This reduces your “taxable gain” when you sell. Most people lose this paperwork and end up overpaying the IRS. Keep every assessment receipt in a permanent file.

X. Resale Value and Liquidity Risk

Condos are the first things to lose value in a recession and the last things to gain it back. Why? Because you aren’t just selling your unit; you are selling the reputation of the building. If the HOA board is in a legal battle with a contractor, or if the “pet policy” is too strict, your pool of buyers shrinks. If the building has “Rental Restrictions,” it might be harder to sell to an investor. You need an exit strategy. If you need to move to assisted living in three months, can you sell this condo in 30 days? In a building with high fees, the answer is often “No.”

XI. Rental Restrictions and Flexibility

I always tell my clients to check the Rental Cap. Many buildings only allow 10% or 20% of units to be rented at one time. If you get sick and need to move in with your kids, you might want to rent out your condo to cover the mortgage. If the rental cap is full, you are stuck with an empty unit and a full bill. This “liquidity lock” is a hidden cost that many 60+ buyers ignore until it’s too late.

XII. Lifestyle vs Financial Tradeoff

Look, I’m not saying condos are bad. I’m saying they are a lifestyle purchase, not always a financial win. You are paying for the convenience of not having to hire a plumber or a lawn guy. You are paying for the social connection of common areas. If you value your time more than your money, a condo is great. If you are trying to maximize your net worth, a well-located single-family home usually wins. It’s about being honest with yourself. Do you want to be the “Master of your Domain,” or are you okay with a “Board of Directors” telling you what color your front door has to be?

XIII. Step-by-Step: How to Calculate Your Personal TCO

Follow these steps to find your real number. Don’t skip the math; the math doesn’t care about your feelings.

Step 1: Get the Monthly Fixed Total. Add your mortgage, property taxes (divide annual by 12), and the current HOA dues. This is your “Base Cost.”

Step 2: Add 15% for HOA Growth. Historically, fees go up. Multiply your current HOA fee by 1.15 to see what you’ll likely be paying in 24-36 months.

Step 3: Factor in Interior Maintenance. Take 1% of the condo’s purchase price and divide by 12. If the condo is $400,000, that’s $333 per month you should be setting aside for your own appliances and repairs.

Step 4: The Assessment Buffer. Look at the Reserve Study. If it’s underfunded, add a “risk premium” of $100–$300 per month to your calculation. This is your “savings account” for the day the board sends out a bill for a new roof.

Step 5: Calculate Utility Gaps. Ask the current owner for 12 months of electric bills. Many condos have poor insulation or shared HVAC systems that are incredibly inefficient.

Step 6: Total the Numbers. Add Steps 1 through 5. This is your True TCO. If this number is more than 35% of your gross monthly income, you are “house poor” in a condo, which is a dangerous place to be after 60.

XIV. Comparison: Condo vs House vs Renting

Which one wins? It depends on your 10-year horizon. In 2026, renting has actually become a viable strategy for some seniors because it caps your risk. When the elevator breaks in a rental, the landlord pays. When it breaks in a condo, you pay. However, the condo gives you a sense of “home” and potential appreciation that a rental never will. A house gives you the most control but the highest “labor cost.” If you enjoy gardening, the house wins. If you hate it, the house is a prison.

Feature

Condo Living

Single Family Home

Renting (Luxury)

Cost Stability

Medium (HOA Hikes)

Low (You fix it all)

High (Fixed Lease)

Control

Low (Board Rules)

High (Your Property)

Low (Landlord Rules)

Risk Exposure

High (Assessments)

Medium (Major Repairs)

Zero (No Equity)

XV. Common Mistakes to Avoid

I see the same three mistakes every year. First, people buy for the amenities. They see a gym and a sauna and think, “I’ll use that every day!” Fast forward six months, and they haven’t stepped foot in the gym once, but they are still paying $150 a month for the electricity and insurance on it. Don’t pay for a lifestyle you don’t actually lead.

Second, people ignore Pending Litigation. If the HOA is suing the developer for a leaky roof, you won’t be able to get a traditional mortgage, and the building’s value will stay flat for years. Third, they assume “Maintenance-Free” means they don’t need a toolbox. You still need to change your air filters, fix your leaky faucets, and deal with your own appliance failures. The HOA only cares about the grass and the bricks.

XVI. Final Decision Framework for Seniors

Before you sign that contract, ask yourself these four brutal questions:

Can I afford a $20,000 surprise bill? If the answer is “No,” you need to find a building with a 90%+ funded reserve.

Do I mind being told what to do? If you want to paint your balcony pink, a condo is not for you.

Will this building work for me at age 85? Check for “Step-Free” access and wide hallways. If you have to climb stairs to get to the elevator, it’s a “no.”

Is the Board competent? Read the last six months of board meeting minutes. If they are arguing about the color of the mulch while the roof is leaking, get out.

Lifestyle Comparison

VIII. Internal Resources & Further Reading

A proper strategy requires multiple data points. Do not make a decision based on one article alone. Expand your knowledge by reviewing these critical HousingAfter60.com resources:

[Senior Property Tax Relief Costs: Labor vs. DIY Savings Tables] — Rising assessments are cannibalizing senior equity. This guide uses first-principles logic to break down “Circuit Breakers,” Homestead Exemptions, and the structural risks of high-tax jurisdictions. We provide the 2026 Cost Transparency Table to help you decide between fighting taxes or selling for a profit.

[Stop Being House Rich and Cash Poor: The 2026 Home Equity Exit Strategy] — In this guide, we are going to perform an “Equity Harvest” in order to help seniors cash out home equity. This isn’t just selling your home; it’s a strategic extraction of capital. We are moving your wealth from a stagnant, high-maintenance asset into a liquid, cash-flowing portfolio.

XVII. Conclusion: The Right Way to Think About Condo Ownership

Condo ownership is not cheaper—it is just structured differently. It is an agreement to share costs and risks with a group of strangers. When that group is well-managed and the building is healthy, it’s a dream. When it’s poorly managed, it’s a financial nightmare that is very hard to escape.

The real goal of your housing search after 60 should be predictability. You want to know what your life will cost so you can enjoy your time without checking your bank balance every morning. Run the TCO. Read the reserve study. Be the most informed buyer in the room. “The best condo decision isn’t the one with the lowest monthly payment—it’s the one you can comfortably afford five years from now, even if everything gets more expensive.”

XVIII. The 2026 Condo “Financial Survival” Checklist

Before You Sign: 15 Questions That Will Save Your Retirement

I. The Paper Trail (The “Truth” Documents)

The 2026 Reserve Study: Is it less than 3 years old? (If no, the HOA is guessing at their costs).

Percent Funded Ratio: Is the reserve fund at least 70% funded? (Under 30% is a “Debt Bomb” waiting to happen).

The “Special” History: How many special assessments have been leveled in the last 10 years? (If it’s more than two, the board can’t manage a budget).

The Pending Litigation File: Is the HOA currently suing—or being sued by—a contractor or owner? (Lawyers eat reserve funds for breakfast).

The 2026 Milestone Inspection: Has the building passed its state-mandated structural safety check?

II. The Unit “Bones” Audit

HVAC Age & Tech: Is the AC unit more than 10 years old? (Replacement in a high-rise costs 2x a standard house).

Window Seal Integrity: Check for fogging. (In many condos, window replacement is a $10k+ “Owner Responsibility”).

The “Sound” Test: Can you hear the neighbor’s TV or toilet? (Bad insulation ruins resale value).

Electrical Panel Load: Is the panel rated for 2026 modern appliance loads (EV charging, high-speed mesh)?

Water Shut-off Valves: Are they localized to your unit, or do you have to shut off the whole floor to fix a leak?

III. The Lifestyle & Governance “Gag” Rules

The Rental Cap: Is the building at its limit for renters? (If yes, you lose your “exit strategy” flexibility).

The “Pet” Fine Print: Are there weight or breed restrictions that would force you to choose between your home and your dog?

Modification Rules: Can you install a walk-in tub or grab bars without a 3-month board approval process?

Parking & Storage Titles: Is your parking space “Deeded” (you own it) or “Assigned” (the board can move you)?

The Insurance “Gap” Analysis: Does your HO-6 policy include at least $50,000 in Loss Assessment Coverage?

About The Author

About Charles O’Dell: Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement.

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement.

Senior Couple Outside Backyard ADU

Introduction

Summary: Transitioning into a tiny home or an Accessory Dwelling Unit (ADU) can dramatically lower your overhead, but hidden infrastructure...

Emotional Weight of a Large Home

Introduction

Summary: Liquidating a large residential property quickly requires a cold, mathematical trade-off between speed and final asset price. Traditional...