Introduction

Summary: Transitioning into a tiny home or an Accessory Dwelling Unit (ADU) can dramatically lower your overhead, but hidden infrastructure expenses, local zoning barriers, and uncooperative layout designs can quickly derail your retirement portfolio. This comprehensive guide breaks down the true capital expenditures, structural requirements, and ten-year financial trajectories associated with these alternative housing types. Note: Local labor rates for tiny home construction and ADU site development change constantly. See our full regional cost table below.

Affiliate Disclosure

I believe in complete transparency. This article contains affiliate links to specific tools, hardware, and structural systems that I have vetted. If you click these links and make a purchase, I receive a small commission at no extra expense to you. This revenue keeps this site running without selling out to corporate marketing fluff.

Video Guide Overview

The Short Answer

The financial validity of tiny homes and Accessory Dwelling Units (ADUs) for seniors depends entirely on site-specific variables, municipal codes, and long-term medical realities. Moving into a tiny home or a backyard cottage can eliminate a traditional mortgage, drop monthly utilities under $100, and place you close to family care networks.

However, your projected return on investment (ROI) vanishes if:

- Your local municipality treats tiny homes on wheels as recreational vehicles (RVs).

- Your backyard requires $25,000 in utility trenching and civil engineering.

Financially, an ADU serves as a permanent asset that boosts primary property value, while a mobile tiny home acts as a depreciating asset akin to a vehicle. Do not make this move based on emotional lifestyle videos; look at the hard zoning codes and utility connection estimates first.

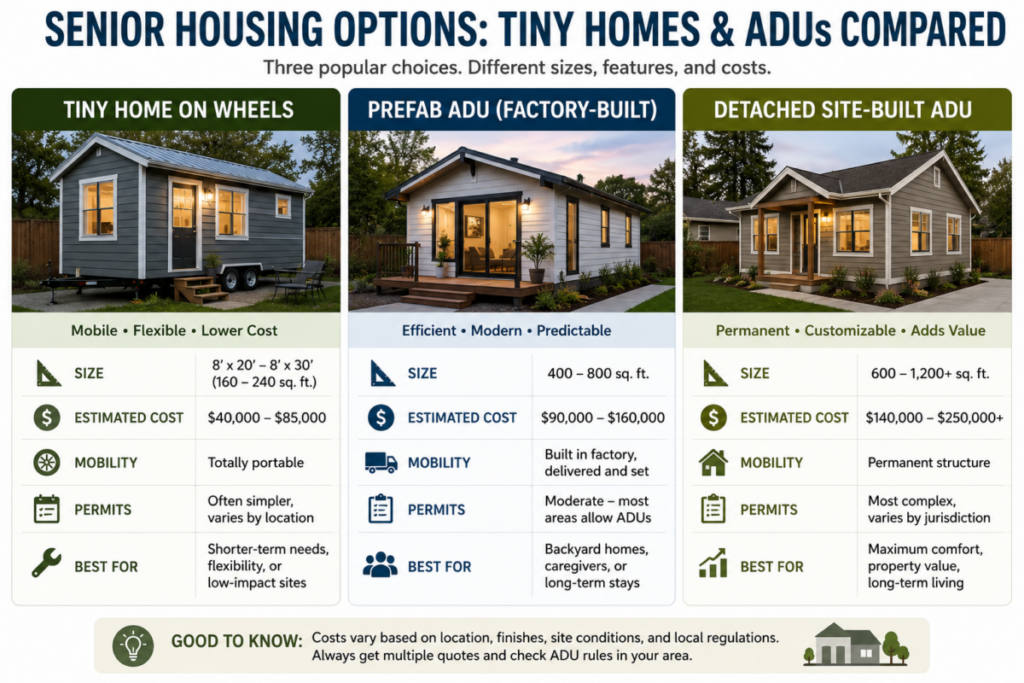

1. What Are Tiny Homes and ADUs?

We need to strip away the lifestyle marketing terms and look at the physical structures. A tiny home is generally defined as a standalone living structure that measures under 400 square feet. These are split into two categories:

- Tiny Homes on Wheels (THOWs): Built on a heavy-duty trailer chassis for portability.

- Foundation-Bound Tiny Homes: Placed on a fixed, permanent base.

Layouts typically optimize every square inch, using lofts, multi-functional furniture, and compact wet baths.

An Accessory Dwelling Unit (ADU) is a secondary residential housing unit located on the same lot as an existing single-family primary home. You might know them as backyard cottages, granny flats, carriage houses, or garage conversions. Unlike a simple guest house, an ADU must include permanent provisions for living, sleeping, eating, cooking, and sanitation. It is tied to the main property infrastructure but functions as a separate, self-contained household.

Seniors are looking at these units because traditional single-family suburban homes are turning into financial money pits due to:

- Rising property taxes

- Escalating insurance premiums

- Deferred maintenance expenses

Downsizing to a micro-footprint eliminates hours of vacuuming, thousands of dollars in roof repairs, and keeps you within arm’s reach of family.

Technical Deep Dive: Structural Engineering and Foundation Mechanics

From a structural engineering perspective, a permanent ADU and a mobile tiny home have entirely different structural loading mechanics. A standard ADU built on a concrete slab foundation relies on continuous soil support. The foundation must extend below your local frost line to prevent frost heaving from cracking the drywall and twisting the framing members.

A tiny home on wheels sits on a steel trailer chassis. The entire structural dead load and live load are concentrated on the leaf springs, axles, and leveling jacks. Because these units move down the highway at 65 miles per hour, they must withstand lateral wind shear forces up to 120 pounds per square foot. This requires heavy-duty steel hurricane straps tying the 2×4 wall studs directly to the steel trailer frame. If you build a tiny home with standard residential framing techniques without anchoring it to the chassis, a single trip down the interstate will turn your retirement dream into a pile of splintered kindling.

Furthermore, weight distribution is vital. You cannot place all your heavy appliances, water tanks, and battery banks on one side of the trailer axles. The tongue weight must remain between 10% and 15% of the total vehicle weight.

- If the tongue weight is too low: The trailer will sway violently behind the tow vehicle.

- If it is too high: It will crush the rear suspension of your truck.

This strict weight balance requirement limits where you can place heavy items like solid hardwood cabinets or natural stone countertops.

2. The Financial Benefits of Tiny Homes for Seniors

The primary financial driver here is the total elimination of a traditional mortgage. A well-built, park-model tiny home costs between $60,000 and $130,000. If you are sitting on a substantial nest egg or selling a primary home worth $400,000, you can pay cash for the tiny home and pocket the remaining equity to fund your everyday living costs.

Your monthly operating expenses will drop significantly due to:

- Reduced energy bills: Heating and cooling 300 square feet takes a fraction of the energy required for a 2,500 square foot house. If you install a highly efficient mini-split heat pump system, your electric bill can drop to less than $40 a month.

- Favorable tax status: Property taxes on mobile tiny homes are often assessed as personal property taxes through your department of motor vehicles rather than real estate taxes, saving you thousands annually.

This predictability makes it much easier to balance your retirement budget when relying solely on fixed income sources like Social Security.

Technical Deep Dive: 10-Year ROI and Capital Depreciation Scenarios

Let us apply cold financial logic to this option. You must understand the difference between an appreciating asset and a depreciating asset. A tiny home on wheels is legally personal property; it is not real estate. The moment you pull it off the manufacturer’s lot, it begins to depreciate just like a motorhome or a pickup truck.

Consider this 10-year comparative scenario based on selling a primary home for $300,000:

Scenario A: Tiny Home on Wheels (Depreciating Asset)

- Spend $100,000 on a tiny home on wheels (depreciating at 5% annually). Value at Year 10: $59,873.

- Invest remaining $200,000 in a conservative index fund (6% compounding return). Value at Year 10: $358,169.

- Combined net worth at Year 10: $418,042.

Scenario B: Foundation-Bound Micro-Home (Appreciating Real Estate)

- Spend $100,000 on a plot of land and build a permanent foundation micro-home (appreciating at 3% real estate historical averages). Value at Year 10: $268,783.

- Invest remaining $100,000 in the same 6% index fund. Value at Year 10: $179,084.

- Combined net worth at Year 10: $447,867.

By choosing a permanent foundation over a wheeled trailer, you prevent $29,825 from disappearing into pure asset depreciation.

3. The Financial Benefits of ADUs for Seniors

Building an ADU on your adult child’s property is a brilliant way to pool familial wealth. It allows you to downsize into a custom, modern living space without competing in the brutal open real estate market. This arrangement also helps you avoid the astronomical costs of private assisted living facilities, which frequently top $5,000 a month.

Alternatively, if you stay in your primary home, you can build an ADU in your backyard and use it as an income-producing asset.

- Renting out a long-term backyard cottage can bring in a reliable $1,200 to $2,500 a month in supplementary retirement income.

- When you eventually decide to sell the property, a legally permitted ADU adds direct appraisal value to the real estate, making the home highly attractive to future multigenerational buyers.

Technical Deep Dive: Property Tax Assessment and Long-Term Value Trajectories

Adding a permanent accessory structure to a parcel of land triggers a supplemental property tax reassessment. Do not assume your tax bill will stay the same. Local tax assessors use a blended approach called the cost approach to determine how much value the new unit adds to the property.

If you spend $180,000 to construct a detached ADU:

- The county tax assessor will determine the market value equivalent of that square footage in your neighborhood, typically increasing the overall property value by roughly 25% to 35% of the total construction cost.

- If your local property tax rate is 1.5%, a $60,000 increase in assessed value means you will owe an extra $900 in property taxes every single year.

You must also consider how this impacts your property insurance. You will need to switch from a standard homeowner policy to a landlord policy or add an “other structures” rider with high replacement cost limits. This adjustment will bump your annual premium up by $300 to $600. You must factor these recurring tax and insurance expenses into your rental cash flow analysis before projecting your net retirement income.

4. Comparing Tiny Homes, ADUs, and Traditional Senior Housing

Traditional retirement communities offer great social activities, but they come with restrictive homeowner association (HOA) rules and steep monthly amenity fees that can rise on a whim. A tiny home gives you total independence and eliminates those overhead fees, though you do lose out on community maintenance services.

When comparing an ADU to an assisted living facility, the math is staggering. Over five years, an assisted living facility can easily drain $300,000 of your savings. Building an ADU costs money upfront, but that capital stays within your family estate rather than going to a corporate care facility.

Many seniors ask me how tiny homes differ from manufactured homes. A standard mobile or manufactured home is built to federal HUD safety codes and usually offers more interior space and comfort. Tiny homes on wheels are often built to RV standards (NFPA 1192), which means they face much stricter local parking restrictions and have lower resale value compared to a manufactured home placed on a permanent foundation.

Technical Deep Dive: Comparative Financial Matrix Analysis

Let us compare the ten-year total cost of occupancy across all four distinct options, factoring in initial capital investment, recurring monthly fees, inflation, maintenance, and asset appreciation or depreciation:

- Traditional Senior Living Community: Assuming zero initial down payment for a rental model, an average monthly rent and fee structure of $3,500, and a 4% annual inflation escalator. Over 10 years, your cumulative out-of-pocket cash outflow will be a stunning $504,252 with zero equity.

- Assisted Living Facility: At an initial $5,500 a month with a 5% annual care inflation escalator, this route will cost you a total of $830,174 over a decade.

- Backyard ADU: Built for $150,000 cash. Recurring costs are limited to utilities, property tax increases, and minor maintenance (averaging around $350/month initially). Over 10 years, accounting for inflation, your operational costs will be roughly $48,342. Adding your initial $150,000 building cost brings your total cash outlay to $198,342, while the asset appreciates alongside the primary property.

The financial logic here is clear: permanent personal real estate assets always beat paying high monthly fees to a third-party corporation.

5. Hidden Costs Seniors Should Understand

The biggest trap for seniors is assuming that a $70,000 sticker price on a tiny home is all you will pay. If you do not own land, you have to buy or lease a plot. Leasing a space in a tiny home community can cost anywhere from $500 to $1,200 every single month, which can quickly wipe out the savings you gained by downsizing.

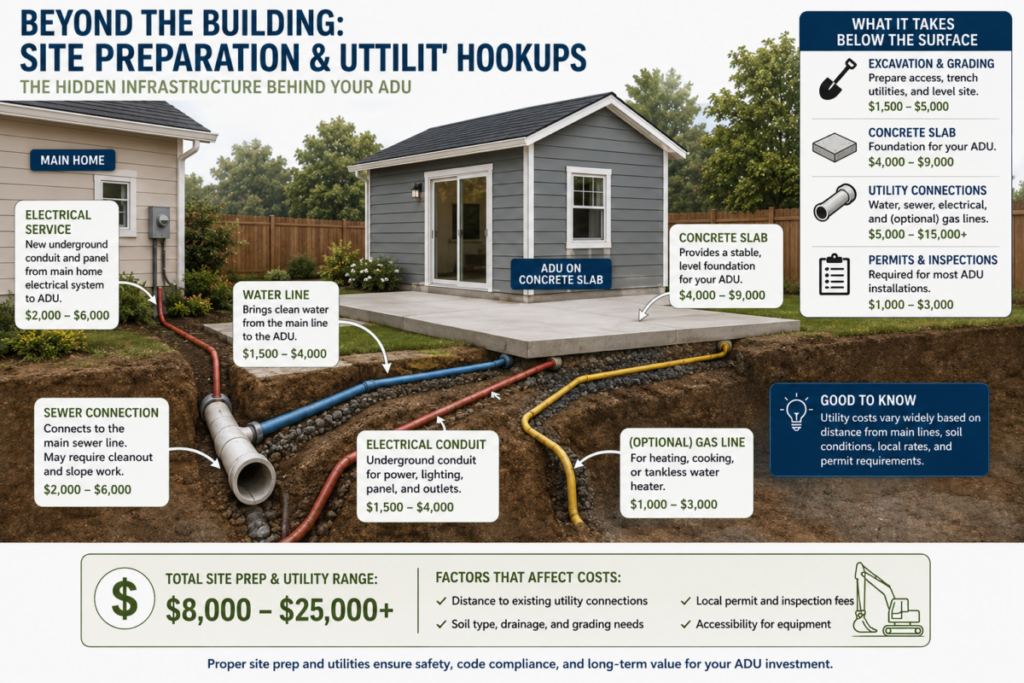

Then comes the infrastructure. You cannot just run an extension cord from the main house and call it a day. You need real utility hookups:

- Electricity: If your local code requires a separate, dedicated electric meter for a new ADU, your power company will charge you thousands just to drop a new line from the transformer.

- Wastewater: If your primary home uses a septic system, adding an ADU might require you to install an expensive, larger capacity septic tank to handle the increased daily wastewater flow.

Technical Deep Dive: Civil Engineering, Permitting, and Impact Fees

Before a single piece of wood is cut, you have to deal with municipal bureaucracy. City planning offices charge impact fees to offset the increased demand on local roads, parks, and water treatment systems. In some restrictive jurisdictions, these impact fees alone can top $15,000 before you even get your building permit.

From a civil engineering standpoint, your backyard layout might require an expensive engineered grading plan:

- If the slope of your yard drops more than 12 inches across the footprint of the planned ADU, you cannot use a simple concrete pour. You will need to build an engineered retaining wall to prevent rainwater runoff from undermining the foundation.

- Plumbing hookups can also get incredibly complicated. Standard gravity-fed sewer lines require a downward slope of at least one-quarter inch per linear foot. If your backyard ADU sits lower than the main sewer line at the street, you cannot rely on gravity. You will have to install a commercial-grade sewage ejector pump system, requiring deep excavation, thick schedule 40 PVC piping, and a reliable electrical backup system to ensure functionality during a power outage.

6. Accessibility and Long-Term Practicality

A home that fits perfectly when you are 62 can become completely unlivable by the time you reach 75 if it is not designed correctly. Most trendy tiny homes feature cute sleeping lofts accessible only by steep vertical ladders. If you develop arthritis or require knee replacement surgery, that loft becomes an unreachable hazard.

True aging-in-place design requires:

- Single-level living layouts

- Zero-threshold entryways

- 36-inch wide interior doorways to accommodate potential wheelchair or walker access

You must also consider storage space. Downsizing from a 2,000 square foot family home down to 350 square feet means letting go of decades of personal belongings, which can be an emotionally taxing process.

Technical Deep Dive: HVAC Load Calculations and Building Envelope Insulation

A micro-home has a very small thermal mass, meaning it heats up and cools down much faster than a standard large house. If your building envelope is poorly insulated, your mini-split system will short-cycle. This means it will turn on and off constantly, which wears out the compressor and causes uncomfortable swings in humidity.

Your builder must perform a proper Manual J load calculation to match the heating and cooling system to the exact square footage of the space. Do not let them install an oversized 2-ton system in a 350 square foot space just because it is what they have on hand.

For the building envelope, standard fiberglass batts are not enough for a tiny home. You should look for closed-cell spray foam insulation. Closed-cell foam provides a higher R-value per inch (around R-6.5 to R-7) and acts as a built-in vapor barrier. This detail is absolutely critical for preventing moisture from condensing on the inside of your walls, which can lead to toxic mold growth in tight, unvented spaces.

7. Best Situations for Seniors Considering Tiny Homes or ADUs

These alternative options work beautifully for empty nesters who want to clear out housing debt, lower their everyday upkeep chores, and free up their home equity. It is a fantastic option for families who want to establish a close, supportive multigenerational household.

By building a backyard cottage on an adult child’s property, you can maintain your independent living privacy while remaining close enough for daily family dinners and easy caregiving assistance. This setup gives everyone their own space while sharing the overall financial responsibility of land ownership.

Technical Deep Dive: Equity Extraction and Legal Frameworks

If you plan to sell your primary home and invest your hard-earned equity into an ADU on a parcel owned by your adult child, you must protect your financial interests with a clear legal agreement. Do not rely on casual verbal agreements. If your child goes through a divorce or faces bankruptcy, the property could be forced into a liquidation sale, and your investment could disappear overnight.

To protect your wealth, you need a real estate attorney to draft:

- A formal life estate deed or a long-term ground lease recorded directly with the county. This document guarantees your legal right to occupy the ADU for the rest of your life.

- A clear framework regarding tax implications. If you give your child $150,000 to build a structure on their land, the IRS may classify that money as a taxable gift. To avoid gift tax implications, you can set up the funds as an equity investment or a formal intra-family loan with a structured repayment schedule that matches the IRS applicable federal rate.

8. Situations Where Tiny Homes or ADUs May Not Work Well

If you have advanced, chronic health conditions that require frequent visits from in-home care nurses or specialized medical machinery, a tiny home can quickly start to feel like an overcrowded obstacle course. There simply is not enough physical room to maneuver a wheelchair easily around tight corners or store large oxygen tanks.

You should also look into your local zoning laws. Many conservative municipalities completely ban tiny homes on wheels or restrict them to licensed RV parks. If you plan to live in an area with strict zoning or local HOA rules, you could face expensive daily fines or legal battles just for parking your home on your own land.

Technical Deep Dive: Regulatory Hurdles and Healthcare Proximity Logistics

The legal battle over tiny homes comes down to municipal zoning classifications. Most local building departments run on older ICC rules that require a minimum room size of 120 square feet for a single dwelling unit. If your tiny home falls below these standard limits, the city will refuse to grant you a Certificate of Occupancy.

Additionally, you must consider the distance to emergency medical services. Many tiny home communities are located in rural areas where land is cheap. If you have a medical emergency, a 45-minute ambulance ride to the nearest level-1 trauma center can have serious consequences. You need to map out the distance to your primary doctors and local hospitals before committing to a rural tiny home lifestyle.

9. Questions Seniors Should Ask Before Making a Decision

Before you sign any contracts or buy any plans, you must ask yourself a few hard financial, legal, and lifestyle questions:

- What are the total upfront site development costs, including utility trenching and permits?

- Will I have to pay recurring monthly lot lease fees or higher property taxes?

- Is this alternative structure fully legal under local city and county zoning codes?

- Does the interior layout include universal design features that will work safely for my physical health over the next 10 years?

Technical Deep Dive: Due Diligence Checklists and Zoning Audits

To complete a proper zoning audit, you need to visit your local municipal planning desk and review their official zoning maps. You must find your parcel’s exact zoning designation, such as R-1 for single-family residential.

Next, request a copy of the specific Accessory Dwelling Unit ordinance for that zone and check the following parameters:

- Setback requirements: Most cities require a detached ADU to sit at least 5 feet away from side property lines and 10 feet away from the rear property line.

- Maximum lot coverage limits: If your city limits total lot coverage to 40%, and your primary house already takes up 38% of the lot, you will be legally barred from building a backyard cottage, regardless of how much open yard space you have left.

10. 2026 Cost Transparency Table

The following table outlines the estimated capital expenditures for a 400-square-foot detached ADU compared to a 350-square-foot premium tiny home on wheels. These numbers reflect real 2026 national averages for materials, structural framing, and municipal compliance fees. Review these figures carefully before tapping into your home equity or retirement savings.

| Expense Category | Tiny Home on Wheels (THOW) | Detached ADU (Permanent) |

|---|---|---|

| Chassis / Foundation | $7,500 (Triple-axle trailer base) | $18,000 (Poured concrete slab foundation) |

| Framing & Building Envelope | $14,000 (Standard 2×4 lumber framing) | $34,000 (Engineered lumber and structural panels) |

| Insulation Material & Labor | $3,200 (DIY spray foam kit application) | $6,500 (Professional closed-cell spray foam) |

| Utility Connections & Trenching | $2,500 (Temporary RV heavy-duty hookups) | $14,500 (Deep permanent underground street tie-ins) |

| Permits, Surveys, & Impact Fees | $450 (Standard DMV registration) | $11,000 (Municipal civil engineering & impact fees) |

| Interior Finish & Accessibility Features | $9,000 (Standard residential grade finishes) | $22,000 (Universal design low-threshold fixtures) |

| TOTAL ESTIMATED CAPITAL OUTLAY | $36,650 | $106,000 |

Key Cost Takeaways for Seniors:

- The Upfront Site Disparity: While a Tiny Home on Wheels (THOW) boasts a significantly lower initial build cost, it requires a legal, pre-developed lot or a leased space in an RV park to legally occupy.

- Impact Fees: Permanent ADU construction triggers local municipal development fees that can quickly add 10% or more to your baseline budget before ground is ever broken.

- Accessibility Engineering: Incorporating 36-inch wide doorways, zero-threshold entries, and reinforced wall studs for grab bars will add roughly $5,000 to $8,000 to the interior finish budget of either unit, but it is mandatory for long-term aging-in-place usability.

11. 2026 Senior Housing Essential Gear & Equipment

Executing a real estate transition or optimizing a home for aging in place requires the proper tools to maintain independent monitoring, structural safety, and efficient space management. The following high-utility hardware items are recommended based on physical performance metrics, long-term durability, and structural reliability. These products are integrated into our projects to protect property equity and mechanical integrity.

| Product Name & Link | Core Technical Specification | Primary Senior Housing Benefit |

|---|---|---|

| Moen Home Care 16-Inch Stainless Steel Grab Bar | Supports up to 500 pounds of downward force when anchored securely into wall studs; features a 1.25-inch bar diameter with a slip-resistant knurled grip surface; constructed from corrosion-resistant 304 stainless steel. | Prevents high-risk slip liabilities in high-moisture bathroom zones without requiring a complete structural wall overhaul. |

| Kidde Wi-Fi Smart Smoke & Carbon Monoxide Detector | Equipped with photoelectric smoke sensors and electrochemical CO sensors; includes a 10-year sealed lithium backup battery; features real-time smartphone notification routing via dedicated wireless network protocols. | Provides early environmental threat detection and immediately alerts long-distance family members or caretakers during an emergency. |

| MagnaCart Personal 150-lb Capacity Aluminum Folding Hand Truck | Constructed with a rugged aluminum frame and 5-inch solid rubber wheels; folds flat to a profile thickness of only 2.5 inches for compact storage; opens instantly with a single motion. | Eliminates axial spinal loading and acute physical strain during down-sizing steps, moving storage crates, or handling heavy bulk supplies. |

Affiliate Product Procurement Strategy:

- Verify Structural Anchor Points: When purchasing hardware items like heavy-duty grab bars, ensure you also buy specialized heavy-duty toggle bolts if direct wall stud alignment cannot be achieved during installation.

- Test Smart Integration Immediately: When deploying wireless safety detectors, confirm that your router sends notifications through to your target smart devices before mounting the hardware permanently to the ceiling surface.

- Prioritize Mechanical Simplification: Select tools and material transport gear that feature mechanical advantages or folding frames to ensure they occupy minimal physical square footage in smaller living layouts.

Links to Other Helpful HousingAfter60.com Articles

9. Summary

Navigating senior housing transitions requires looking past emotional sales pitches and focusing strictly on the bottom-line numbers. Whether you are balancing the capital expenditures of a permanent backyard build or managing the structural variables of aging in place, every decision should protect your retirement equity. Weigh your immediate upfront fees against long-term maintenance costs, verify your local municipal zoning rules, and implement safety upgrades before they become emergencies. Protecting your net worth after 60 comes down to executing logical, data-driven real estate decisions.

10. Author Bio

Charles O’Dell is a senior housing transition expert and the founder of HousingAfter60.com. Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of hands-on industry experience and over 100 successful property flips, Charles specializes in stripping away marketing fluff to help homeowners find sustainable, logical real estate solutions. He applies first-principles financial logic to housing decisions, ensuring seniors protect their hard-earned net worth throughout retirement.Stop Being House Rich and Cash Poor: The 2026 Home Equity Exit Strategy

Written by Charles O’Dell, a former CPA and real estate investor with 23+ years of experience and over 100 successful property flips.