Introduction

Summary: Liquidating a large residential property quickly requires a cold, mathematical trade-off between speed and final asset price. Traditional real estate listings maximize the gross purchase price by exposing the property to the entire retail buyer pool, but they subject the seller to carrying costs, repair demands, and financing contingencies that average 60 to 90 days. Real estate auctions eliminate contingencies and guarantee a non-negotiable closing date within 30 days, yet they risk a lower baseline valuation and command steep buyer premiums. Note: Local labor rates for home maintenance and auction coordination change constantly. See our full regional cost table below.

Video Guide Overview

Affiliate Disclosure

I believe in total financial transparency. Some of the links inside this guide are affiliate links. This means if you click through and purchase a product or service, I earn a commission at no extra cost to you. I only recommend tools, platforms, or services that survive my personal first-principles analysis. This financial engineering helps keep HousingAfter60.com independent and free from corporate real estate bias.

The Short Answer: Speed vs. Net Proceeds

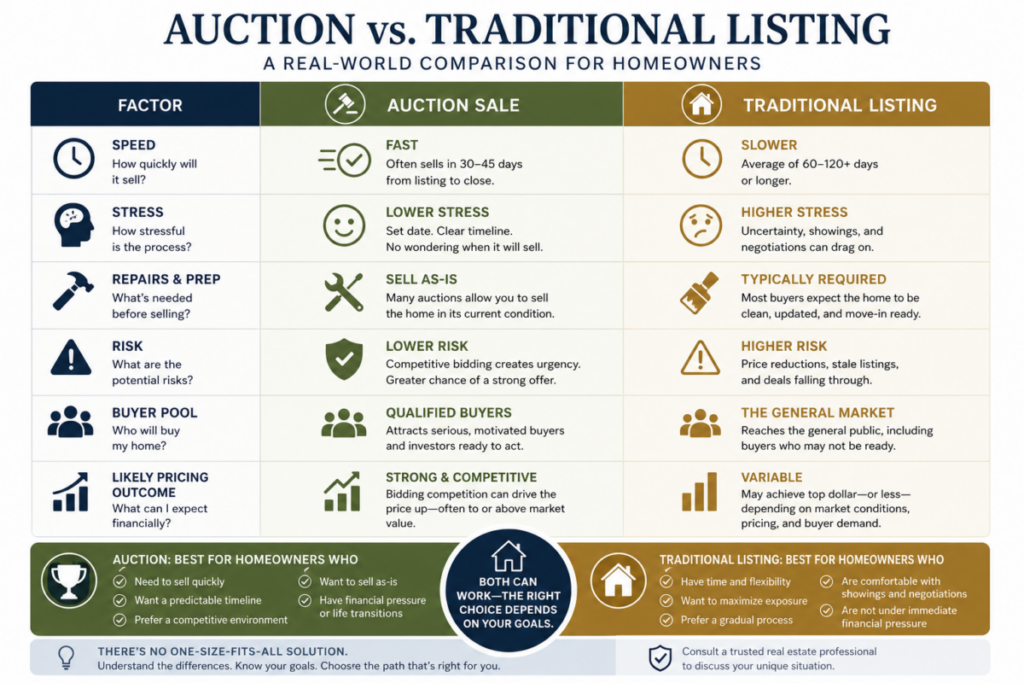

If your priority is extracting every last cent of equity from your home, a traditional real estate listing via the Multiple Listing Service (MLS) remains the optimal choice. This assumes your property is in marketable condition and you possess the liquidity to cover monthly holding costs during the marketing and escrow phases. However, if your holding costs are high, the property requires substantial deferred maintenance, or an urgent life transition demands immediate liquidity, a real estate auction is superior. Auctions convert a real estate asset into cash on a fixed calendar date. They strip away inspection contingencies, appraisal shortfalls, and buyer financing issues by demanding non-refundable cash deposits. You trade a predictable, market-driven discount on the sale price for absolute certainty and the total elimination of ongoing carrying costs.

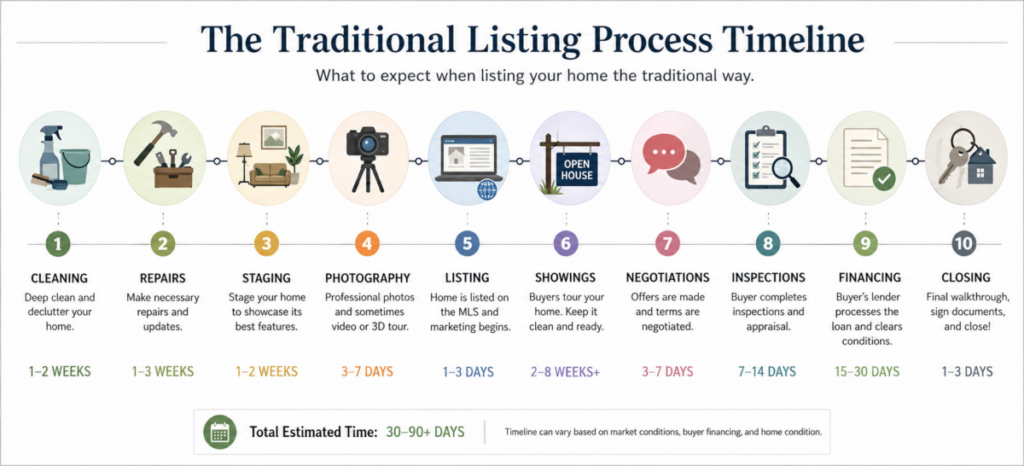

Section 1: What is a Traditional Real Estate Listing?

A traditional real estate listing relies on an open-market, retail approach to home sales. As a seller, you contract with a licensed real estate broker who acts as your fiduciary agent. The agent lists the home on the local Multiple Listing Service, which syndicates the data to thousands of consumer-facing search portals. Buyers schedule individual property viewings, accompanied by their own agents, or attend weekend open houses. This method depends entirely on courting the emotional and practical desires of owner-occupant buyers who intend to fund the purchase via conventional, FHA, or VA mortgage financing products.

The operational lifecycle of a traditional sale is highly fragmented. It begins with property preparation, which frequently requires cosmetic upgrades, deep cleaning, decluttering, and staging. Once live on the market, the property undergoes an indefinite period of public exposure until an offer is submitted. Negotiation ensues regarding the gross purchase price, seller concessions, and repair credits. Once an agreement is executed, the property enters an escrow period. During this phase, the buyer executes home inspections, titles are cleared, and the buyer’s lending institution processes the mortgage loan. This process requires a physical appraisal to verify the home’s value matches the loan amount.

Technical Deep Dive: Underwriting and Appraisal Hurdles in 2026

The traditional mortgage underwriting landscape in 2026 has grown exceptionally rigid due to heightened macroeconomic volatility and stricter bank capital requirements. When an owner-occupant buyer submits an offer on a large, older property, their lender subjects the asset to strict property condition standards. For example, traditional conventional underwriting guidelines require that all major structural elements, including the roof, HVAC systems, electrical panels, and plumbing networks, possess a minimum remaining economic life. If a home inspector identifies a roof with less than three years of functional viability, the underwriter will condition loan approval upon full roof replacement prior to closing.

Furthermore, the appraisal process introduces severe valuation friction for atypical or expansive properties. In 2026, automated valuation models (AVMs) are used heavily by lenders to screen properties before human appraisers step foot on the site. If your home has highly customized features, a non-standard floor plan, or significant deferred maintenance, the AVM flags it as high risk. The subsequent human appraisal must utilize comparable sales within a tight one-mile radius that have closed within the preceding 90 days. In neighborhoods where large homes sell infrequently, the appraiser is forced to make aggressive downward adjustments for age, size, or layout anomalies. This often leaves a valuation shortfall. If the home is under contract for $600,000 but appraises for $550,000, a traditional transaction faces an immediate roadblock. The seller must drop their price by $50,000, the buyer must bring an additional $50,000 in cash to the table, or the transaction collapses completely, forcing the property back onto the market as a stale listing.

Section 2: What is a Real Estate Auction?

A real estate auction is an accelerated asset liquidation mechanism that replaces prolonged negotiation with transparent, competitive bidding. Instead of posting an asking price and waiting for downward offers, an auction establishes a firm date of sale and forces motivated buyers to bid the price upward in real time. The property is marketed intensely for a brief, compressed window, usually 21 to 30 days, culminating in a public bidding event conducted either live on-site or via an online algorithmic platform. All bidding is completely transparent, meaning participants can see exactly what their competitors are willing to pay, which eliminates the blind negotiation common to traditional real estate transactions.

Auctions operate under strict, pre-established legal terms that are non-negotiable for the buyer. All properties sold via auction are transferred in an “as-is, where-is” condition with all faults. Buyers are required to complete all physical due diligence, title reviews, and land-use assessments prior to placing a bid. To participate, bidders must present verifiable funds, such as a cashier’s check or a pre-certified bank wire, often ranging from $5,000 to $50,000 depending on the asset value. The winning bidder must immediately sign a purchase contract and deposit a non-refundable earnest money down payment, typically 10% of the total purchase price, with closing legally mandated within 30 days. No financing or inspection contingencies are permitted.

Technical Deep Dive: Legal Structure and Auction Fee Engineering

The legal framework governing a real estate auction is anchored in the distinction between absolute auctions and reserve auctions. In an absolute auction, the property is legally bound to sell to the highest bona fide bidder on the day of the event, regardless of the price achieved. This structure generates the maximum level of buyer urgency and competitive intensity because it guarantees a sale will occur. However, it exposes the seller to catastrophic downside risk if marketing reach fails or market demand slumps on auction day. Conversely, a reserve auction includes a confidential minimum price established between the seller and the auctioneer. If the high bid fails to meet this reserve threshold, the seller is under no legal obligation to accept the offer and can pass on the sale. While this protects asset value, it can suppress bidder turnout, as professional buyers are often hesitant to invest time and due diligence capital into a property that might not actually be sold.

The financial engineering of an auction also differs fundamentally from standard brokerage models through the utilization of the Buyer’s Premium. In a traditional listing, the seller pays a gross commission out of their sale proceeds to cover both listing and buying brokers. In an auction framework, the auction company typically charges a 10% premium that is added directly on top of the high bid hammered down at the event. For instance, if the high bid on a property is $500,000, the buyer actually pays a gross contract price of $550,000. This structure shifts the primary transactional cost burdens onto the buyer. The seller must still navigate upfront marketing and administrative fees, which range from $2,500 to $10,000, to fund the aggressive, hyper-local, and digital advertising campaigns required to assemble the competitive bidder pool within the compressed 3-week timeline.

Section 3: Why Some Seniors Choose Auctions

The decision to liquidate a significant real estate asset through an auction rather than a standard brokerage listing is rarely driven by a desire to test the limits of real estate appreciation. Instead, it is an exercise in risk mitigation and timeline control. For individuals over 60, a home is often a massive, illiquid store of wealth tied up in a physical structure that no longer aligns with their operational capacity or health profile. When an urgent need arises to transition into an assisted living community or relocate closer to specialized medical infrastructure, waiting six to twelve months for a traditional buyer to secure bank financing is an unviable strategy.

Furthermore, large family homes that have been occupied for decades naturally collect a tremendous volume of personal property and suffer from hidden capital obsolescence. Coping with the logistical nightmare of a traditional sale requires continuous property maintenance, dealing with unexpected buyer walkthroughs, and undergoing stressful home inspections. For a seller with limited mobility, keeping a 4,000-square-foot property in showroom condition for months on end is physically exhausting. An auction bypasses this entirely by shifting the burden of property condition and clear-out onto the buying entity, allowing the senior seller to walk away with a clean slate and definitive financial execution.

Technical Deep Dive: Multi-Party Estate Liquidation Logic

When a large home must be liquidated as part of an estate settlement or a revocable living trust configuration involving multiple adult children or heirs, emotional asset attachment frequently interferes with rational financial decision-making. If one heir believes the property is worth $700,000 based on childhood memories, while another heir recognizes that the outdated electrical system and cracked foundation value it closer to $500,000, a traditional listing inevitably stalls. The heirs will bicker over list prices, counter-offers, and who should pay for repairs demanded by traditional buyers, leading to prolonged market exposure, rising carrying costs, and potential litigation.

An auction acts as a transparent, legally bulletproof solution that neutralizes family friction through unassailable market validation. Because the bidding process is entirely public and market-driven, it establishes the absolute definition of fair market value at that specific point in time. No heir can claim the property was undersold or mismanaged by the executor because the market spoke directly via open competition. The auction contract provides clean, undeniable documentation that satisfies probate courts, title companies, and trust parameters. It accelerates the distribution of estate liquid assets to heirs within a fixed 30-day window, preventing ongoing property tax obligations and insurance premiums from eroding the principal value of the estate.

Section 4: When Auctions Can Work Very Well

Auctions yield their highest utility when deployed against properties that defy standard valuation metrics or face structural market friction. A classic example is the highly customized luxury home or rural estate with significant acreage. These properties lack a standardized pool of comparable sales data, making them incredibly difficult to price accurately within a traditional MLS framework. Real estate agents often overprice these homes out of a desire to flatter the seller, causing the property to sit on the market until it becomes visually stale to buyers, who then assume some hidden physical defect exists. An auction flips this dynamic by creating a sense of extreme scarcity and urgency, forcing affluent buyers to compete openly for an item that cannot be easily replicated on the open market.

This approach also works wonders for properties suffering from extreme deferred maintenance, such as severe structural settling, outdated mechanical systems, or hoarding conditions. Traditional owner-occupant buyers cannot secure financing for these properties because banks refuse to underwrite homes without functioning kitchens, bathrooms, or structural integrity. An auction bypasses the retail buyer pool completely and targets capitalized real estate professional buyers, syndicates, and cash investors. These entities do not care about cosmetic appeal; they evaluate the property purely through a pro-forma spreadsheet lens, pricing in renovation labor against potential market yield.

Technical Deep Dive: Competitive Bidder Psychology and FOMO Mechanics

The underlying force driving high performance in a successful real estate auction is the deliberate engineering of competitive urgency, commonly known as the “fear of missing out” or FOMO. In a traditional listing, a buyer operates in a vacuum of information. When they submit an offer, they do so with the knowledge that they can back out during the inspection period, and they have no idea if other offers are real or merely a negotiation tactic used by the listing agent. This lack of transparency causes buyers to bid conservatively and include numerous protective contingencies to manage their risk.

An auction completely reverses this psychological dynamic. When multiple qualified bidders are gathered in a single room or logged into an online portal with active countdown clocks, all information becomes transparent. A bidder sees their competitor physically raise a paddle or input a higher bid. This creates immediate social proof: if other capitalized entities are actively bidding on this asset, its value is validated. This transparent validation lowers the buyer’s perceived risk barrier. As the clock ticks down, the fear of losing the asset to a direct rival over a small increment frequently overrides rational bidding ceilings, causing professional investors and emotional buyers alike to push their bids well past their pre-planned limits, sometimes yielding a final sale price that exceeds traditional retail valuations.

Section 5: When Auctions Can Go Very Wrong

While the velocity of an auction is highly attractive, the mechanism possesses structural risks that can result in substantial equity destruction if executed poorly. The most severe exposure occurs when a seller opts for an absolute auction structure without conducting a rigorous pre-market viability assessment. If the auction company fails to generate sufficient regional and digital advertising traction, or if a sudden macroeconomic shock occurs right before the event, turnout will be low. In an absolute auction, if only three bidders show up and the highest bid is 40% below true market value, the auctioneer’s hammer falls, and the seller is legally obligated to transfer the deed for that deficient amount. There is no legal recourse or cancellation policy once the bidding commences.

Another major point of failure stems from the predatory fee structures utilized by low-tier, unaccredited auction firms. These operators often entice vulnerable senior homeowners with promises of a fast, stress-free cash sale while demanding massive upfront “marketing and administrative fees” ranging from $5,000 to $15,000. These fees are non-refundable, regardless of whether a single bid is placed on the property. These untrustworthy firms frequently pocket the upfront fee, run cheap classified advertisements, and exert heavy pressure on the seller during the event to lower their reserve price to an unreasonable degree just so the firm can collect its transactional premium.

Technical Deep Dive: Illiquidity Traps and Bidder Collusion Risks

In niche regional markets or specialized real estate sectors, auctions can fall victim to an asset illiquidity trap compounded by implicit bidder collusion. Because auctions strip away traditional mortgage buyers, the remaining buyer pool is comprised entirely of cash-rich investors, wholesalers, and institutional flippers. In smaller municipal areas or specific counties, these professional buyers know one another well and attend the same auction events regularly. This introduces a distinct risk of bidding rings or tacit collusion, where buyers intentionally refrain from bidding against each other to artificially cap the final price of a property, later splitting the asset or assigning the contract among themselves post-event.

Furthermore, if a reserve auction fails because the high bid does not meet the seller’s minimum threshold, the property enters an illiquidity trap. The asset has now been publicly exposed to the local investment community and labeled as a “failed auction” property. Traditional retail buyers and real estate agents monitoring the market see this failure and immediately assume the property is plagued by severe title clouds, environmental issues, or structural defects. When the frustrated seller attempts to pivot back to a traditional MLS listing, they find their bargaining position completely ruined. Retail buyers will submit low-ball offers, knowing the seller is desperate for cash and has already exhausted an accelerated liquidation pathway.

Section 6: Why Traditional Listings Still Dominate

Despite the speed and certainty offered by modern auction platforms, over 90% of residential real estate transactions continue to flow through traditional brokerage listings. This dominance is not an accident of history; it is a direct reflection of how consumer capital is structured. The vast majority of individuals seeking to buy a home do not possess hundreds of thousands of dollars in liquid cash sitting in a checking account. Their purchasing power is built on leverage, specifically long-term amortized mortgage loans provided by institutional lenders. Traditional listings are deliberately structured to accommodate this leverage by allowing for extended escrow periods, finance contingencies, and independent appraisal steps.

By making your home accessible to buyers who require mortgage financing, you expand your potential consumer pool exponentially. A larger buyer pool naturally leads to increased competition and a higher ultimate valuation for an asset that is in good repair. Furthermore, traditional listings allow for detailed emotional marketing. Buyers can tour the home multiple times, visualize their family utilizing the space, and negotiate custom terms, such as flexible move-out dates for the seller, that are completely unavailable within the rigid framework of an auction contract.

Technical Deep Dive: Optimization of the Retail Buyer Pool

To maximize your net proceeds from a traditional listing, you must understand the mathematical distribution of the retail buyer pool. Real estate values follow a standard bell curve based on property condition and market exposure. A traditional listing leverages the maximum reach of the MLS to capture the top 5% of buyers who are willing to pay a premium because the property matches their exact emotional or geographical desires. These buyers are looking for a turn-key, move-in-ready experience and are not focused on factoring in investment margins or renovation costs.

When you optimize a traditional listing, you deploy strategic digital staging, targeted broker previews, and systematic price positioning to trigger multiple-offer scenarios. In a balanced or high-demand market, a properly priced traditional home can generate a bidding war that mimics the intensity of an auction while operating on a retail valuation baseline. Because these buyers are using institutional leverage, they are bidding with the bank’s money rather than their own immediate liquid reserves. This allows them to push the purchase price to its absolute limit, providing the seller with a significantly higher net equity payout at closing than could ever be achieved in an investor-dominated auction room.

Section 7: The True Cost of “Waiting for Top Dollar”

Many senior homeowners fall into a cognitive trap where they focus entirely on the gross sale price of their property while ignoring the continuous drain of monthly carrying costs. When an agent tells you that your large home could sell for $650,000 if you wait patiently for six to nine months, that number is an illusion. Every single month that a large, older residential property sits on the market, it consumes a substantial amount of capital in the form of property taxes, insurance premiums, utility bills, landscape upkeep, and basic structural maintenance. These expenses are completely unrecoverable and directly subtract from your net equity at closing.

For a large property, these carrying costs accumulate with alarming speed. A 3,500-square-foot home with an older roof and aging HVAC systems requires continuous climate control to prevent mold accumulation and structural deterioration. If the home is vacant because the owner has already relocated to a retirement community, insurance companies frequently require a specialized vacant home policy premium, which can cost two to three times more than a standard homeowner’s policy due to the increased risk of undetected water leaks or vandalism.

Below is a detailed engineering breakdown of the monthly and 6-month carrying costs associated with holding an unliquidated 3,500-square-foot property in 2026:

Carrying Costs Breakdown Table

| Expense Category | Monthly Cost (Basic/Standard) | Monthly Cost (Premium/Large Scale) | 6-Month Total (Accumulated Loss) |

|---|---|---|---|

| Mortgage Principal & Interest | $1,800 | $3,200 | $10,800 – $19,200 |

| Property Taxes (Assessed) | $450 | $850 | $2,700 – $5,100 |

| Vacant Home Insurance Policy | $250 | $500 | $1,500 – $3,000 |

| Climate Control Utilities (Gas/Electric) | $300 | $600 | $1,800 – $3,600 |

| Landscape & Exterior Upkeep | $150 | $350 | $900 – $2,100 |

| HOA Dues or Community Assessments | $100 | $400 | $600 – $2,400 |

| Preventative Deferred Maintenance | $200 | $500 | $1,200 – $3,000 |

| TOTALS | $3,250 | $6,400 | $19,500 – $38,400 |

Technical Deep Dive: Opportunity Cost and Capital Reinvestment Trajectories

To truly understand the cost of a delayed home sale, you must look beyond direct monthly outlays and evaluate the opportunity cost of trapped equity using a multi-year net-worth trajectory. When a senior has $400,000 of net equity locked up in a slow-selling, non-liquid traditional listing, that capital is effectively dead. It produces zero income while continuously incurring the carrying costs detailed above. If that equity were freed up immediately through an accelerated auction sale, even at a 10% market discount, those funds could be redeployed into income-generating financial instruments.

Let us look at a practical asset trajectory comparison over a ten-year horizon. Scenario A assumes the senior insists on a traditional listing, waiting 9 months to net a gross equity amount of $400,000, while burning $25,000 in carrying costs and enduring high stress. Scenario B assumes the senior utilizes an auction to sell the asset within 30 days, taking an immediate 10% price hit to net $360,000. However, they immediately place that cash into a diversified portfolio of ultra-safe 2026 treasury instruments and high-yield dividend funds yielding a conservative 5% compound annual return.

In Scenario B, the $360,000 compounding annually at 5% grows to approximately $586,440 at the end of year ten, while producing roughly $18,000 in liquid, hands-off income every single year to help cover retirement living or assisted living expenses. Conversely, the senior in Scenario A who waited for top dollar lost nine months of compound interest, spent thousands maintaining an empty house, and delayed their transition plans. When you calculate the compounding return on fast capital versus the continuous drain of a stagnant physical asset, the mathematical reality reveals that a fast liquidation often yields a significantly stronger net-worth position over time.

Section 8: How to Evaluate an Auction Company

Entrusting the liquidation of your primary asset to an auction firm requires deep operational due diligence. You must treat this process exactly like hiring a corporate chief financial officer. Do not rely on slick brochures or emotional appeals about how much they care about seniors. You need to analyze their data, look closely at their transactional history, and review their legal contracts under a microscope to ensure your equity is fully protected.

To protect your financial interests, you must interview multiple operators and demand written answers to the following operational questions:

- What is your documented success rate for reserve auctions within my specific ZIP code? You need to verify that they actually convert listings into completed sales in your local market, not just in distant states.

- Can you provide an itemized breakdown of your marketing budget and media mix? Ensure they are leveraging digital targeted campaigns, programmatic real estate platforms, and local investor syndicates, rather than just placing a single sign in the front yard.

- What specific terms are included in your buyer’s premium framework? You must know exactly what percentage is being added to the hammer price and whether any portion of that premium is shared back with you to offset your upfront marketing costs.

- How do you verify that registered bidders possess true liquid capital before allowing them onto the floor? Demand to see their financial screening protocol to ensure no unqualified individuals can disrupt the bidding process.

Technical Deep Dive: Screening for Predatory Marketing Agreements

When reviewing an auction company’s standard listing contract, you must keep an eye out for predatory clauses designed to lock you into costly obligations regardless of performance. The most dangerous clause to watch for is an uncap-able “upfront marketing fee recharge.” Legitimate auction companies will share the risk by capping upfront marketing costs or absorbing them into the final transactional premium. Predatory operators, however, write clauses that require the seller to pay for expensive print media campaigns, luxury catering for live events, and travel expenses for auction staff, all billed at a hefty markup without requiring your prior written approval.

You must also audit the contract for a “withdrawal penalty clause.” This provision dictates that if you choose to cancel the auction because you are uncomfortable with the pre-auction bidder registrations, or if you reject a low bid that fails to meet your expectations in a reserve framework, you legally owe the auction company the full commission premium based on their estimated market value of the property. This effectively forces you into a corner, compelling you to sell your home at a deep discount just to avoid an immediate five-figure legal penalty. Ensure your contract explicitly states that if the reserve price is not achieved, the contract terminates with zero commissions owed.

Section 9: How to Evaluate a Traditional Real Estate Agent

If you choose to take the traditional listing route, you cannot afford to hire a hobbyist agent, a family friend, or someone who primarily sells small starter condos. Liquidating an expansive, aging family home requires an agent with deep technical experience in senior housing transitions and estate logistics. They must possess a robust network of vetted contractors, estate liquidation vendors, and structural engineers to address property challenges quickly before they derail a transaction.

When screening traditional real estate brokers, disregard their personal charisma and grade them strictly on their answers to these operational metrics:

- What is your average list-to-sale price ratio and days-on-market metric for homes over 3,000 square feet? Look for a track record of accurate initial pricing strategies rather than a pattern of continuous price reductions.

- How do you calculate your initial list price recommendation using first-principles data? Demand a comprehensive market analysis that factors in physical system ages, roof life expectancies, and local carrying cost trends.

- What is your specific plan to manage buyer home inspection objections without blowing up the escrow timeline? Ensure they have reliable contractors on call who can provide rapid, binding repair bids to satisfy stubborn underwriters.

- Can you provide references from at least three estate executors or seniors who have gone through a quick downsizing transition with you? Verify their hands-on experience navigating the unique logistics and paperwork of senior transitions.

Technical Deep Dive: The Stale Listing Trap and Pricing Psychology

The most significant risk in traditional real estate is falling into the “stale listing trap.” This scenario is caused by an agent who practices “buying the listing”—intentionally telling you your home is worth an inflated price just to secure your listing contract. Once the home is live on the MLS at an unrealistic price, it sits completely ignored by qualified buyers. In the retail real estate market, a listing receives the absolute highest level of consumer attention and digital platform algorithmic boost during its first 14 days live on the market.

When a home passes the 45-day mark without an offer, it undergoes an adverse psychological transformation in the minds of consumer buyers and buyers’ agents. They assume that since the property hasn’t sold in an active market, there must be a major hidden flaw, such as a failing foundation or a title issue. To break this stagnation, the seller is forced to execute a series of price cuts. However, these cuts often trail behind the market’s perception of value. A home that could have sold quickly for $600,000 with an accurate initial price strategy often ends up selling for $530,000 after sitting on the market for six months and undergoing multiple desperate price reductions. Accurate, data-driven initial pricing is critical to protecting your equity.

Section 10: 2026 Cost Transparency & Comparison Tables

To make an informed financial choice, you must review the underlying costs of both transaction methods. Below are the comprehensive data tables for 2026, comparing structural preparation costs against transactional service fees and affiliate software tools designed to streamline the liquidation process.

2026 Real Estate Liquidation Cost Table

| Liquidation Activity | Low-End Estimate (DIY / Basic Auction) | High-End Estimate (Pro / Full Brokerage) | Primary Cost Driver |

|---|---|---|---|

| Pre-Sale Home Inspection & Structural Audit | $400 | $1,200 | Square footage and structural complexity |

| Estate Clean-Out & Junk Removal Services | $800 | $4,500 | Volume of personal property and debris weight |

| Cosmetic Repairs, Staging, & Painting | $1,500 | $12,000 | Contractor labor rates and material selection |

| Upfront Auction Marketing & Media Fees | $2,500 | $10,000 | Digital ad spend and local targeted media buying |

| Transactional Commission or Premium Fee | 0% (Paid by Buyer via Premium) | 6% (Paid by Seller via Listing Agent) | Gross final contract price of the home |

| Escrow, Title Search, & Transfer Taxes | 1.5% of sale price | 3.0% of sale price | Municipal transfer tax rates and title insurance |

Affiliate Product Comparison Table

To prepare your home for liquidation, track your carrying costs, and screen local market trends, utilize the vetted tools below:

| Product/Service Name | Primary Application | Core Strategic Benefit |

|---|---|---|

| RealEstatePro Financial Ledger | Carrying cost tracking and property cash-flow analytics | Calculates daily holding costs to show exactly how much equity is being lost each day. |

| HomeAudit Laser Measuring System | Independent precision square footage and layout verification | Prevents listing errors and verifies room sizes to protect against appraisal issues. |

| EstateOrganizer Digital Vault | Document archiving for deeds, titles, and property disclosures | Organizes all necessary documents in a secure space for fast due diligence review. |

Section 11: Common Mistakes Seniors Make

The process of liquidating a long-held family home is an operational minefield. The most common mistake I see seniors make is waiting too long to initiate a sale. They often cling to an overly large property until a sudden health crisis or the loss of a spouse forces a rushed, desperate decision. When you are forced to sell a property under extreme duress, you lose your tactical advantages and are often forced to accept the first low offer that comes your way, resulting in significant equity loss.

Another classic mistake is spending tens of thousands of dollars on major cosmetic renovations right before listing the property. Homeowners frequently install high-end granite countertops, custom cabinetry, or luxury flooring, mistakenly believing they will recover every dollar spent. In reality, modern buyers have their own design preferences and will often rip out brand-new updates. You rarely receive a 1:1 return on investment for major pre-sale renovations; it is far more logical to price the home accurately for its current condition or use an auction framework to sell it completely “as-is.”

Technical Deep Dive: Capital Gains Tax Pitfalls under Code Section 121

When liquidating a primary residence that has experienced significant long-term appreciation, many seniors overlook the tax implications of IRS Code Section 121. This statute allows an individual filer to exclude up to $250,000 of capital gains from their taxable income, while married couples filing jointly can exclude up to $500,000. However, for seniors who have owned a large home for 30 or 40 years in a highly desirable market, the capital gain can easily exceed these exclusion limits.

Let us look at the numbers. If a married couple purchased a home in 1986 for $80,000 and sells it in 2026 for $750,000, their total capital gain is $670,000. After applying the $500,000 exclusion, they are left with $170,000 in taxable capital gains. If they fail to accurately document capital improvements made over the decades, such as roof replacements, room additions, or electrical upgrades, which would raise their tax basis, they will face a substantial federal and state tax bill upon sale. Furthermore, if a spouse passes away and the surviving spouse waits more than two years to sell the property, their exclusion limit drops back down to the single filer cap of $250,000, instantly exposing an additional $250,000 of home equity to capital gains taxes. Consulting with a tax professional before deciding on a sale method is absolutely essential to protect your net worth.

Section 12: Real-World Liquidation Case Studies

To demonstrate how these concepts play out in real life, let us analyze four distinct case studies from my investment files. These examples show how property condition, pricing strategy, and chosen sale method directly impact the final financial outcome.

Case Study 1: The Traditional Listing Success

A senior seller owned a well-maintained, 2,800-square-foot home in a desirable suburban neighborhood. The home featured an updated kitchen, a modern HVAC system, and a roof less than five years old. The seller was under no immediate pressure to relocate and chose a traditional broker listing, pricing the home accurately at market value. The property attracted three competitive retail offers within the first 10 days on the market and closed smoothly in 45 days at 102% of the asking price, maximizing the seller’s net proceeds.

Case Study 2: The Real Estate Auction Success

An estate executor had to liquidate a massive, 4,500-square-foot custom home built in 1978. The property suffered from decades of deferred maintenance, including a failing roof, an outdated electrical panel, and a non-functional pool. Traditional buyers could not secure financing, and the home sat empty, racking up $4,000 a month in carrying costs. The executor opted for a targeted reserve auction. Within 21 days of intense digital marketing, 14 cash investors registered to bid. The live event drove the price up to $420,000, completely cash, with all contingencies waived and closing completed in under three weeks.

Case Study 3: The Failed Auction Strategy

A homeowner insisted on utilizing an absolute auction for a highly specialized rural property with complex zoning issues, but hired a low-end auctioneer who primarily handled farm equipment rather than real estate. The auctioneer ran minimal local marketing and failed to target out-of-state land buyers. On auction day, only four buyers showed up, and the bidding stalled at a point roughly 45% below the home’s true value. Because it was an absolute auction framework, the home sold for that low amount, resulting in a severe, unrecoverable loss of family equity.

Case Study 4: The Traditional Listing Failure

A senior couple chose to list their home traditionally but insisted on an initial asking price $100,000 above market data, rejecting their agent’s advice. They wanted to test the market and see if they could get lucky. The home sat live on the MLS for five months without a single offer, becoming a stale listing. Desperate to fund their move to a retirement community, they executed three consecutive price cuts, eventually accepting a low-ball offer at 15% below true market value. They also had to pay for $15,000 in buyer-demanded repairs during escrow and cover five additional months of carrying costs.

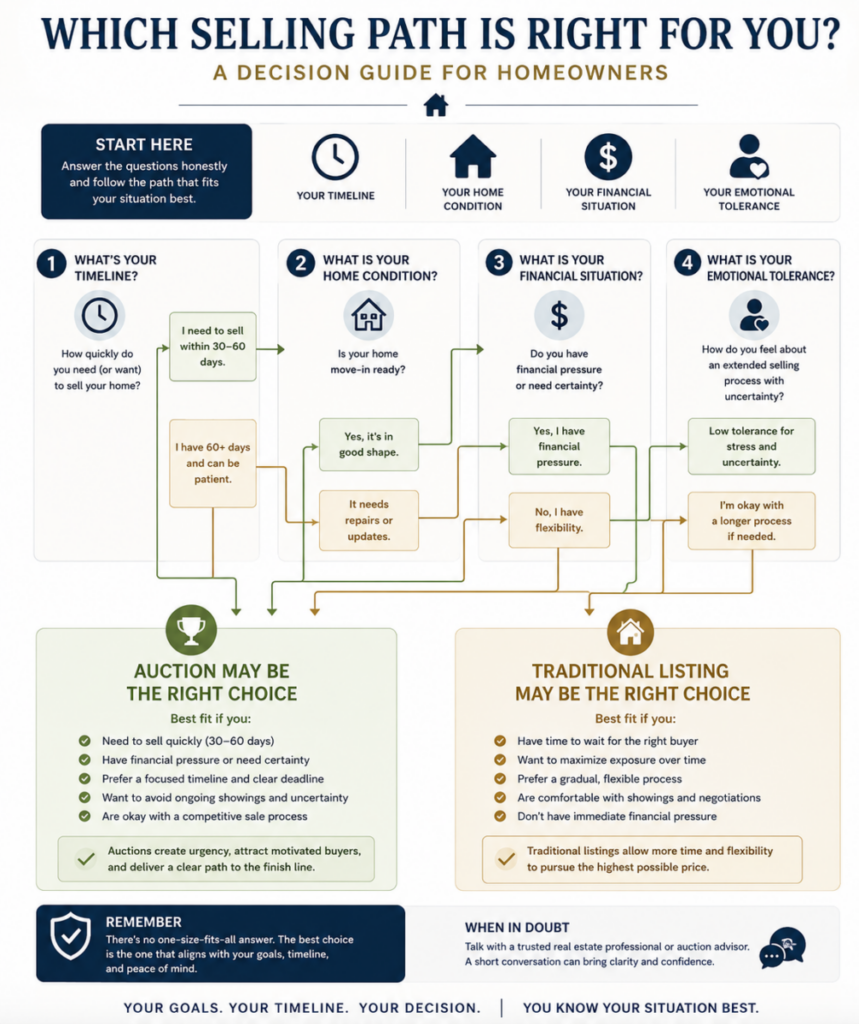

Section 13: Actionable Decision Framework & Checklist

To determine the most logical path for your specific situation, step through this sequential, data-driven decision framework:

- Audit your available liquid cash reserves: Calculate if you possess enough capital to cover a minimum of six months of carrying costs without touching your core retirement funds. If cash is tight, lean toward an auction.

- Evaluate the age and condition of major systems: Document the exact age of the roof, HVAC units, electrical systems, and plumbing. If multiple systems are near the end of their lifespan, a traditional buyer’s lender will likely demand expensive repairs, making an “as-is” auction highly attractive.

- Establish your true operational timeline: Define the exact date you need to relocate or access your home’s equity. If that timeline is under 60 days, traditional financing timelines are too risky, making an auction the logical choice.

- Analyze local market inventory metrics: Check the average days on market for homes of similar size in your neighborhood. If inventory is rising and homes are sitting for over 60 days, an auction will bypass that stagnation and guarantee a definitive sale date.

Internal Resources

To further protect your net worth during a senior housing transition, review these core guides on HousingAfter60.com:

Summary

Liquidating a large home after 60 is an operational business decision that must be guided by logic rather than emotion. Traditional listings remain the premier choice for well-maintained properties where the seller has the time and capital to attract emotional, retail buyers using institutional mortgage leverage. Real estate auctions are an incredibly powerful tool for unique properties, homes needing major repairs, or situations where speed and transactional certainty are critical. By calculating your true monthly carrying costs, avoiding common pricing mistakes, and conducting thorough due diligence on your real estate team, you can successfully protect your hard-earned equity and set yourself up for a stable retirement transition.

Related Questions (FAQ)

Do homes always sell for less at auction?

Not necessarily. While professional investors looking for a discount dominate the auction market, unique or luxury homes can see intense bidding wars that push prices well past traditional retail estimates. However, standard suburban homes in good repair usually achieve their highest price through a traditional listing.

Can you auction a luxury home with a mortgage?

Yes. You can sell a property with a mortgage at auction, provided the highest bid covers the outstanding balance of the loan, plus any auction fees and administrative costs. The mortgage is paid off directly out of the cash proceeds at closing, just like a traditional transaction.

Who pays the auctioneer fees?

In most modern auction structures, the auction company’s primary commission fee is structured as a Buyer’s Premium, which is added directly on top of the winning bid and paid by the buyer. The seller is typically only responsible for upfront marketing costs and standard title closing fees.

Are real estate auction sales cash only?

Yes, practically speaking. While an auction company does not care if a buyer secures a personal loan after the event, the purchase contract explicitly states that the sale is not contingent on financing. If a buyer’s financing fails, they forfeit their non-refundable 10% deposit to the seller.

How fast can an auction sale close?

An auction transaction typically closes within 21 to 30 days from the date of the auction event. Because all inspection and financing contingencies are stripped away, the title company can process the paperwork and transfer funds with maximum velocity.

Should seniors fix up a home before selling?

Seniors should focus only on minor, high-ROI tasks like deep cleaning, decluttering, and basic paint touch-ups. Major renovations rarely return their full cost at sale and add substantial timeline delay and stress to the transition process.

Chuck O’Dell (Bio)

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of hands-on real estate experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing fluff to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement. He focuses on delivering data-driven insights tailored directly to the 60+ demographic.

Written by Charles O’Dell, a former CPA and real estate investor with 23+ years of experience and over 100 successful property flips.