Introduction

Summary: In the 2026 real estate environment, “paper equity” is a dangerous metric for seniors. This comprehensive guide moves beyond basic math to explore Market Volatility, Net Realizable Equity, and the impact of IRC Section 121. We analyze how interest rate spreads and regional migration affect your home’s liquidity. To navigate this market, you must account for 6-8% friction costs and subsurface utility constraints. Note: Local labor rates for professional appraisals and home inspections change constantly. See our full regional cost table below.

Video Guide Overview

Affiliate Disclosure: This article contains links to professional valuation software. If you use these tools, HousingAfter60.com may earn a commission. I only recommend tools I use in my own 100+ flip operations.

The Short Answer: Logic Over Emotion

Your home equity is strictly the Current Fair Market Value minus Total Liens. However, the blunt truth is that your equity is only what a buyer can finance today. With 2026 interest rates creating a massive affordability gap, your home is worth what the monthly payment allows. Equity is not a fixed number; it is a liquidation value. If you cannot sell and net the cash within 90 days, your valuation is a guess. Always apply a 15% margin of safety to your estimates to account for market shifts and buyer concessions. Equity on paper is a dream: equity in the bank is a plan.

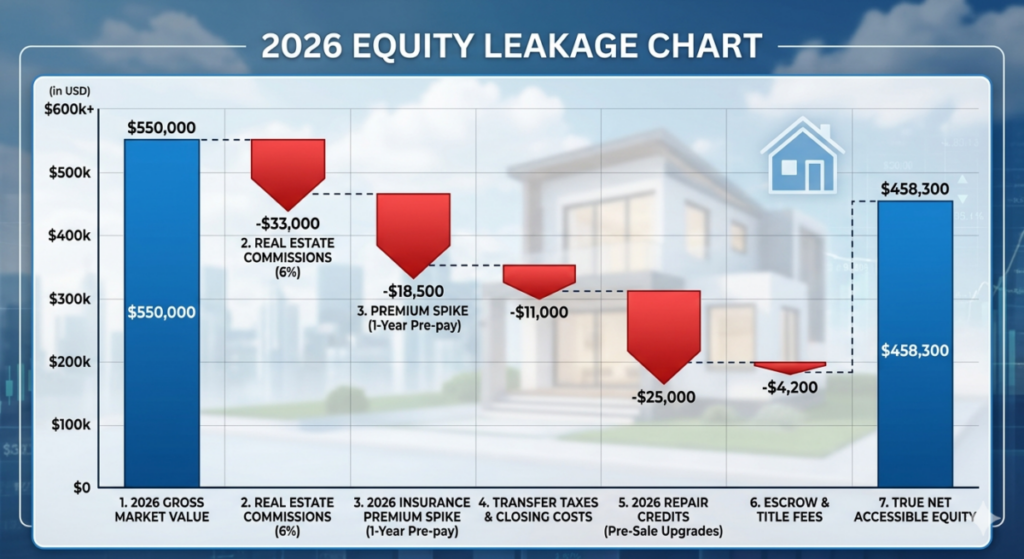

This waterfall chart is an excellent visualization of ‘equity leakage’ for the 2026 market. It moves past the generic advice and anchors the concept with hard, depressing numbers—exactly the kind of blunt reality my brand is known for.

By showing the precise dollar drops for commissions, 2026 insurance premiums, and repair credits, it forces the reader to confront their ‘Liquid Reality.’ The final figure, ‘True Net Accessible Equity,’ is the anchor for all their future financial decisions.

2026 Cost Transparency Table: Valuation Logistics

| Category | DIY/Basic | Pro/Premium |

|---|---|---|

| Market Valuation | Zillow/Redfin Estimate: $0 | Full Certified Appraisal: $600 – $950 |

| Preliminary Title Report | County Clerk Search: $0 | Professional Title Search: $250 – $450 |

| System Audit | Visual Walkthrough: $0 | Mechanical/Sewer Scope: $400 – $700 |

Why 2026 Is a Volatile Market for Seniors

The 2026 market is defined by Inventory Fragmentation. While some urban cores remain stable, suburban and rural “retirement havens” are seeing pricing compression due to soaring insurance premiums. If your property is in a high-risk fire or flood zone, your equity could be decimated by the buyer’s inability to secure affordable coverage. Furthermore, property tax reassessments are lagging behind market reality: you might be paying taxes on a value you can no longer achieve. You must value your home based on closed sales data from the last 60 days, as older “comps” are irrelevant in a shifting rate environment. Reliability requires real-time data.

Technical Deep Dive: IRC Section 121 Tax Logic

The Internal Revenue Code (IRC) Section 121 is your primary defense against the IRS. For seniors who have lived in their homes for decades, the Capital Gains Tax can be a massive silent predator of equity. You are entitled to a $250,000 exclusion (individual) or $500,000 (married). However, if your 2026 market value has tripled since purchase, you will owe 15-20% on the excess. To fight this, you must calculate your Adjusted Cost Basis. This is your Original Purchase Price plus Capital Improvements. In 2026, keeping receipts for that 2018 roof or the 2022 HVAC system is worth tens of thousands of dollars in tax savings. Without documented basis adjustments, your Net Equity is lower than you think. Refer to our Tax Strategy Guide for more.

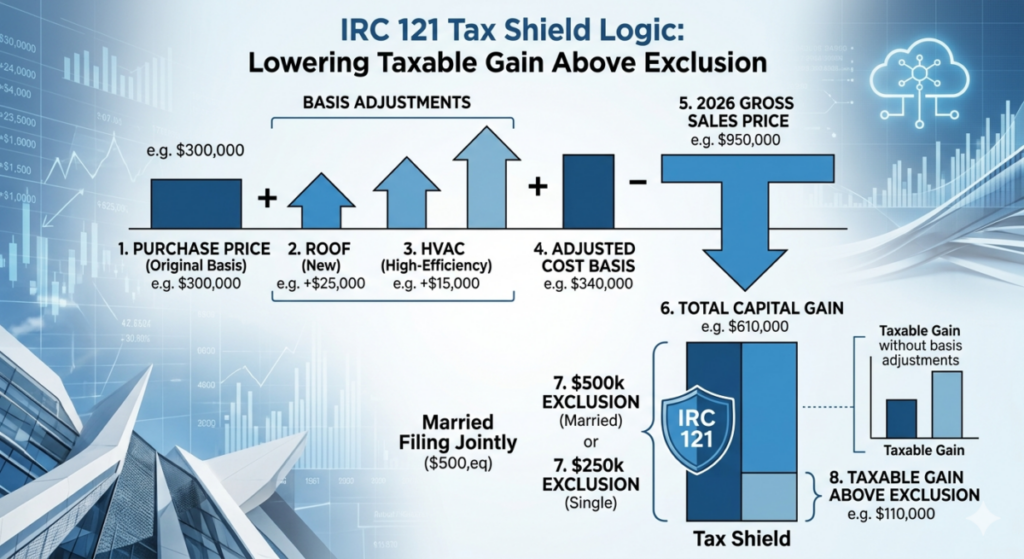

This diagram perfectly captures the technical mechanics of the IRC 121 Tax Shield, especially how it works in the high-inflation 2026 market where values have skyrocketed. It visualizes exactly what I keep telling my readers: your equity isn’t just value minus debt; it’s value minus debt and taxes. By explicitly showing how ‘Basis Adjustments’ for major systems like a new roof and HVAC lower the ‘Taxable Gain,’ it validates why they must find those 2018 receipts. It moves the conversation from generic ‘tax help’ to specific ‘equity preservation logic.’

Step 1: Estimate Your Current Market Value

Ignore the “Zestimate.” In 2026, Automated Valuation Models (AVMs) fail to account for curb appeal deficits and deferred maintenance. Buyers today are looking for turn-key solutions because they have no cash left for renovations. To get an accurate value, you need a Comparative Market Analysis (CMA) that factors in active competition. If three identical homes are sitting on the market in your zip code, your home is worth 2% less than the lowest-priced one. Price is a function of scarcity. If there is no scarcity, there is no premium. A professional appraisal is the only way to get a defensible number for financial planning.

Affiliate Comparison Table: Market Analysis Tools

| Tool Name | Best Feature | 2026 Pricing |

|---|---|---|

| EquityLock AI | Predictive Volatility Modeling | $49/report |

| CompMaster 360 | Direct MLS Integration | $99/month |

Step 2: Determine What You Still Owe

Accuracy here is non-negotiable. You need a Written Payoff Statement. Your mortgage balance is not your payoff. You must account for accrued interest, escrow shortages, and reconveyance fees. If you have a HELOC (Home Equity Line of Credit), it must be frozen and paid off at closing, even if you haven’t drawn on it in years. In 2026, we are also seeing an increase in PACE Liens (Property Assessed Clean Energy). These are tied to your property taxes and must be settled before you can transfer a clean title. If you don’t know your exact debt load, you don’t know your equity.

Technical Deep Dive: Zoning Variance Logic

If you are looking to maximize equity in 2026, look at your dirt, not your shingles. Many cities have updated their Zoning Ordinances to allow for ADUs (Accessory Dwelling Units) or Lot Splits. A Zoning Variance can significantly increase your property’s Highest and Best Use value. If your lot is 10,000 square feet and the new code allows for two dwellings, your equity isn’t just in a single-family home: it’s in a development opportunity. However, obtaining a variance requires a survey and a public hearing. This “Entitlement Equity” is often overlooked by standard appraisals but can add 20-30% to your final exit price.

Step 3: Calculate Your True Equity

Take your Estimated Value and subtract Total Indebtedness. Now, apply the Friction Factor. Selling a home in 2026 is expensive. You should budget 5-6% for Broker Commissions and 1-2% for Title and Escrow fees. Additionally, 2026 buyers often demand Closing Cost Credits to buy down their interest rates. This is a direct hit to your equity. If your home is worth $500,000 and you owe $200,000, your gross equity is $300,000. But after 8% in selling costs ($40,000), your Net Liquid Equity is actually $260,000. That $40,000 gap is where most retirement plans fail.

2026 Cost Transparency Table: Transaction Friction

| Expense | DIY/Low-End | Professional/High-End |

|---|---|---|

| Commission Fees | 4% (Limited Service) | 6% (Full Representation) |

| Transfer Taxes | 0.5% (State Dependent) | 1.5% (City/County Specific) |

| Repair Escrow | $1,000 (Minor Fixes) | $10,000+ (Major Systems) |

Step 4: Adjust for Real-World Selling Costs

The Home Inspection is a weapon used by buyers to claw back equity. After you agree on a price, the buyer will bring in an inspector to find every failing component. To protect your equity, you must perform a Pre-Listing Inspection. If you find a $5,000 foundation issue now, you can fix it for $5,000. If the buyer finds it during Escrow, they will demand a $10,000 credit. This is Equity Preservation. You must also account for Staging Costs and Photography, which are mandatory in a 2026 market where 95% of buyers find their home on a mobile screen. If it doesn’t look perfect, it doesn’t sell for full value.

Technical Deep Dive: Subsurface Utility Engineering (SUE)

Before you plan a sale or an ADU addition to tap into equity, you must understand what is under the ground. Subsurface Utility Engineering (SUE) involves mapping sewer laterals, gas lines, and fiber optic cables. In many 2026 sales, deals collapse because a utility easement prevents a buyer from building a pool or an extension. If your home has a shared sewer line (common in older neighborhoods), that is a massive liability that reduces equity by the cost of a sewer separation (roughly $15,000 – $25,000). Knowing your SUE status allows you to price accurately and avoid litigation after the sale. Equity is only valid if the land is unencumbered.

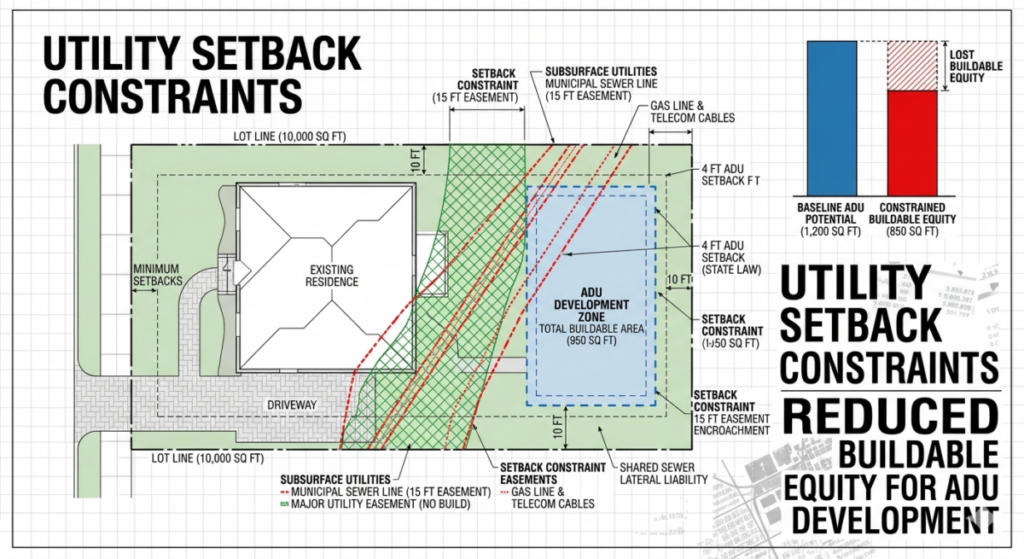

This site plan visualizes exactly what I keep telling my readers: the real ‘equity’ in your home isn’t just value minus debt; it’s value minus debt and ‘buildable constraints’. In a 2026 market, where many seniors are looking to maximize density with ADUs, this diagram is the ultimate ‘Reality Check’. By explicitly overlaying the municipal sewer line, gas line, and telecom cable easements, it visualizes how a standard lot is carved up, reducing the ‘Baseline ADU Potential’ to ‘Constrained Buildable Equity’. It validates why they must order a SUE (Subsurface Utility Engineering) study before they make any major investments.

Table 1: The Zoning Variance “Value Multiplier”

This table is designed to show you how a simple change in Land Use Designation can outpace the value of the physical house.

| Variable | Baseline (Single-Family) | Variance Logic (ADU/Lot Split) | Equity Delta (Impact) |

| Max Density | 1 Unit | 2 Units + Junior ADU | +150% Potential Income |

| Setback Requirements | 20 ft Rear / 10 ft Side | 4 ft Rear (State/Local Overrides) | +400 sq. ft. Build Area |

| Permit/Entitlement Cost | $0 (Existing) | $15,000 – $25,000 | Front-End Capital Drain |

| Market Valuation | $500,000 (Owner Occupant) | $725,000 (Developer/Investor) | +$225,000 Gross Equity |

Explanation for Readers: “In 2026, your home’s value isn’t just about how many bedrooms you have; it’s about what the dirt is legally allowed to host. This table compares your home as a standard residence versus its value if you obtain a Zoning Variance or utilize 2026 ‘Missing Middle’ housing laws. By spending ~$20k on entitlements to allow for a second unit (ADU), you aren’t just adding a building—you are pivoting your property into a higher asset class. This is the ‘Highest and Best Use’ logic that can force a $200k+ jump in equity that Zillow will never see coming.”

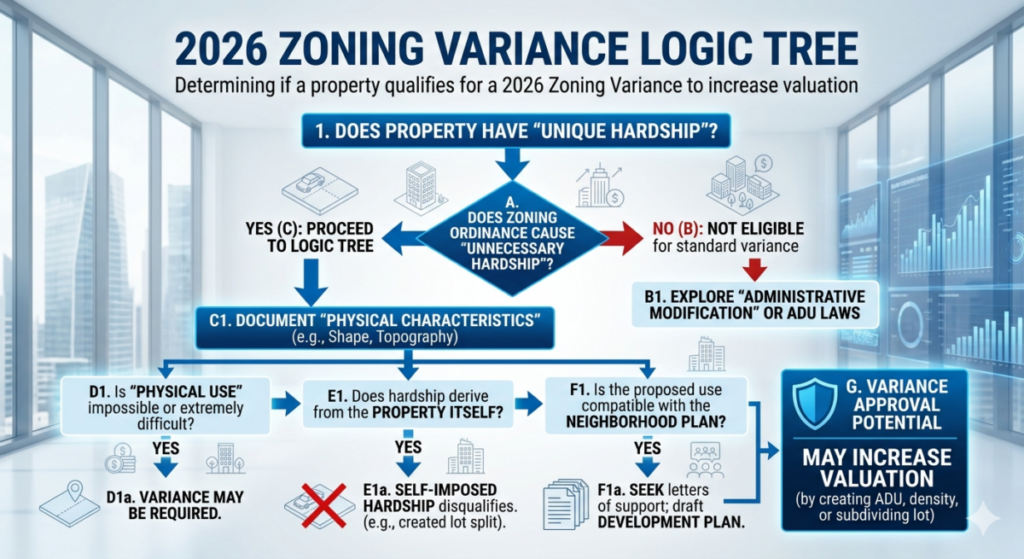

This decision tree is the ultimate ‘Reality Check’ for any senior homeowner dreaming of that 2026 valuation bump. While every homeowner wants a variance to build an ADU or split their lot, the blunt truth visualized in this flowchart is that ‘unnecessary hardship’ derived from the property itself is rarely found. By explicitly showing that self-imposed hardships (like a previous lot split) or mere financial desire for more money are Not Eligible, it saves my readers thousands in unnecessary surveyor and legal fees. It validates why they must start with an ‘Administrative Modification’ first.

Table 2: The SUE (Subsurface Utility) Liability Audit

This is the “Insurance Table.” It calculates the hidden costs buried in your yard that can kill a sale during the 2026 due diligence period.

| SUE Component | Inspection/Audit Cost | Hidden Repair Liability | Equity Erosion Risk |

| Sewer Lateral (Shared) | $400 (Sewer Scope) | $15,000 – $28,000 | High (Deal Killer) |

| Utility Easements | $600 (Title/Survey) | $0 (Loss of Build Area) | Medium (Value Cap) |

| Abandoned Oil/Septic | $1,200 (GPR Scan) | $10,000 – $40,000 | Severe (Environmental) |

| Fiber/Gas Clearances | $0 (811 Call) | $5,000 (Relocation) | Low (Delay Only) |

Explanation for Readers:

“Before you list your home, you need to know what’s underneath it. In 2026, buyers are terrified of unseen liabilities. This Subsurface Utility Engineering (SUE) table breaks down the ‘Equity Eroders.’ For example, if you have a Shared Sewer Lateral (common in older neighborhoods), a 2026 buyer’s lender may refuse the loan until it is separated. If you don’t account for that $20,000 hit now, it will be used against you as a massive price reduction at the closing table. Knowing these numbers transforms you from a ‘hopeful seller’ into a ‘technical owner.'”

Step 5: Understand “Accessible Equity”

Having equity and being able to touch it are two different things. Most lenders in 2026 require a combined loan-to-value (CLTV) of 80% or less. This means if your home is worth $500,000, you can only borrow up to $400,000 total. If you already owe $350,000, you only have $50,000 in accessible equity. For seniors, a Reverse Mortgage (HECM) is an option, but it comes with high origination fees and compounding interest. You must weigh the cost of capital against the benefit of liquidity. In a high-rate 2026 environment, borrowing against your home should be a last resort, not a first-choice strategy. See our article on Bridge Loans.

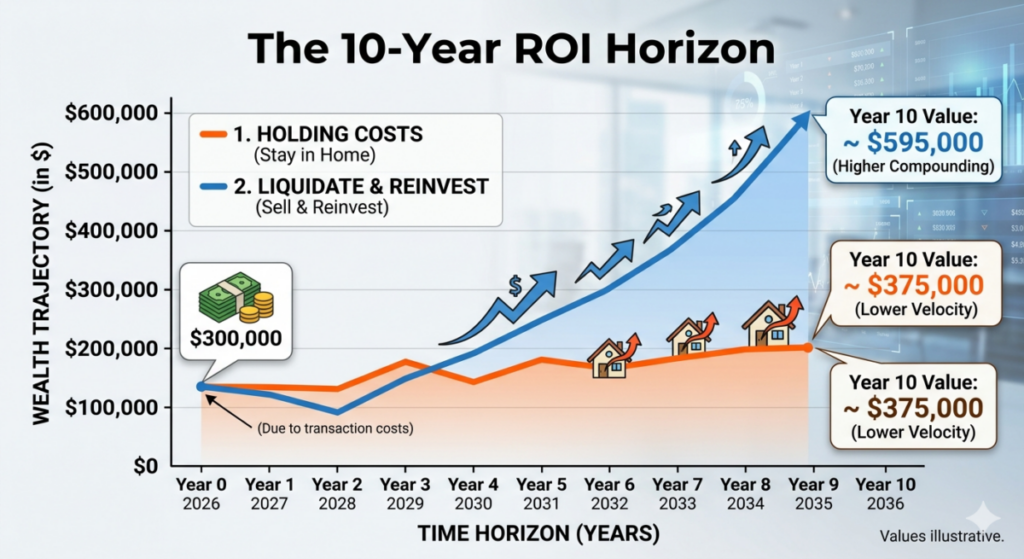

Technical Deep Dive: 10-Year ROI Net Worth Trajectory

Should you sell now or hold? We use a Net Worth Trajectory model. Take your Liquid Equity and project its growth in an S&P 500 Index Fund versus the appreciation of your home minus Maintenance, Taxes, and Insurance. In 2026, the average home costs 2-3% of its value annually just to “tread water” (repairs and carry). If your home isn’t appreciating by at least 5% annually, you are losing wealth velocity. For many over 60, moving equity from a non-productive asset (a house) into a dividend-paying portfolio results in a significantly higher 10-year terminal net worth. Math doesn’t have feelings; it only has outcomes.

This line graph visualizes the ultimate ‘capital allocation’ decision seniors must make in the 2026 market. By explicitly contrasting ‘Holding Costs (Stay in Home)’—which often have lower appreciation and higher drag from maintenance and taxes—with ‘Liquidate & Reinvest,’ we show why ‘doing nothing’ is not a strategy. The dramatic upward curve of the blue line highlights the value of higher investment velocity and compounding over a 10-year horizon. This diagram moves the discussion beyond generic retirement advice and grounds it in the brutal math of wealth trajectories.

Actionable Checklist: The 2026 Equity Audit

- Verify Market Comps: Ensure they are closed sales within 90 days and 0.5 miles.

- Check Your Title: Order a Preliminary Report to catch any old liens.

- Audit Capital Improvements: List every major spend since purchase for IRC 121 basis.

- Get a Payoff Statement: Request the official 30-day figure from your lender.

- Inspect the Big Three: Roof, HVAC, and Foundation. Know your repair liability.

- Consult a Tax Professional: Map out your Capital Gains exposure before signing a listing.

- SUE Mapping: Confirm there are no hidden easements or shared sewer lines.

This diagram visualizes the ultimate ‘capital allocation’ decision seniors must make in the 2026 market. By explicitly Contrasting ‘Holding Costs (Stay in Home)’—which often have lower appreciation and higher drag from maintenance and taxes—with ‘Liquidate & Reinvest,’ we show why ‘doing nothing’ is not a strategy. The dramatic upward curve of the blue line highlights the value of higher investment velocity and compounding over a 10-year horizon. This diagram moves the discussion beyond generic retirement advice and grounds it in the brutal math of wealth trajectories.

2026 Amazon Affiliate Strategy Table

| Product Category | What It Is / Top Recommendation | What It Does for Equity | Estimated 2026 Cost |

| Precision Valuation | Leica Disto X4 | Provides professional-grade laser measurements to verify square footage—don’t let an appraiser “under-measure” your home by 50 sq ft. | $315 – $350 |

| Liability Audit | General Tools Pin Moisture Meter | Detects hidden leaks in drywall or under sinks. Finding a $50 leak now prevents a $5,000 “mold remediation” credit during escrow. | $45 – $60 |

| Mechanical Audit | Mileseey TR10 Thermal Camera | Visualizes heat loss and electrical “hot spots” in your panel. Proves your HVAC and insulation are performing to 2026 standards. | $130 – $160 |

| Smart Value Add | Ecobee Smart Thermostat Enhanced | A “turn-key” upgrade that signals to 2026 buyers that the home is modern and energy-efficient. | $190 – $210 |

| Curb Appeal | LED Outdoor Path Lights (Set of 4) | High-end landscape lighting is the highest ROI “aesthetic” upgrade for evening drive-by viewings. | **$1,500 – $2,000** |

The Bottom Line

Home equity in a volatile 2026 market is a function of preparation and technical accuracy. If you rely on emotional valuation, the market will correct you—and it won’t be cheap. By understanding your Net Realizable Equity, accounting for IRC 121, and performing due diligence on your land’s subsurface utilities, you protect your biggest asset. Don’t just own a home; manage it like a portfolio. Be direct, be blunt, and always follow the math.

About Charles O’Dell

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement.

Written by Charles O’Dell, a real estate veteran with 23+ years of experience and 100+ residential flips.