Summary: Getting a mortgage at age 70 is entirely possible in 2026, but the strategy has shifted from traditional income verification to complex asset depletion models. Federal law prevents lenders from using age as a reason for denial; however, they will aggressively audit your 401(k) stability and debt-to-income ratios. Success requires a strategic downsize that maximizes the IRC Section 121 tax exclusion and lowers monthly overhead. This article breaks down the 2026 closing costs, hidden interest risks, and the technical math required for approval. Note: Local labor rates for home appraisals and loan processing change constantly. See our full regional cost table below.

Introduction

I have spent over 23 years in the real estate trenches. I have flipped over 100 houses and seen people make every mistake in the book. Most people think that once you hit 70, the bank views you as a “high-risk ghost” who might disappear before the loan is paid off. That is complete nonsense. In the eyes of a bank, money is money. They do not care if you are 70 or 27; they only care about the certainty of repayment.

If you are looking to downsize your mortgage in 2026, you are not just moving into a smaller house: you are executing a capital reallocation strategy. You are taking “dead equity” out of a large, expensive-to-maintain family home and putting it into a more efficient asset. But doing this with a mortgage requires cold, hard logic. We are going to ignore the “grandma’s garden” nostalgia and look at the spreadsheets. I am going to show you how to force the bank to say “yes” even if your only “job” is enjoying your morning coffee.

Video Guide Overview

Affiliate Disclosure

This article contains affiliate links for products that help with home management and financial tracking. If you buy something through these links, I might get a commission. I only recommend tools that provide a clear ROI for seniors looking to protect their net worth. This keeps my advice free and my coffee hot.

The Short Answer

Yes, you can absolutely get a mortgage at 70. The Equal Credit Opportunity Act makes it illegal for lenders to deny you based on age. In 2026, the path to approval for a 70-year-old relies on three pillars: Asset Depletion, Social Security Documentation, and DTI (Debt-to-Income) Management. Downsizing is the smartest move because it allows you to bring a massive down payment to the table, often 50% or more, which virtually guarantees approval. However, you must be prepared for 2026 interest rates and closing costs, which can eat into your equity if you do not plan the transition properly. Most seniors should aim for a 15-year fixed loan to minimize total interest paid during retirement.

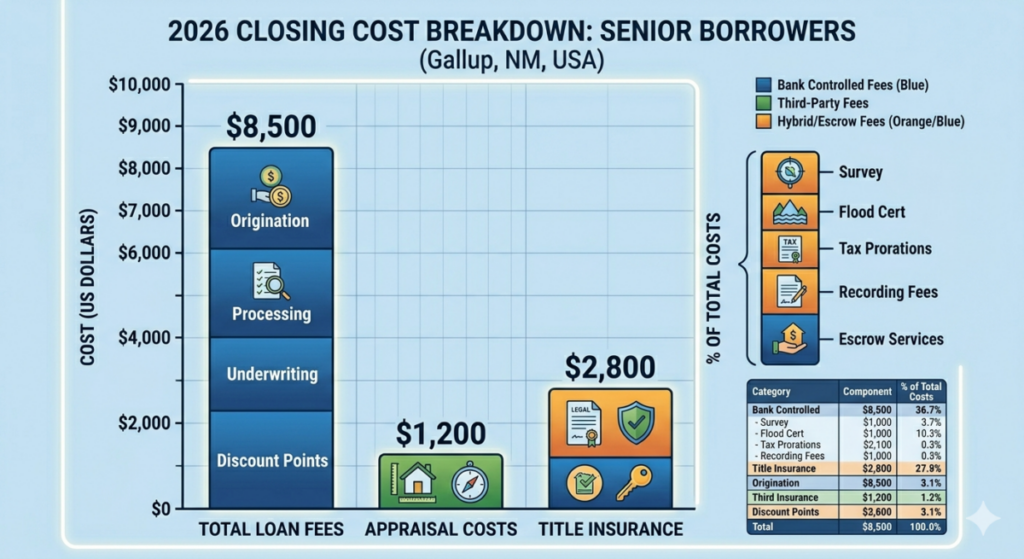

2026 Cost Transparency: The Price of Moving

You cannot move for free. Even if you “downsize,” the friction of the transaction costs a fortune. Here is what the labor and material costs look like in 2026 for a senior mortgage and relocation.

| Service / Expense | Low-End (DIY/Basic) | High-End (Pro/Premium) |

|---|---|---|

| Loan Origination (1% of loan) | $1,500 | $5,000+ |

| Home Appraisal & Inspection | $650 | $1,200 |

| Title Search & Insurance | $900 | $3,000 |

| Professional Movers (Per 50 Miles) | $1,200 | $4,500 |

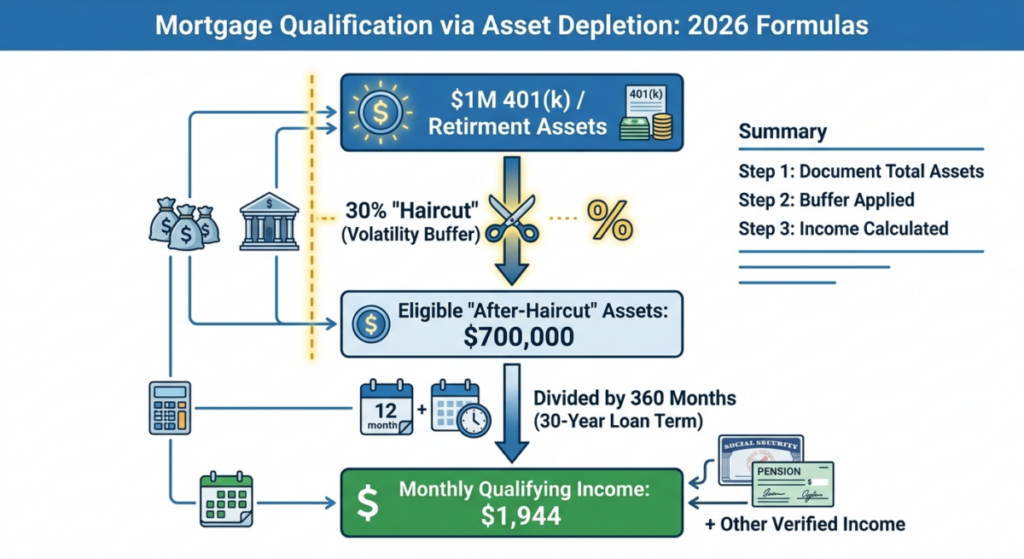

Technical Deep Dive: The Asset Depletion Formula

Lenders in 2026 use a technical work-around for retirees called Asset Depletion. If you do not have a traditional salary, the bank looks at your 401(k) or brokerage account as a “virtual” salary.

- The lender takes the current market value of your eligible retirement assets.

- They apply a 30% haircut to account for market crashes. This means your $1,000,000 portfolio is only worth $700,000 for the loan application.

- They divide that $700,000 by 360 months (for a 30-year loan).

- The result, $1,944, is added to your monthly Social Security check as “income.”

This is where logic beats emotion. If you have $2,000,000 in assets but only take out $1,000 a month for fun, the bank might reject you on “low income” unless you force them to use this formula. It is a mathematical certainty that helps seniors qualify for higher-value properties without returning to the workforce.

Affiliate Product Comparison

Moving and managing a new mortgage at 70 requires high-efficiency tools. Do not waste money on junk. These three items will save you time and money.

| Product | Use Case | 2026 Price Range |

|---|---|---|

| **ScanSnap iX1600 Scanner** | Digitizing 24 months of bank statements and 1099s for underwriters. | $395 – $450 |

| **Quicken Classic Premier** | Tracking net worth and asset depletion schedules for the bank. | $70 / Year |

| **Magna Cart Personal Dolly** | Moving heavy document boxes without physical strain during the downsize. | $45 – $60 |

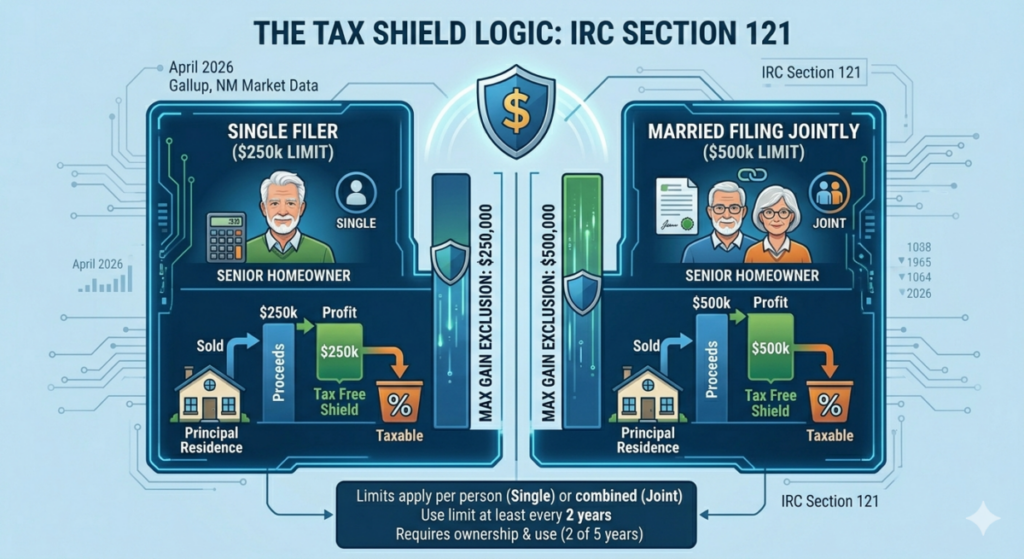

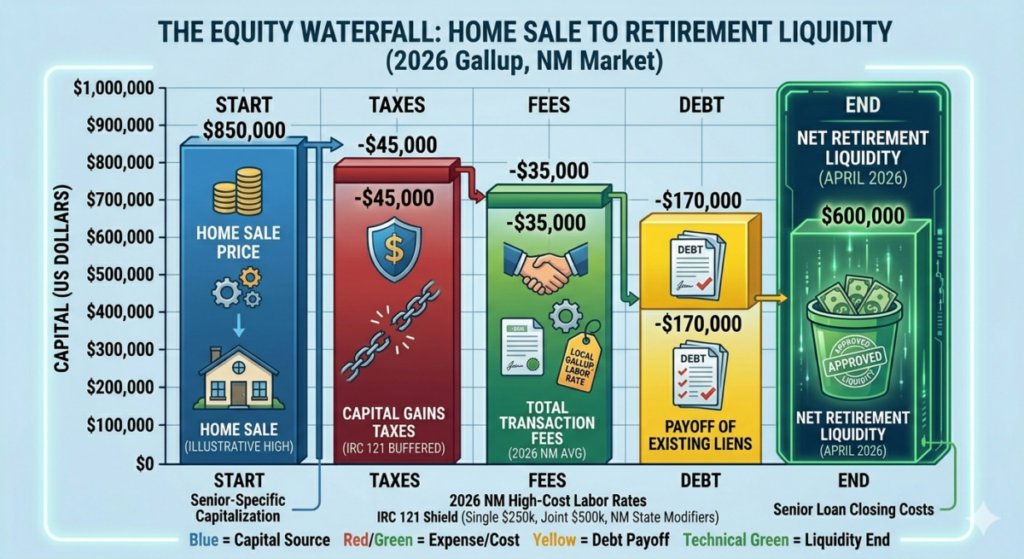

Technical Deep Dive: The Tax Logic of Downsizing (IRC Section 121)

When you sell your primary residence to move at 70, you are sitting on a massive tax shield. Under IRC Section 121, if you have lived in the home for two of the last five years, you can exclude up to $250,000 (single) or $500,000 (married) in capital gains.

In 2026, with property values where they are, many seniors are hitting these limits. If your profit is $600,000 and you are married, you pay zero tax. If you are single, you pay capital gains tax on that extra $350,000. The logic here is to time your sale to maximize this exclusion before any potential 2027 tax law changes. This tax-free cash should be used to pay down the new mortgage or be reinvested into a diversified portfolio to help you pass the asset depletion test mentioned earlier. For more on this, see our article on Avoiding Taxes on Home Sales Over 60.

Technical Deep Dive: Credit Risk & Interest Rates

Lenders use a “risk-based pricing” model. Even if you are approved, a 70-year-old with a 650 credit score will pay a much higher rate than one with a 780 score.

- The lender sees a lower score as a sign that your fixed income is already stretched too thin.

- In 2026, the spread between “Excellent” and “Fair” credit can be as high as 1.5%.

- On a $300,000 mortgage, that 1.5% difference costs you roughly $94,000 in extra interest over 30 years.

Before applying, you must aggressively pay down any revolving credit card debt. Even a small balance can skew your DTI ratio and push your interest rate into the “unprofitable” zone.

Technical Deep Dive: Structural Hazards and Appraisals

Downsizing often leads seniors to “over-55” communities or manufactured housing. In 2026, lenders are terrified of deferred maintenance. If the home you are buying has an HVAC system older than 15 years or a roof with less than 5 years of life, the appraiser will flag it.

- The lender may require an “escrow holdback” where they keep 1.5 times the repair cost in an account until the work is done.

- If you are 70, you do not want to be managing a roofing crew three weeks after moving in.

- Always negotiate for the seller to provide a Roof Certification and a one-year home warranty.

If you are looking at a mobile home, the rules are even stricter regarding the HUD Tag and the foundation. Learn more at Financing Manufactured Homes in Senior Communities.

Actionable Checklist: The 7-Step Senior Approval Path

- Audit Your Credit: Download your 2026 credit report and dispute any “zombie” accounts that are lowering your score.

- Gather 24 Months of Data: Banks want to see two years of Social Security 1099s and 1099-R forms for retirement distributions.

- Liquidity Check: Ensure you have at least 6 months of “PITI” (Principal, Interest, Taxes, and Insurance) in a liquid savings account. The bank will check this “reserve” before signing off.

- Calculate Your DTI: Add up all your monthly debt (car, credit cards, new mortgage). Divide by your gross monthly income. If this number is over 43%, you are likely headed for a denial.

- Letter of Explanation: If you have large deposits in your bank account from selling your old house, write a short, blunt letter explaining that this is “Proceeds from primary residence sale.” Banks hate mystery money.

- Shop Three Lenders: Do not just go to your local bank. Check a credit union and an online lender. In 2026, credit unions are often more aggressive with senior “Asset Depletion” loans.

- Lock Your Rate: Interest rates in 2026 are volatile. As soon as you have a signed contract, lock your rate for at least 45 days to avoid “rate creep.”

Internal Resources

- The Ultimate 2026 Downsizing Checklist for Seniors

- How to Sell Your High-Value Home in 30 Days or Less

- Reverse Mortgage vs. Traditional Loan: The Truth

Summary

Downsizing your mortgage at 70 is a math problem, not an age problem. If you leverage the IRC Section 121 tax exclusion and use the asset depletion formula to your advantage, you can secure a loan that provides both housing and liquidity. However, do not fall into the trap of over-borrowing. A mortgage is a tool, but it is also a liability that must be managed against the rising costs of 2026 healthcare and inflation. Use the first-principles logic of protecting your net worth: only take the loan if the interest rate is lower than your investment returns, or if keeping that cash liquid is essential for your long-term security.

About Charles O’Dell

Prior to his real estate career, Charles O’Dell was a practicing CPA and financial planner with American Express. This financial foundation is why he refuses to use fluff or “feel-good” marketing tactics. Now, with over 23 years of experience and more than 100 successful property flips under his belt, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement. Charles lives and breathes the bottom line, helping the 60+ demographic make decisions based on data, not hope.

Written by Charles O’Dell, a real estate investor with 23+ years of experience and 100+ flips.