Introduction

Summary: Being “House Rich, Cash Poor” means your net worth looks great on paper, but you cannot buy a gallon of milk with a brick from your chimney. In 2026, rising property taxes and insurance premiums make this a dangerous trap for those over 60. This guide provides first-principles logic to help you calculate your liquidity ratio, evaluate the 2026 costs of downsizing versus reverse mortgages, and rebalance your portfolio for maximum cash flow. You need more than a roof; you need a strategy that pays the bills.

Note: Local labor rates for home maintenance and relocation services change constantly. See our full regional cost table below.

Video Overview Guide

Affiliate Disclosure: Some links in this article are affiliate links. If you purchase through them, I may earn a commission at no extra cost to you. I only recommend tools that provide logical value to your real estate strategy.

The “Short” Answer: Why Your Home Is Not an ATM

In simple terms, being “house rich and cash poor” means you own an expensive asset (your home) but lack the liquid cash (money in the bank) to live comfortably. After age 60, this is a recipe for disaster. Your home equity is “trapped” wealth. Unless you sell, borrow against it, or rent it out, that equity does exactly zero to help you pay for groceries, healthcare, or a trip to see the grandkids. In 2026, we are seeing property insurance rates skyrocket in many regions, turning “paid-off” homes into expensive liabilities. If 70% or more of your net worth is tied up in your primary residence, you are effectively betting your entire retirement on a single piece of real estate. Real investors call that “lack of diversification.” I call it a ticking time bomb for your lifestyle.

The Psychology of the Real Estate Trap

Most people over 60 are emotionally attached to their homes. I get it. You raised kids there. You measured their height on the pantry door. But from a first-principles logic perspective, a house is a box where you store your stuff and your body. If that box costs $3,000 a month in taxes, insurance, and repairs, but you only bring in $4,000 from Social Security, you are one broken water heater away from a financial crisis. Humor me for a second: would you take $500,000 out of your bank account and bury it in your backyard? Of course not. But that is exactly what you are doing when you sit on massive home equity while struggling to pay monthly bills. You are literally living on top of your retirement fund instead of living off of it.

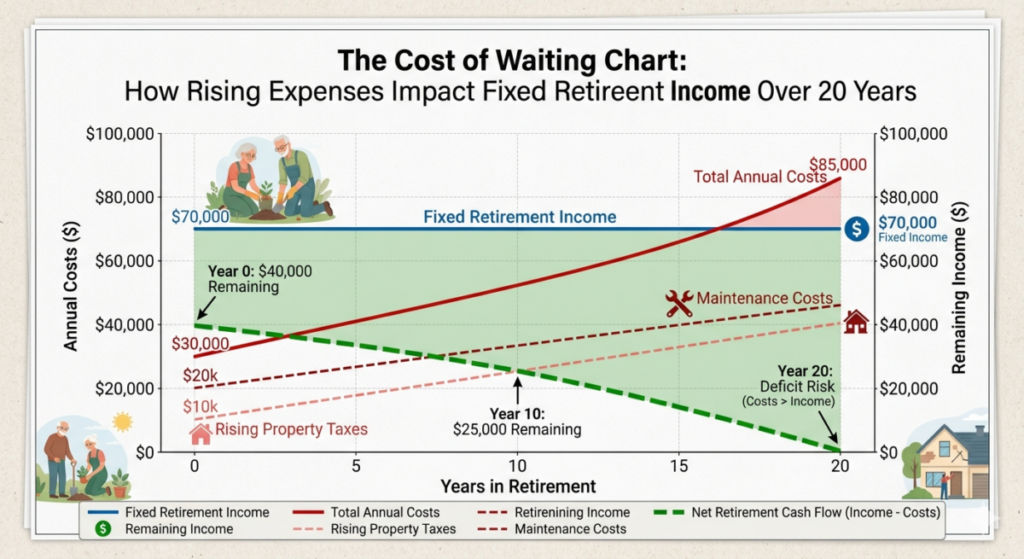

Technical Deep Dive: The Inflationary Tax Trap in 2026

Property taxes are not static. In 2026, many jurisdictions have completed their post-pandemic reassessments. If your home value jumped 40% in the last few years, your tax bill is following suit. Even if your mortgage is paid off, “carrying costs” are rising faster than Social Security COLAs (Cost of Living Adjustments).

- Mill Levies: Many local governments are increasing millage rates to cover infrastructure costs, meaning your tax bill can rise even if your home value stays flat.

- Assessment Caps: Some states have caps on how much an assessment can rise, but these often reset the moment you make a major repair or if the “homestead exemption” is not filed correctly.

- Insurance Hardening: The 2026 insurance market is “hard,” meaning carriers are pulling out of high-risk areas. If your home is older, you may be forced into “Fair Access to Insurance Requirements” (FAIR) plans, which are significantly more expensive.

These costs are the “leak” in your financial bucket. You cannot ignore them just because you like your neighbors.

Understanding Your Current Financial Position

Before you can fix the problem, you have to admit you have one. This requires a cold, hard look at the numbers. Disregard what you “think” the house is worth based on what your neighbor said at the BBQ. Look at the actual data.

Step 1: Calculate Your True Net Worth

- Get a realistic valuation of your home using a professional appraisal or a broker price opinion (BPO). Do not trust “Zestimates.”

- Subtract every penny of debt tied to the property, including HELOCs or solar panel liens.

- List every liquid asset: checking, savings, brokerage accounts, and the cash under your mattress.

- Divide your liquid assets by your total net worth. If the result is less than 0.20 (20%), you are officially house rich and cash poor.

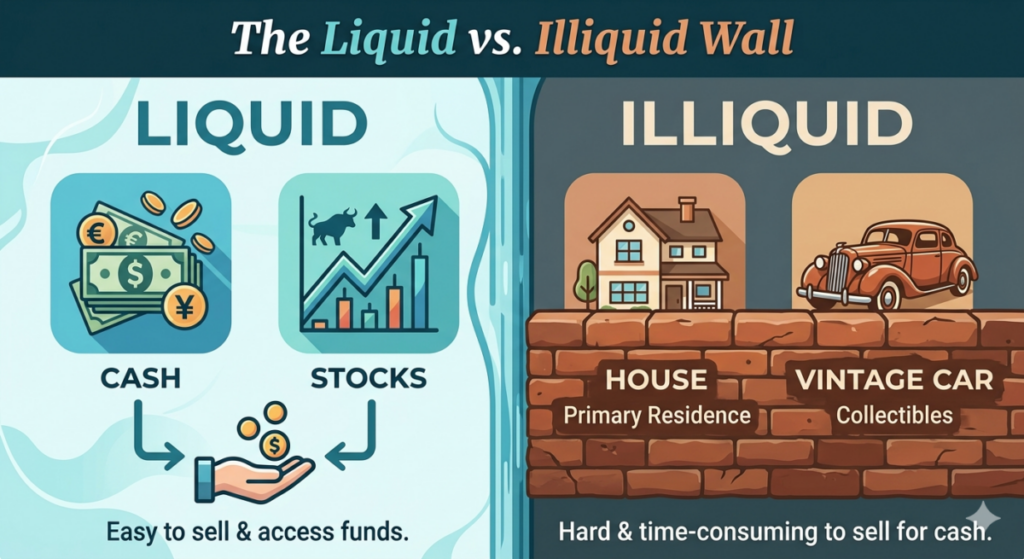

Step 2: Identify Liquid vs. Illiquid Assets

Liquidity is the ability to turn an asset into cash quickly without losing significant value. Your home is the ultimate “illiquid” asset. It takes months to sell and costs roughly 8% to 10% in transaction fees to exit. If you need $50,000 for a medical emergency tomorrow, your home equity is useless. You need a balance. Logic dictates that as you age, your need for liquidity increases because your ability to “earn” your way out of a hole decreases.

Technical Deep Dive: 2026 Liquidity Ratios for Seniors

Financial planners often use the “Current Ratio,” but for those over 60, I prefer the “Housing-to-Equity Ratio.” In a high-interest environment like 2026, the opportunity cost of “dead equity” is massive. If you have $400,000 in home equity and it is earning 0% while a safe Treasury bond is paying 4% to 5%, you are effectively “losing” $16,000 to $20,000 a year in potential income. That is a luxury vacation or a year of premium healthcare you are throwing away just to stay in a specific zip code.

2026 Cost Transparency Table: Rebalancing Options

To make a logical decision, you must compare the costs of staying versus the costs of moving or borrowing. Here is how the numbers look in 2026.

| Rebalancing Strategy | Low-End Cost (Basic) | High-End Cost (Premium) | 2026 Impact on Cash Flow |

|---|---|---|---|

| Downsizing (Local) | $15,000 (Moving/Fees) | $55,000+ (Commissions/Tax) | High Increase |

| Reverse Mortgage (HECM) | $6,000 (Closing Costs) | $25,000+ (FHA Insurance) | Moderate Increase |

| HELOC (Interest Only) | $500 (Appraisal) | $2,500 (Origination) | Decreases Cash Flow |

| Staying in Place (Maintenance) | $4,000/year (DIY) | $12,000/year (Pro) | Constant Drain |

Affiliate Products for Financial Management

To manage your transition, you need the right tools to track your data and secure your documents. Here are the logical choices for 2026.

| Product Name | Best For | Why It’s Needed |

|---|---|---|

| Fireproof Document Safe | Title/Deed Storage | Keeps original closing docs and appraisals safe from disasters. |

| Digital Property Scanner | Expense Tracking | Digitize every repair receipt to prove basis and lower capital gains tax. |

| Precision Laser Measure | Downsizing Planning | Determine exactly what furniture fits in a smaller condo before you move. |

The Risks of Staying in This Position

Hope is not a strategy. Many seniors think, “I’ll just wait until I have to move.” By then, you have lost the power of choice. If you have a medical crisis and are forced to sell in 30 days, you will take a “haircut” on the price. You might be selling into a down market. Even worse, you might be so “cash poor” that you cannot afford the repairs needed to get top dollar for the house. It is a vicious cycle. You are essentially letting the house own you.

Technical Deep Dive: Opportunity Cost and 10-Year Net Worth Trajectories

Let’s look at the math. If you have a $700,000 home with no mortgage and $20,000 in savings, your net worth is $720,000.

- Scenario A (Stay): The house appreciates at 3% per year. In 10 years, it is worth $940,000. But you spent $100,000 in taxes, insurance, and repairs over that decade. Your “real” net worth growth is minimal, and your lifestyle was “poor” because you had no cash.

- Scenario B (Rebalance): You sell the house, pay $50,000 in fees, buy a $400,000 condo, and invest the remaining $250,000 in a balanced portfolio yielding 6%. In 10 years, your condo is worth $537,000, and your investment account has grown to nearly $450,000. Total net worth: $987,000.

Scenario B gives you more money AND $15,000 a year in passive income to spend. Logic wins every time.

Options to Rebalance Your Portfolio

You have six main levers to pull. Some are better than others depending on your “stomach” for change.

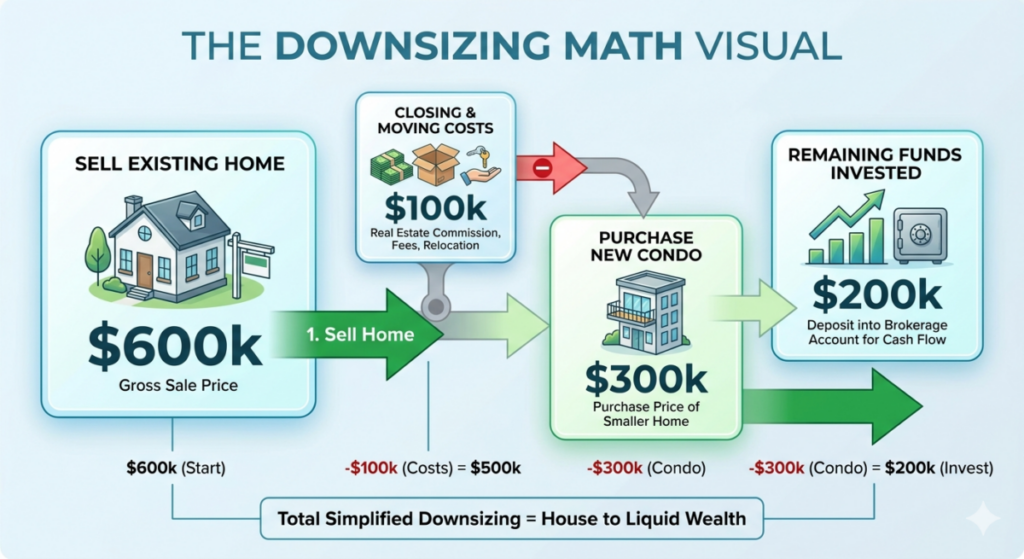

Option 1: Downsizing Your Home

This is the cleanest logical break. You sell a big, expensive asset and buy a smaller, cheaper one.

- Calculate the “Net Proceeds” after 6% commission and 2% closing costs.

- Identify a target market with lower property taxes.

- Account for the “Move-In” costs, which usually include new paint and light fixtures.

- Set aside the surplus into a liquid, interest-bearing account.

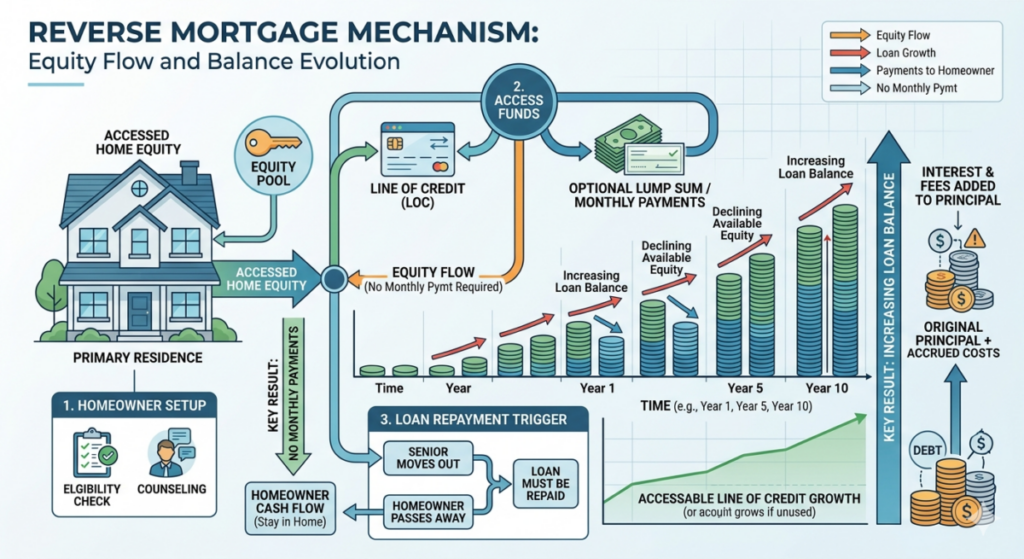

Option 2: The Reverse Mortgage (HECM)

I have seen these save people, and I have seen them mismanaged. A HECM allows you to access equity without a monthly payment.

- You must be at least 62 years old.

- The loan is repaid when you move out, sell, or pass away.

- You must still pay taxes and insurance. If you fail at this, the bank can foreclose.

- In 2026, interest rates on these are higher than in the past, meaning your equity disappears faster.

Technical Deep Dive: Regulatory Hurdles and Zoning in 2026

If you consider “House Hacking” (renting out a basement) to increase cash flow, you must check local 2026 zoning laws. Many HOAs and municipalities have cracked down on Short Term Rentals (STRs).

- ADU Laws: Some states have passed laws making it easier to build “Granny Flats.” This can increase your property value while providing rental income.

- Occupancy Limits: Check for “unrelated person” ordinances that might prevent you from taking in a roommate.

- Permit Costs: In 2026, permit fees for converting space have risen 15% on average due to municipal budget shortfalls.

Real-World Scenarios: The Math in Action

Example 1: The “Frozen” Retiree

Bob and Linda own a $850,000 home in California. They have $15,000 in savings. Their property tax is $9,000/year. They refuse to move because they like their rose garden. When Bob needs knee surgery, they have to put the $8,000 deductible on a credit card at 24% interest. They are “millionaires” who can’t afford a surgery. This is illogical.

Example 2: The Strategic Relocator

Susan sells her $600,000 home in a high-tax state. She moves to a $350,000 manufactured home in a land-lease community. She pockets $200,000. That money goes into a high-yield account. Her monthly income jumps by $1,200. She now travels twice a year and has zero stress when the car needs new tires. She is winning at life.

Actionable Checklist: Are You Financially Balanced?

- Calculate Liquidity: Is your cash-to-equity ratio above 20%? If no, proceed to the next step.

- Review Tax Bills: Compare your 2024 vs 2026 property tax. If it rose more than 10%, your cash flow is under attack.

- Audit Housing Costs: Total your taxes, insurance, and maintenance. If this exceeds 40% of your monthly income, you are in the “Danger Zone.”

- Check Emergency Fund: Do you have 12 months of expenses in a liquid account? If you are using credit cards for repairs, you are failing.

- Consult a Professional: Speak to a CPA regarding the $250k/$500k capital gains exclusion before you sell.

Internal Resources

- Check out our guide on mobile home investing to see how low-cost housing can save your retirement.

- Learn about the hidden costs of aging in place before you decide to stay.

- Read our analysis of 2026 real estate market trends for seniors.

Summary

The “House Rich, Cash Poor” trap is a choice, not a destiny. In 2026, the cost of holding onto “dead equity” is higher than ever due to inflation and rising carrying costs. By applying first-principles logic, you can see that your home is a tool for your life, not a shrine to your past. Rebalancing your portfolio by downsizing, relocating, or using home equity products can transform you from a stressed homeowner into a secure retiree with the cash flow to actually enjoy your life. Don’t wait for a crisis to force your hand. Make the move while you are still the one in the driver’s seat.

About the Author: Charles O’Dell

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement. Charles focuses on the 60+ demographic, ensuring that equity isn’t just a number on a page, but a functional asset that provides security and freedom.

Written by Charles O’Dell, a real estate investor with 23+ years of experience and 100+ successful property flips.