Introduction

Summary: In 2026, the traditional 4% Rule for retirement spending is being crushed by 16% insurance hikes and rising property taxes. To survive a 30-year retirement, your total housing costs—including “hidden” maintenance—must stay below 30% of your total draw. If your home eats 40% or more, you aren’t “aging in place”; you are “evicting your future self.” This guide breaks down the exact 2026 math you need to stay solvent.

Note: Local labor rates for home maintenance change constantly. See our full regional cost table below.

Video Guide Overview (4% Rule)

Affiliate Disclosure

I’m a straight shooter. To keep this site running without selling my soul to a big bank, I include links to products I actually use. If you buy through these links, I get a small commission at no extra cost to you. I only recommend tools that protect your bottom line.

The “Short” Answer (4% Rule)

The 4% Rule states you can safely withdraw 4% of your total retirement savings in your first year of retirement (adjusted for inflation thereafter) without running out of money for 30 years. In 2026, the math is blunt: your monthly housing payment is the largest variable you can control. For most seniors, housing should consume no more than 25% to 30% of that 4% draw plus Social Security. If you have $1,000,000 saved, your 4% draw is $40,000 a year, or $3,333 a month. If your mortgage, taxes, and insurance total $2,000, you are spending 60% of your “allowance” on a roof. That is a recipe for disaster. You need a buffer for healthcare and the inevitable $15,000 HVAC replacement that 2026 labor rates will demand.

What Is the 4% Rule (Plain English Explanation)

The Simple Idea

Think of your retirement savings like a giant bucket of water. You need that water to last through a 30-year drought. If you drink too much too fast, you die of thirst in year 20. The 4% Rule is the “sipping” speed. By taking out only 4% a year, you allow the remaining 96% to keep growing in the stock market, hopefully replenishing what you took. It’s a balancing act between your greed today and your needs at age 90.

Quick Example

Let’s look at the raw 2026 withdrawal numbers: * $500,000 savings: You get roughly $20,000 a year. That’s $1,666 a month. * $1,000,000 savings: You get $40,000 a year. That’s $3,333 a month. * $2,000,000 savings: You get $80,000 a year. That’s $6,666 a month. If those numbers look small, welcome to reality. This is why I tell people that a “paid-off home” is the best investment you’ll ever make. It lowers the “sip” you need from the bucket.

Why It Matters for Housing

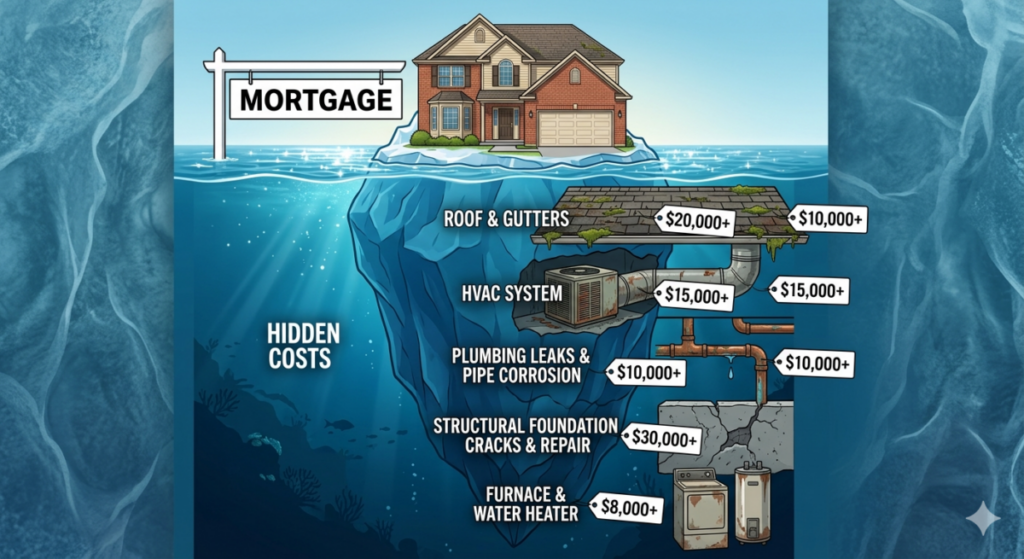

Your home isn’t just a place to sleep: it’s a liability that masquerades as an asset. Unlike a stock portfolio, you can’t sell 2% of your kitchen to pay for groceries. Housing is a “lumpy” expense. It’s steady until the roof leaks, then it’s a $20,000 punch to the gut. If you are already at the limit of your 4% draw, one bad storm in 2026 can break your entire financial plan.

Technical Deep Dive: The 2026 Economic Reality

In 2026, we are dealing with the fallout of the “One Big Beautiful Bill” (OBBBA). While it provided an enhanced standard deduction for seniors, it didn’t stop the “Insurance Cliff.” In states like California and Florida, premiums are rising by 16% this year alone. If you’re using the 4% Rule based on 2020 data, you’re already behind.

I’ve seen 100+ flips where the owners “felt” rich because their house value went up. But as a former CPA, I’ll tell you: You can’t eat equity. If your $800,000 home costs you $3,000 a month in carry costs, and your 4% draw only gives you $4,000, you are “house poor.” You have $1,000 left for food, medicine, and travel. That’s not a retirement: that’s a prison with a nice lawn.

| 2026 Cost Transparency Table | Low-End (DIY/Basic) | High-End (Pro/Premium) |

| Labor (Per Hour) | $45 – $65 (Handyman) | $125 – $250 (Specialized Trade) |

| HVAC Replacement | $6,000 (Window/Mini-split) | $18,000 (Full Central/High Efficiency) |

| Property Tax (National Avg) | 0.38% (Alabama) | 2.23% (New Jersey) |

| Home Insurance (Annual) | $1,200 (Low Risk) | $6,000+ (High Risk/Coastal) |

What Counts as a “Monthly Housing Payment” in Retirement

Not Just the Mortgage

Most people look at their P&I (Principal and Interest) and think they’re done. Wrong. In retirement, the mortgage is often the smallest part of the headache. You have: * Property Taxes: These never go away. In 2026, many municipalities are reassessing values to catch up with the post-pandemic boom. * Homeowners Insurance: As mentioned, this is the “silent killer” of retirement budgets. * HOA Fees: These are notorious for “special assessments.” If the condo roof needs a fix, you might get a $10,000 bill with a 30-day due date.

Often Forgotten Costs

I call these the “Wealth Eroder” costs. You should budget 1% to 2% of your home’s value every year for maintenance. On a $500,000 home, that’s $5,000 to $10,000. If you don’t spend it this year, save it for next year. The house *will* demand its tribute eventually. * Utilities: Energy costs in 2026 are volatile. * Major Replacements: A roof lasts 20 years. If you bought your house 18 years ago, you have a $25,000 bill coming.

Real-World Monthly Example: The $400,000 “Modest” Home

Let’s look at the actual carry costs for a “modest” $400,000 home in 2026. Most retirees underestimate these numbers because they forget that inflation doesn’t just hit the grocery store—it hits the hardware store and the tax office too.

| 2026 Monthly Housing Expense | Estimated Monthly Cost | Why This Number? |

| Mortgage (P&I) | $1,500 | Based on a standard fixed-rate loan. |

| Property Taxes (1.2%) | $400 | 2026 average; much higher in states like NJ or IL. |

| Home Insurance | $250 | Reflects the 2026 national average hike. |

| Maintenance Fund (1.2%) | $400 | The 1.2% Rule for 2026 labor/material rates. |

| Utilities | $300 | Covers electricity, water, and gas spikes. |

| TOTAL MONTHLY COST | $2,850 | Your baseline “survival” cost. |

The “4% Rule” Reality Check

To pay that $2,850 monthly bill using only the 4% Rule, you would need a $855,000 nest egg just to keep the lights on and the roof from leaking.

Logic Check: If your total savings are $1,000,000, you only have $483 a month left over for food, gas, healthcare, and hobbies. In 2026, that doesn’t even cover a single steak dinner or a trip to see the grandkids. If your house is eating 85% of your safe withdrawal, you aren’t an owner—you’re a tenant of your own property.

Technical Deep Dive: The Structural Engineering of Maintenance

As a guy who has flipped 100 properties, I can tell you that deferred maintenance is a debt that always collects with interest. In 2026, supply chain issues for specialized building materials—like impact-resistant windows or high-SEER heat pumps—remain tight.

If you live in a house built in the early 2000s, your polybutylene piping or original roof is a ticking time bomb. From a first-principles logic perspective, spending $1,500 on a smart leak detector today is an ROI-positive move. It prevents a $30,000 mold remediation later. If you are on a fixed 4% draw, you cannot afford the luxury of “hoping” things don’t break. You must be proactive or you will be forced to sell your property at a distressed price.

| 2026 Affiliate Product Comparison | Item 1: Moen Flo Smart Leak Detector | Item 2: Honeywell Home T9 Smart Tstat | Item 3: MERV 13 High-Efficiency Filters |

| Why You Need It | Prevents $20k water damage. | Cuts 2026 utility spikes. | Protects HVAC longevity. |

| Retirement Benefit | Potential Insurance Discount. | Automated Comfort. | Lower Repair Bills. |

| Price Point | ~$400 (plus install) | ~$180 | ~$25/ea |

The Key Question — How Much of Your Income Should Go to Housing?

Conservative Guideline

I recommend keeping housing under 30% of your total retirement income. If you have a pension and Social Security, add those to your 4% draw before doing the math. Being conservative isn’t boring; it’s how you stay in control.

Why Seniors Should Be More Conservative Than Working Adults

When you’re 40, a $10,000 repair is a setback. When you’re 70, it’s a crisis because you have no “human capital” left. You aren’t going back to the office to earn an extra $10k. Inflation also hits seniors harder because your “fixed” income buys less every year, but your house’s demand for paint and shingles never shrinks.

The Danger Zone

If 40% or more of your income is going to housing, you are in the “Danger Zone.” One spike in property taxes or a medical co-pay could force you to sell your home in a down market. That is the quickest way to go broke.

Technical Deep Dive: IRC Section 121 and the 2026 Downsize

If you are considering downsizing to align with the 4% Rule, you need to understand IRC Section 121. In 2026, the exclusion remains $250,000 for singles and $500,000 for married couples filing jointly. This is the ultimate “get out of jail free” card for your home’s appreciation. If you bought your home for $200k and it’s now worth $800k, you have a $600k gain. As a couple, $500k is tax-free. The remaining $100k will be hit with capital gains taxes (likely 15% or 20% in 2026).

However, if you “stay put” until death, your heirs get a step-up in basis to the fair market value. Logic check: Is it worth living “house poor” for 20 years just so your kids pay less tax later? No. Sell the house, take the $500k tax-free, and move into something that fits the 4% Rule.

Real-Life Scenarios: Side-by-Side 2026 Comparisons

To see how the 4% Rule actually plays out, we have to look at the Housing Ratio. This is the percentage of your total monthly income (Draw + Social Security) that vanishes into your home. In 2026, if this number is over 30%, you are effectively “shorting” your own retirement.

| Retirement Scenario | Monthly Income (4% Draw + SS) | Total Monthly Housing Cost | Housing Ratio (%) | Financial Health Status |

| Scenario 1: Paid-Off Home | $4,500 | $900 | 20% | Winning: High flexibility for travel/healthcare. |

| Scenario 2: Moderate Mortgage | $4,500 | $1,800 | 40% | Danger Zone: One major repair away from debt. |

| Scenario 3: High Housing Cost | $4,500 | $2,700 | 60% | Disaster: Living for the house, not the human. |

Scenario 1 — The Strategic Winner

With a Housing Ratio of 20%, this person is in the “Sweet Spot.” Because they don’t have a mortgage, their 4% draw is protected. Even if property taxes spike in 2026, they have the margin to absorb the hit without cutting back on the “good” wine or the grandkids’ birthday gifts.

Scenario 2 — The “House Poor” Retiree

This person is in a fragile state. At a 40% Housing Ratio, nearly half of every dollar is gone before they buy a single bag of groceries. They are “house poor.” If the market takes a 10% dip in 2026, they will be forced to raid their principal just to keep the bank from calling. They should consider downsizing after 60 immediately.

Scenario 3 — The Structural Deficit

A 60% Housing Ratio is a financial suicide mission. This person is essentially “spending” their legacy and their future medical fund to live in a house they can no longer afford. From a first-principles logic perspective, there is no “emotional value” high enough to justify this level of risk.

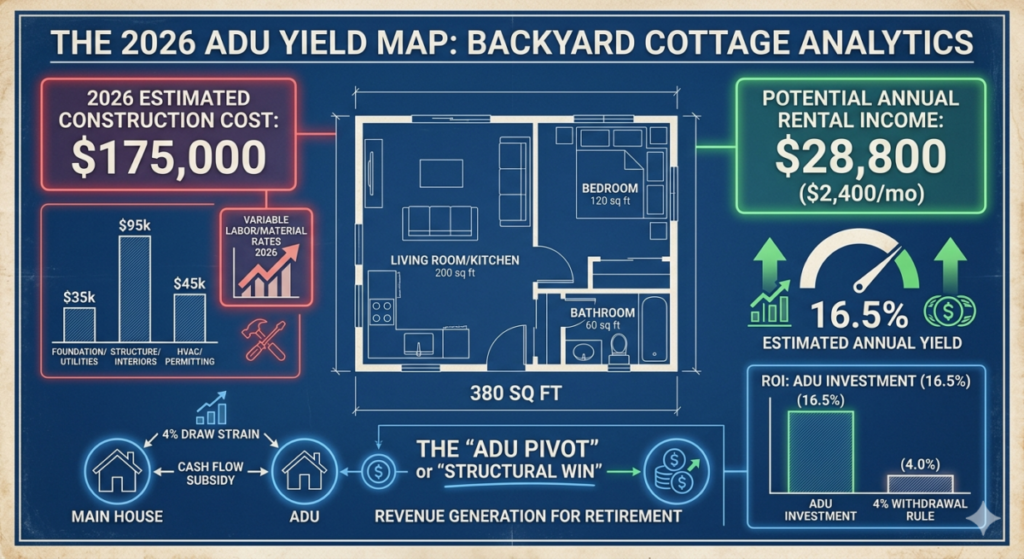

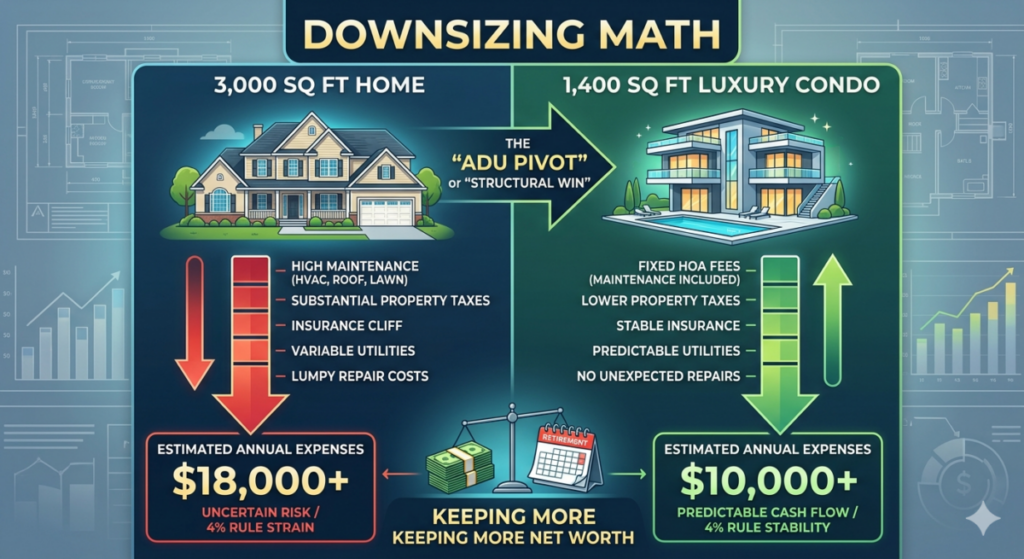

Technical Deep Dive: 2026 Zoning and the “ADU Pivot”

One way to fix your housing ratio without the trauma of moving is the “ADU Pivot.” In 2026, many states have relaxed zoning laws to allow Accessory Dwelling Units (granny flats) by right. If your home is eating too much of your 4% draw, you can turn your backyard into a revenue stream.

- Structural Logic: Spending $150,000 to build an ADU might seem crazy when you’re retired. However, if you have the cash sitting in a low-yield account, it’s a dead asset.

- The Math: If that unit rents for $2,000 a month ($24,000/year), your $150k investment is yielding 16% annually. That crushes the 4% Rule and subsidizes your own housing cost, making your retirement much safer.

- ROI Logic: This increases the total property value and creates a multi-generational living option. If you can’t afford your home on the 4% Rule, making the home generate its own income is the only logical move besides selling.

| 2026 ADU Cost Transparency Table | Low-End (Small Junior ADU) | High-End (Full Detached Unit) |

| Permitting Fees | $2,500 (Streamlined) | $12,000 (Coastal/Strict) |

| Construction (Per Sq Ft) | $175 (Conversion) | $350 (New Build) |

| Plumbing/Electrical | $8,000 (Main Tie-in) | $25,000 (New Service Lines) |

| Estimated Rent Yield | 8–10% | 12–18% |

How Social Security Changes the Equation

Why It Reduces Risk

Social Security is an inflation-adjusted annuity. It’s the floor of your birdhouse. While the 4% Rule depends on the “mood” of the stock market, Social Security depends on the US Government’s ability to print money. I’ll bet on the latter every time.

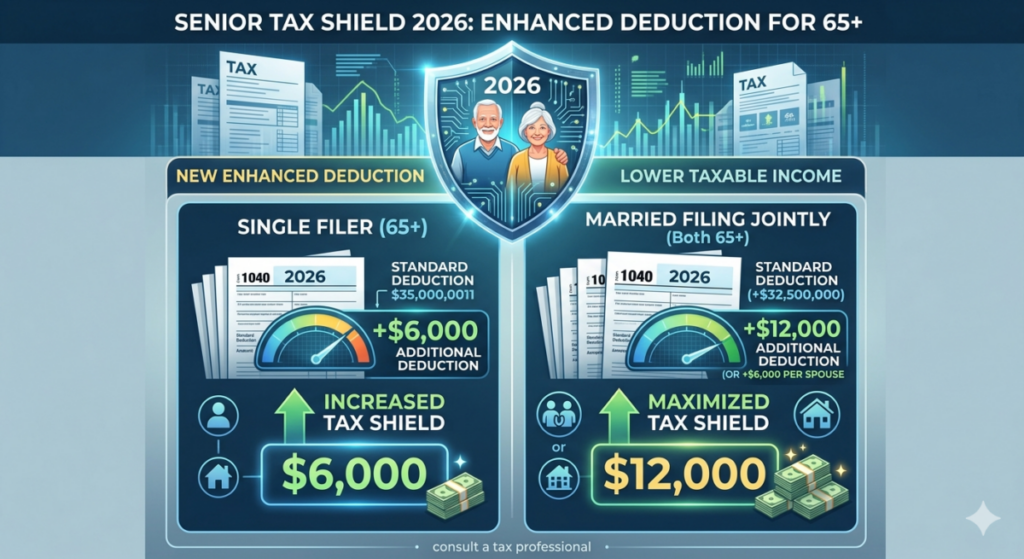

The 2026 “OBBBA” Impact

The One Big Beautiful Bill Act of 2025/2026 introduced an Enhanced Deduction for Seniors. * Single: $23,750 total deduction. * Married: $47,500 total deduction. This means most of your Social Security income in 2026 is effectively tax-free. This “tax alpha” gives you slightly more breathing room in your housing budget than you had in 2024. Use it to pay down debt, not to buy a more expensive house.

Technical Deep Dive: 2026 Step-Up in Basis Rules

Let’s talk about the “Dead Hand” strategy. In 2026, the Step-Up in Basis remains one of the most powerful wealth-transfer tools in the Internal Revenue Code. When you pass away, the “basis” of your home—the price used to calculate taxes—resets to the current fair market value. If you bought for $100k and it’s worth $1M when you die, your kids can sell it for $1M and pay $0 in capital gains.

The Opportunity Cost: If you stay in a $1M home that costs you $4,000 a month just to “save” your kids from taxes, but you run out of cash and have to eat Ramen, you have made a logical error.

The Alternative: Sell now, move to a $400k condo, and put the $600k surplus into a brokerage account. Even with the taxes paid now, your quality of life in the next 20 years increases exponentially.

Practical Step-by-Step: Can You Afford This Home?

Follow these steps to “Stress Test” your 2026 life:

- Step 1: Calculate Your Withdrawal: Multiply your total liquid savings by 0.04 (or 3.9% if you want to be extra safe in 2026). This is your safe annual draw.

- Step 2: Add Guaranteed Income: Add your annual Social Security and any pensions to the number from Step 1. This is your “Gross Retirement Income.”

- Step 3: Deduct Non-Housing Essentials: Subtract $15,000 to $20,000 for “Life Happens” (Healthcare, basic food, basic transport). What is left is your housing ceiling.

- Step 4: Audit Your Real Home Costs: Total up your annual PITI (Principal, Interest, Taxes, Insurance) plus a 1.5% maintenance reserve based on your home’s value.

- Step 5: The Final Comparison: If Step 4 is greater than 30% of Step 2, you are in a “Structural Deficit.” You are consuming your wealth faster than it can grow.

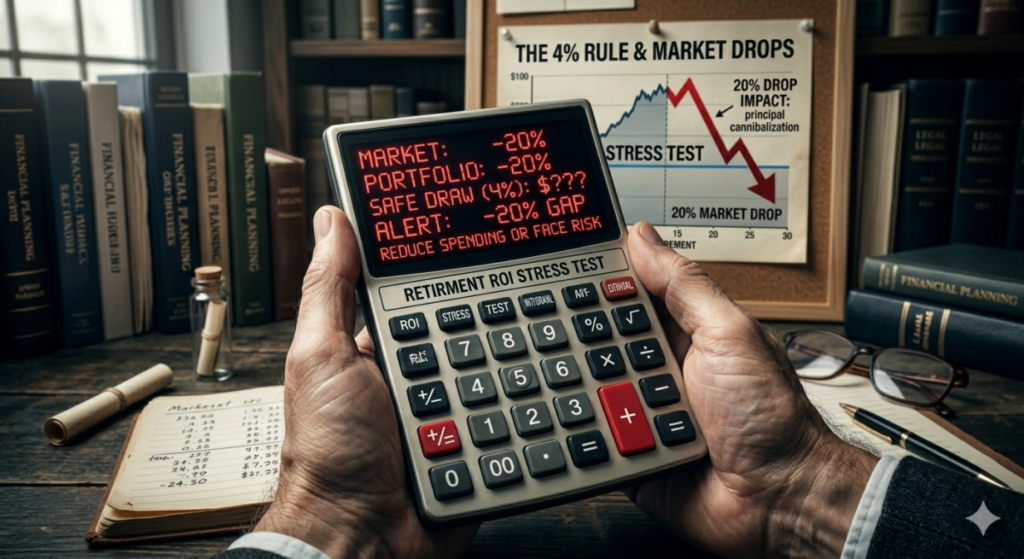

Stress Test Scenarios

What happens if the 2026 market drops 20%? Your $1M becomes $800k. Your 4% draw is now only $32,000. If your housing cost is fixed at $25,000, you are now spending 78% of your draw on housing. This is why you need a bridge loan strategy or a significant cash reserve (2 years of expenses) to avoid selling stocks at the bottom.

Downsizing vs. Staying Put

When Downsizing Makes Sense

If your housing costs exceed 30% of income, you are living for the house, not yourself. A large, underused home is just a collection of empty boxes that you have to heat, cool, and insure.

When Staying Makes Sense

If your home is paid off, your property taxes are locked in (like in California with Prop 13), and your insurance is manageable, staying put is a mathematical win. It keeps your 4% draw dedicated to your lifestyle, not your roof.

Middle Ground Options

Consider moving to a lower-cost area. Moving from New Jersey (2.23% tax) to Alabama (0.41% tax) can save you $8,000 a year in taxes alone. That’s an extra $666 a month in your pocket without taking a penny more from your savings.

Technical Deep Dive: 2026 Smart Home ROI for Seniors

From a first-principles logic perspective, you shouldn’t buy technology for “fun”; you buy it to lower your carry costs. In 2026, homeowners insurance providers are offering significant discounts for homes with active leak detection and monitored security. If your 4% withdrawal strategy is tight, these tools act as a shield against the “lumpy” expenses that ruin a retirement budget.

| 2026 Affiliate Product Comparison | Item 1: Ring Alarm 8-Piece Kit | Item 2: Rachio 3 Smart Sprinkler | Item 3: Govee Smart Water Sensors |

| Why You Need It | Home Security / Lower Insurance. | Cuts Water Bills by up to 50%. | Detects small leaks before they flood. |

| Retirement Benefit | Peace of Mind and theft protection. | Automated Savings on utilities. | Avoids High Deductibles($5k+). |

| Price Point | ~$200 | ~$150 | ~$50 for a 3-pack |

Why These Specific Tools?

- Ring Alarm: In 2026, many insurance carriers require monitored security to keep your “Preferred” rate status. It’s a small investment to prevent a massive premium hike.

- Rachio 3: With water scarcity taxes rising in 2026 (especially in the Sunbelt), an intelligent controller pays for itself in less than two seasons.

- Govee Sensors: Water damage is the #1 reason for insurance claims among seniors. These sensors are your early warning system against a $20,000 mold remediation nightmare.

Rent vs. Own in Retirement (Through the 4% Lens)

Renting

In 2026, renting is becoming more attractive for seniors who want to “cap” their risk. When the water heater explodes, you don’t use your 4% draw; the landlord uses theirs.

Owning

Ownership is a hedge against rent inflation, but it exposes you to tax and insurance inflation. In a high-inflation environment like 2026, your “fixed” mortgage stays the same, but your insurance might double.

Which Fits Better?

Ownership is better if you have a low-interest rate mortgage (3-4%) or a paid-off home. If you are “buying fresh” in 2026 at 7% interest rates, renting might actually preserve more of your net worth over a 10-year period.

Simple Rules of Thumb (Quick Reference)

* Keep housing under 25%–30% of total retirement income.

* Always calculate total monthly cost (not just mortgage).

* Maintain a cash reserve for repairs (don’t raid the 4% draw).

* If unsure, err on the conservative side. Your 90-year-old self will thank you.

Actionable Checklist: Can I Afford This Home in Retirement?

- Verify Income: Is my PITI + Maintenance less than 30% of my total income?

- Liquidity Check: Do I have a 2-year cash “bucket” to avoid selling stocks during a market dip?

- Insurance Audit: Have I calculated the 2026 insurance premium hike (avg 10-16%)?

- Physical Reality: Is the house “senior-ready” (no stairs, wide doors) or will I need a $50k remodel?

- Tax Optimization: Have I used my 2026 Enhanced Senior Deduction to its full potential?

Internal Resources

* Downsizing After 60: A Financial First-Principles Approach

* The Total Cost of Ownership for a Condo in 2026

* Bridge Loan Strategies for Senior Transitions

Summary

Retirement success isn’t about having the biggest house on the block; it’s about having the most freedom in your 80s. The 4% Rule is a guideline, but your house is a shark that never stops eating. In 2026, you must be the gatekeeper of your own cash flow. If the math doesn’t work, don’t try to “feel” your way through it. Sell, downsize, or rent. Your future self will thank you when they aren’t working a greeting job at a big-box store just to pay the property taxes.

Bio: Charles O’Dell

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement. He doesn’t care about your curb appeal; he cares about your 10-year net-worth trajectory.

Written by Charles O’Dell: 23+ years experience, 100+ flips, and former American Express financial planner.