Summary: “Independent Living”? In 2026, most Long-Term Care Insurance (LTCI) policies remain strictly “care-based,” meaning they do not pay for the lifestyle costs of independent living. Unless you fail at least two Activities of Daily Living (ADLs) or have a severe cognitive impairment, your policy is a paperweight for housing costs. Independent living is legally classified as “housing,” not “custodial care.” Relying on insurance to pay your rent in a 55+ community is a fast track to a drained bank account.

Note: Local labor rates for independent living and home health care change constantly. See our full regional cost table below.

Introduction

I have spent over 23 years watching people make the same expensive mistake. They buy a Long-Term Care Insurance (LTCI) policy, pay premiums for decades, and then get hit with a “denial of claim” the moment they try to move into a fancy independent living apartment. Why? Because they fell for the marketing fluff instead of reading the math. I am Charles O’Dell, and I do not care about your “dream retirement” if it leads to bankruptcy. I care about your bottom line.

The allure of Independent Living communities often masks a critical oversight in the Long-Term Care Insurance landscape. Many policyholders, seduced by appealing amenities, find themselves unprepared for the harsh realities of claim denials when seeking coverage for these lifestyle choices. This guide aims to illuminate the financial intricacies and limitations inherent in LTCI policies, ensuring that you understand the true nature of your coverage before making potentially costly decisions. By fostering transparency, we seek to empower you to prioritize your financial security and avoid the pitfalls of inadequate insurance protection.

Video Guide Overview (Independent Living & LTC Policy)

Affiliate Disclosure

I am a straight shooter. Some of the links in this article are affiliate links. This means if you click them and buy something: I might get a small commission. It does not cost you a penny extra: and I only recommend tools that actually help you track your net worth or protect your assets. I use the proceeds to keep the lights on here at HousingAfter60.com so I can keep giving you the cold, hard truth.

The “Short” Answer

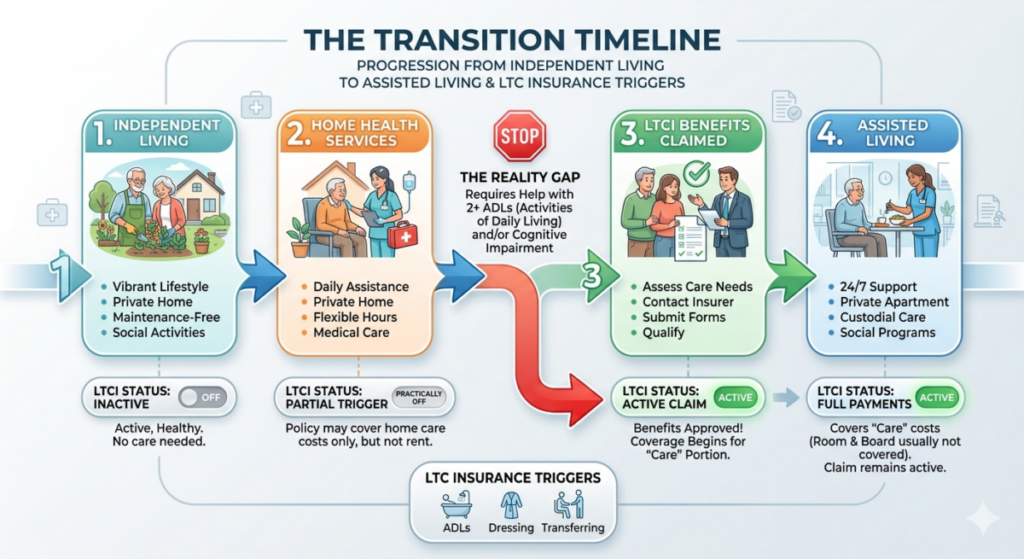

The short answer is a resounding NO. Your LTCI policy will not pay for independent living in 2026. Here is the logic: Independent living is real estate. LTCI is a health product. Unless you meet the “Benefit Triggers”: usually needing help with two out of six Activities of Daily Living (ADLs) like bathing or eating: the insurance company owes you nothing. You are paying for the roof: they only pay for the person helping you get out of bed under that roof. If you move into independent living today, you are 100% on the hook for the rent, the entry fee, and the meal plan.

Technical Deep Dive: IRC Section 213 and the Tax Trap of 2026

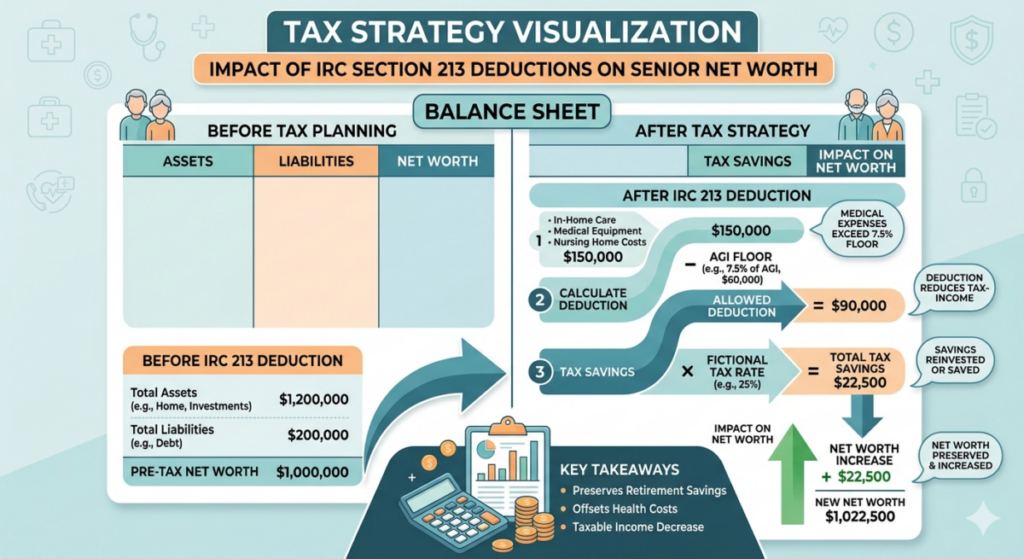

As a former CPA, I look at every housing move through the lens of the Internal Revenue Code. For 2026: many seniors assume that the full cost of an independent living “buy-in” or monthly fee is a deductible medical expense. This is a dangerous assumption. Under IRC Section 213: you can only deduct expenses for “medical care.” This creates a massive logic gap for those in independent living. Unlike assisted living or memory care: where a significant portion of the monthly fee can be justified as medical: independent living is almost entirely “room and board.”

The IRS is notoriously pedantic about this. If you are paying $8,000 a month for a luxury apartment in a senior community: and that community provides zero medical supervision: your deduction is $0. However: if you have a “Life Care” contract (Type A), a portion of your entry fee may be deductible as a prepaid medical expense. The math is brutal: typically only 20% to 40% of the fee qualifies. If you try to deduct the whole thing: the IRS will come for you like a heat-seeking missile. You must obtain a “disclosure statement” from the facility that breaks down the percentage of their operating budget spent on medical care. Without this: your deduction is just a guess; and the IRS does not like guesses.

Furthermore: in 2026, the standard deduction remains high. Unless your medical expenses (including the care portion of your housing) exceed 7.5% of your Adjusted Gross Income (AGI): you get zero tax benefit. For a senior with a high net worth: you might need to spend $60,000+ out of pocket before a single dollar becomes deductible. This is why I always tell my clients: “Do not move for the tax break; move for the logic of the asset transition.” If you are relying on a tax refund to make the monthly rent work: you are already in financial trouble.

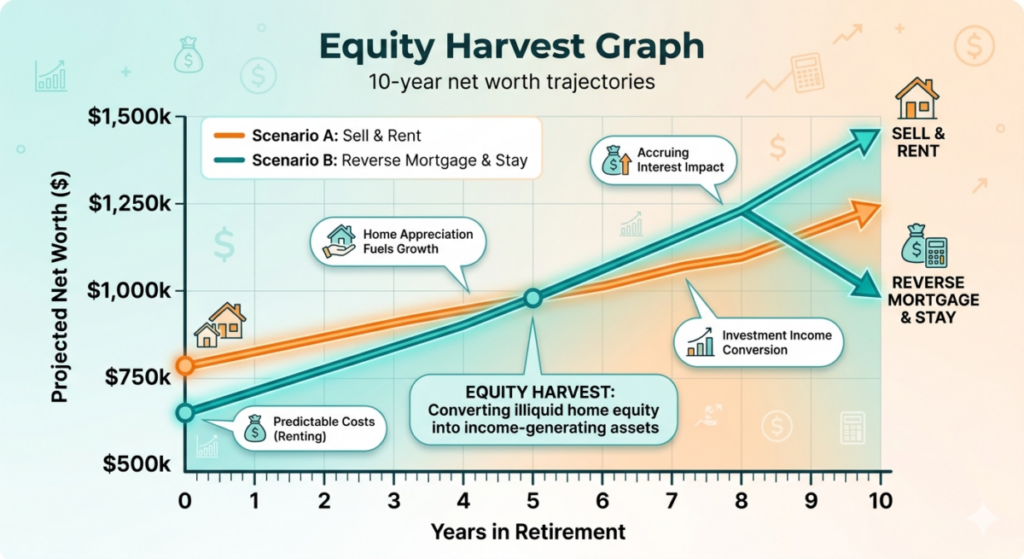

Consider the opportunity cost: in 2026, many seniors are choosing to stay in their homes to maintain the Step-Up in Basis for their heirs. If you sell a highly appreciated asset (your home) to move into a non-deductible rental, you are effectively liquidating a tax-advantaged asset to fund a tax-disadvantaged lifestyle. From a first-principles perspective, you should only liquidate the home if the carry cost (maintenance, taxes, insurance) exceeds the rent of the independent living facility after accounting for the lost investment yield of the home equity. If your home is worth $1.2 million and appreciating at 4%, that’s $48,000 in “hidden” earnings you lose by selling to pay rent.

We see this frequently with homeowners in California or Florida where homestead exemptions provide a massive tax shield. Moving to independent living strips that shield away. I advise clients to run a 10-year net-worth projection: comparing the compounded value of the home plus the LTCI premiums saved vs. the drained principal of a rental move. Often, the “Independent Living” path results in a 30% lower net worth by year ten. That’s a failing grade in my book.

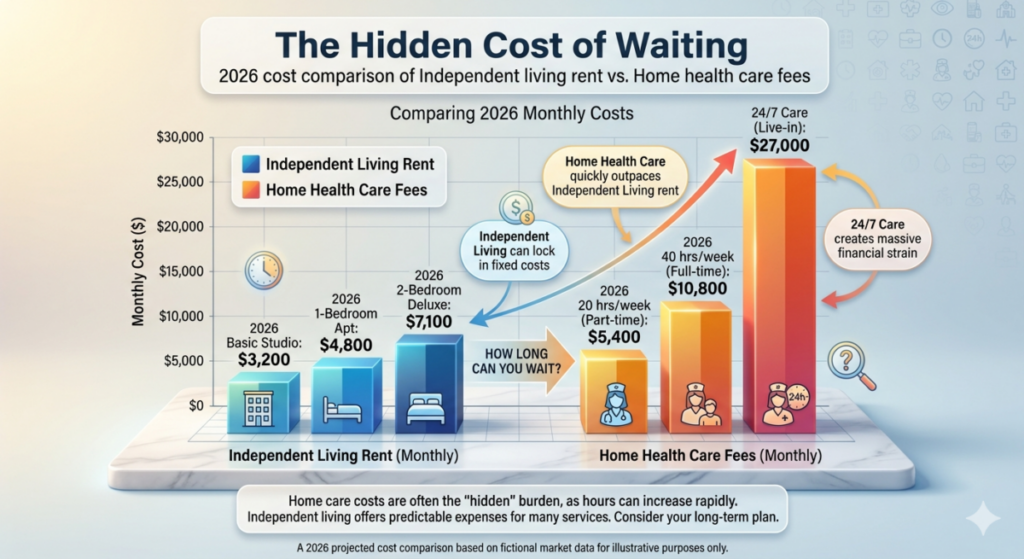

| 2026 Cost Transparency Table | Low-End (DIY/Rural) | High-End (Pro/Urban) |

|---|---|---|

| Independent Living Rent (Monthly) | $3,200 | $8,500 |

| In-Home Care (20 hrs/week) | $2,800 | $5,200 |

| Tech/Safety Monitoring Fees | $150 | $700 |

| **Total Out-of-Pocket** | **$6,150** | **$14,400** |

| Recommended 2026 Wealth Tools | Best For | Price |

|---|---|---|

| AssetLock Portfolio Monitor | Tracking LTCI Value | $19/mo |

| Lively Mobile2 Alert | Independent Safety | $49.99 |

| HomeZon Digital Audit | Zoning & Licensing Checks | $129 |

What Is Independent Living?

Independent living is essentially “downsizing with a social calendar.” It is designed for seniors who can handle their own business: manage their own meds: and drive their own cars. You are buying convenience. You are buying someone else to shovel the snow and fix the leaky sink. You are not buying healthcare. In 2026: these communities are often marketed as “Resort Living”: but do not let the palm trees fool you. From a legal and financial standpoint: you are just a tenant in an apartment building that happens to have an age requirement.

I have flipped over 100 properties, and I can tell you that the market value of an independent living unit is driven by demand, not by the quality of care. If the community is in a high-growth ZIP code, you will pay a real estate premium. This premium is not reimbursable by your LTCI provider. They view your move to a luxury independent living tower in downtown Nashville the same way they view a move to a beach house: it’s a luxury consumption, not a medical necessity.

Technical Deep Dive: Zoning and Facility Licensing Hurdles

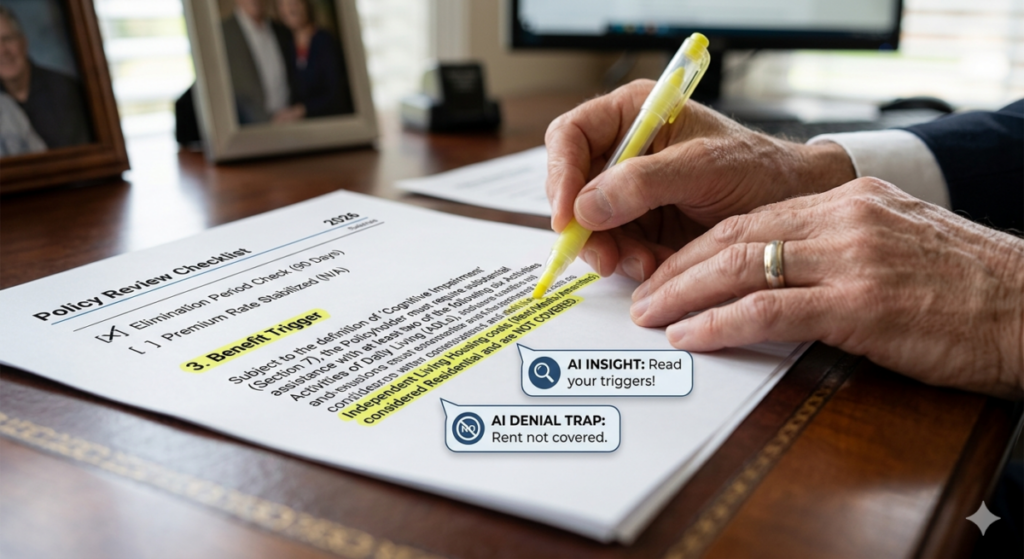

Why won’t they pay? It comes down to legal definitions. In the eyes of the law: and the 2026 insurance policy language: a facility must be “licensed” to provide custodial care for benefits to kick in. Most independent living communities are zoned as R-2 (Residential Multi-Family) or similar residential classifications. They are essentially apartments with a clubhouse. They are not “Health Care Facilities.”

If your policy says it covers “Care in a licensed facility”: and you move into an R-2 zoned apartment: the insurance company’s legal team will laugh your claim out of the room. I have seen homeowners try to sue: claiming that because the facility has a “wellness center”: it should count. They lose every time. The “wellness center” is a marketing gimmick: not a clinical license. For a facility to qualify for LTCI payments: it must meet state-specific staffing ratios for nurses and certified nursing assistants (CNAs). Independent living communities do not have these ratios because their residents are, by definition, independent.

In 2026, many states like California and New York have introduced Enhanced Residential Care licenses. However, a facility holding this license still must provide assistance with ADLs to you specifically for a claim to be valid. You can’t just live in a building that offers care; you must be receiving care. If you are 75 and fit enough to play 18 holes of golf, the Actuarial Risk department at your insurance company has already flagged your file for a denial if you submit a claim for housing.

Furthermore, the “Plan of Care” requirement is a massive hurdle. In 2026, insurance companies require a Licensed Health Care Practitioner (a doctor or registered nurse) to certify that you are chronically ill and will remain so for at least 90 days. Most independent living residents don’t qualify because their functional capacity is too high. If you can self-administer medication, you aren’t “chronically ill” enough for the insurance company to start cutting checks. This is the brutal reality: you have to be sick to get the money, but you moved to independent living because you were healthy. That’s a logical paradox that ends with you paying the full bill.

Why LTC Insurance Usually Does NOT Cover Independent Living

The core reason is simple: Actuarial Risk. If insurance companies paid for independent living: every 65-year-old in America would sign up and move into a resort on the company’s dime. The system would collapse in forty-eight hours. The insurance company only wins when you stay healthy: and they only pay when you are significantly “broken.” To trigger the benefits: you must meet the “ADL” threshold.

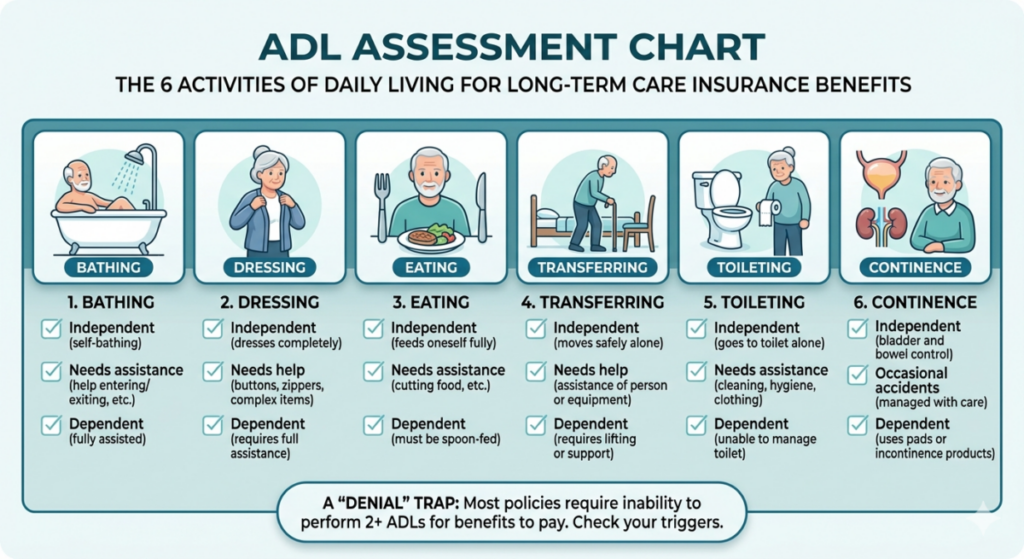

The 2026 ADL Threshold List: The “Gatekeepers” of Your Payout

To trigger a payout from a Long-Term Care Insurance (LTCI) policy in 2026, you generally must require “substantial assistance” with at least two of the following six Activities of Daily Living (ADLs). In the eyes of an insurance adjuster, “difficulty” is not enough; you must be physically or cognitively incapable of performing these tasks safely.

- Bathing: The ability to wash yourself in a tub, shower, or by sponge bath. This includes the physical task of getting into or out of the tub or shower. If you can bathe yourself but just need a grab bar, you are still independent.

- Dressing: Putting on and taking off all items of clothing and any necessary braces, fasteners, or artificial limbs. If you can dress yourself but just struggle with 2026-style “smart apparel” or tight shoes, you are still independent.

- Transferring: The ability to move in and out of a bed, chair, or wheelchair. This is a “high-stakes” trigger. If you can stand up from a recliner using your own strength or a walker, the insurance company stays silent.

- Toileting: Getting to and from the toilet, getting on and off the toilet, and performing associated personal hygiene.

- Continence: The ability to maintain control of bowel and bladder function; or, when unable to maintain control, the ability to perform associated personal hygiene (including caring for a catheter or colostomy bag).

- Eating: Feeding oneself by getting food into the body from a table, plate, or cup, or by a feeding tube or intravenously. Note: This does not include preparing the meal (cooking). If you can’t cook but can still move a fork to your mouth, you fail the trigger.

The “Cognitive Impairment” Exception: In 2026, you may also trigger benefits if you require “substantial supervision” due to a severe cognitive impairment (such as Alzheimer’s or Dementia) that threatens your health or safety. However, being “forgetful” is not a claim trigger. You must show a loss of 10-year short-term memory or disorientation as to person, place, or time.

If you can do these things: you are independent. Therefore: your housing is a personal choice: not a medical necessity. The insurance company treats your rent the same way they treat your Tesla payment: it is your problem: not theirs. In 2026, the “Benefit Trigger” is the most litigated part of these policies because seniors believe they are “paying for their future,” but they haven’t defined what that future looks like clinically.

I have seen families spend $15,000 on legal fees trying to fight a “transferring” denial. The insurance company sent an undercover nurse to watch the claimant walk to the dining hall. If you can walk to dinner, you can “transfer.” Claim denied. This is the bottom-line reality of the insurance business. They are not in the business of lifestyle support; they are in the business of risk mitigation. If you aren’t a high-risk patient, you aren’t getting a payout.

Technical Deep Dive: ROI and 10-Year Opportunity Cost Scenarios

Let’s talk about your net worth. Most people see their home as a “nest egg.” I see it as a non-performing asset if you are over 60 and it is draining $3,000 a month in taxes, insurance, and maintenance. If you move to independent living: you are swapping one housing expense for another. The real question is: “What is the opportunity cost of using your own cash vs. trying to force an LTCI claim?”

Consider a 10-year trajectory. In 2026: if you stay in your $850,000 home: you are likely losing 3% to 4% of that value annually to “friction costs” (maintenance, taxes, etc.). If you sell and move to independent living: you unlock $850,000. If you invest that at a conservative 5% yield in 2026: you have $42,500 a year in new income. This “income” covers your independent living rent without you ever needing to touch your LTCI policy. By the time you actually *need* the insurance (maybe at age 82): your original $850,000 is still intact: and your LTCI kicks in to cover the $14,000 monthly nursing fee. People who try to “save” their money by waiting for the insurance to pay for housing usually end up with a house that has a leaking roof and zero liquidity. That is bad math.

We also need to look at the Inflation Guard. Most LTCI policies have a 3% or 5% compound inflation rider. If you start your claim too early—by forcing a move to independent living—you might exhaust your lifetime maximum benefit before you actually hit the high-cost years of a nursing home. In 2026, a private nursing room can easily exceed $18,000 a month in urban centers. If you burn your $300,000 benefit pool on $4,000 monthly rent subsidies at age 70, you will be penniless at 85 when you need real care. From a wealth preservation standpoint, you should self-fund the “lifestyle years” and save the insurance ammunition for the “medical years.” This is how the 1% stay the 1%. They arbitrage the risk instead of consuming the capital.

Furthermore, consider the Internal Rate of Return (IRR) on your premiums. If you have paid $100,000 in premiums over 20 years, your breakeven point on an LTCI claim is usually about 18 to 24 months of full nursing home care. If you use it for independent living, where the payout is significantly lower (or zero), your IRR drops into the negatives. You are better off investing the premiums in a diversified REIT or high-yield bond fund. I tell my HousingAfter60 readers: “Don’t bet on being sick; bet on being smart.”

When LTC Insurance MIGHT Pay in an Independent Living Setting

There is a narrow loophole: and I mean narrow. If you are living in an independent living unit and your health takes a dive: but you refuse to move to the assisted living wing: you can sometimes “bring the care to you.” This is essentially “Aging in Place” within a facility. Most modern policies will cover “Home Health Care” services even if your “home” is a rented apartment in a senior community.

But beware: they only pay for the caregiver’s hourly rate. They will still not pay your rent. In 2026: the average cost of an HHA (Home Health Aide) is $38/hour. If you need 8 hours of help a day: that’s $9,120 a month. Your insurance might cover $7,000 of that (if that’s your policy limit): but you still have to pay the $6,000 rent for the apartment. You are now spending $15,120 a month. At that point: logic dictates you should move to Assisted Living where the room, board, and care are bundled: often triggering a higher reimbursement from your policy. Don’t let a slick salesperson tell you that “insurance covers us”: they are only half-right: and being half-right in finance is the same as being wrong.

Technical Deep Dive: Structural Engineering and Universal Design Costs

If you decide to “Age in Place” in your own home because the LTCI won’t pay for independent living: you need to understand the capital expenditure (CapEx) involved. To make a standard home safe for a 2-ADL impairment: you are looking at significant structural changes. In 2026: a “Wet Room” bathroom conversion costs between $22,000 and $40,000. Widening three interior doors to accommodate a wheelchair? That’s $5,500. A ramp that meets ADA slope requirements? $3,500.

Insurance does not pay for these renovations. This is another “Lifestyle Cost” that seniors often overlook. When you move to independent living: these features are already built-in. This is where the “Independent Living” math actually starts to make sense. You are pre-paying for universal design. From a first-principles perspective: you are trading a one-time capital hit (home renovation) for a recurring operational expense (rent). If you plan to live in that independent living unit for more than 4 years: the “rent premium” often exceeds the cost of the home renovation. However: if you sell a house with a $600k gain: the liquidity gives you the freedom to choose. In the house: you are stuck with your renovations. In the apartment: you can leave if the neighbors get annoying. In real estate: flexibility is a form of currency.

I also look at maintenance reserves. A homeowner over 60 should have a “CapEx Reserve” of at least 1% of the home value annually. For a $1,000,000 home, that is $10,000 a year just to keep the roof from caving in. In independent living, your reserve is $0. When you factor in the “Time-Adjusted Cost of Ownership,” the rent in a senior community often looks better than a free and clear home. But remember: you are still the one writing the check, not Manulife or Genworth. They don’t care if your HVAC dies; they only care if you die or get sick. Always keep your real estate logic separate from your insurance logic.

Technical Deep Dive: 2026 Step-Up in Basis and Estate Logic

If you are holding onto your home just to avoid “wasting” money on independent living: you need to understand the 2026 Step-Up in Basis rules. Many people think they should keep the house until they die so their kids get the tax break. But if you move into independent living and need to sell the house to fund your care because your LTCI isn’t kicking in yet: you might face massive capital gains taxes. In 2026: the exclusion is still $250k for singles and $500k for couples. If your home has appreciated more than that: selling it while you are alive to move into independent living might trigger a tax bill that wipes out three years of rent.

You need to coordinate your LTCI strategy with your real estate exit strategy. Sometimes: it is better to use a reverse mortgage to pay for the “independent” years and keep the asset in the family: rather than selling in a panic when the insurance company says “No.” A reverse mortgage allows you to tap the equity without a monthly payment: providing the “rent” for your independent living move. But be careful: if you move out of the house for more than 12 consecutive months: the reverse mortgage becomes due and payable. You cannot keep the house and live in independent living indefinitely using a reverse mortgage. This is a common trap. The logic is simple: the bank wants their money back when you leave. If you are moving to independent living: that is your permanent move. You have one year to sell the house or pay off the loan. In 2026: with interest rates stabilized but higher than the 2010s: the interest “burn” on a reverse mortgage can be 7% or higher. That is a very expensive way to fund a lifestyle choice. If you can’t afford independent living without a complex debt instrument: you can’t afford independent living.

There is also the “Medicaid Five-Year Look-Back” to consider. In 2026, the surrender of home equity to pay for independent living can be seen as a disqualification for future Medicaid if it’s not handled as a “Fair Market Value” transaction. If you “sell” your house to your kids for $1 so you can move into independent living and preserve the Step-Up in Basis, you have just destroyed your eligibility for state-funded nursing care. You must be ruthless with the math. If you are 60+, every six-figure transaction must be vetted by an elder law attorney and a real estate professional who knows the Senior Housing landscape. I’ve seen $100+ flips where the biggest profit was in the tax avoidance, not the sale price. Apply that same investor mindset to your own home.

Actionable Checklist

The 2026 Independent Living “Anti-Trap” Checklist

Before you sign a lease or sell your home, run through this checklist to see if you are actually covered. If you check “No” on more than two of these, you are self-funding this move.

- [ ] Policy Verification: Do you have a copy of your “Outline of Coverage”? Look for the definition of a “Qualified Long-Term Care Facility.” If the policy says it only pays for “Skilled Nursing,” it will never pay for an apartment.

- [ ] Licensing Audit: Call the facility’s admissions office. Ask for their License Category. In 2026, most LTCI policies require the facility to be licensed as an “Assisted Living Facility” or “Residential Care Facility” to trigger room and board payments. If they are licensed as “Congregate Housing” or “Active Adult,” the claim is a non-starter.

- [ ] The “Wait-Out” Math: Identify your Elimination Period. Is it 90 Calendar days or 90 Service days?

- Calendar Day: Payout starts 90 days after you qualify.

- Service Day: Payout starts only after you have paid for 90 days of actual care. If you only get care 3 days a week, it could take 30 weeks before the insurance pays a dime.

- [ ] Physician Alignment: Does your primary doctor agree that you require “Hands-on Assistance” with at least two ADLs? If your doctor’s notes say you are “doing great and staying active,” the insurance company will use that as evidence to deny your claim.

- [ ] The “Home Care” Loophole Check: If the facility is unlicensed but you need care, does your policy have a “Home Care” rider? This may allow you to hire an outside agency to provide care inside your independent living apartment. You still pay the rent, but the insurance covers the $35+/hour caregiver cost.

- [ ] Elimination Period Liquidity: Do you have at least $40,000 in liquid cash? Between the 90-day waiting period and the initial “community fee” (often equal to one month’s rent), the first 120 days of independent living are the most expensive.

- [ ] Inflation Shield Review: Compare your daily benefit (e.g., $200/day) to the 2026 local rate. If there is a $100/day gap, that is a $36,500 annual deficit you must fund from your own pocket.

Internal Resources

To further protect your net worth: check out these other guides we have prepared for the 2026 market:

- 2026 Retirement Housing Costs: Is Your Monthly Payment Breaking the 4% Rule? (Labor vs. DIY Tables)

- The $2,500 Senior Safety Home Upgrades That Save $78,000 in Nursing Home Fees (2026 Guide)

- 2026 Reverse Mortgage vs. Downsizing: The 10-Year Equity Drain Math They Don’t Show You

Summary

The math is cold and the reality is blunt: Long-term care insurance is a medical safety net: not a housing subsidy. If you are moving to independent living for the social life: the amenities: or the lack of yard work: you are paying for it yourself. In my 23+ years of experience: I have seen too many seniors “wait for the insurance” until they are too frail to actually enjoy the transition. Use logic. Sell the house when it makes sense: invest the proceeds: and keep the LTCI in your back pocket for the day you actually need a nurse. Retirement is a business decision: treat it like one. If you can’t see the profit in the move: don’t make the move.

Bio: Charles O’Dell

Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. Now, with 23+ years of experience and over 100 successful property flips, Charles is a leading expert in senior housing transitions. He specializes in stripping away the marketing “fluff” to help homeowners find sustainable, logical real estate solutions that protect their net worth in retirement. Charles doesn’t care about the color of the granite countertops; he cares about the 10-year internal rate of return on your housing choices. He believes that every senior deserves a strategy built on first-principles: not feelings.

Written by Charles O’Dell, a former CPA and real estate investor with 100+ flips and 23+ years of experience in senior housing.