Executive Summary: Renting in retirement. In 2026, the financial landscape for retirees has shifted significantly. Rising property taxes, skyrocketing insurance premiums, and the ballooning cost of skilled maintenance labor have made traditional homeownership a potential liability. Choosing to be a “Forever Tenant” allows seniors to unlock “dead capital,” maximize liquidity for healthcare needs, and offload physical risks to professional landlords. This article provides cost transparency tables and technical deep-dives into IRC Section 121 to help you decide if renting is your smartest financial move.

Note: Local labor rates for home maintenance and rental management change constantly. See our full regional cost table below.

Introduction

I’ve spent more than 23 years in the real estate trenches. I have flipped over 100 houses, and I’ve seen it all: from houses that were literally sliding down hillsides to homeowners who lost their entire retirement nest egg because they were “house proud” but “cash poor.” The old American Dream of a paid-off mortgage being the ultimate finish line is starting to look more like a finish line for your bank account. I’m Charles O’Dell, and I’m here to tell you that for many of you over the age of 60, becoming a “Forever Tenant” isn’t just a lifestyle choice; it’s a sophisticated financial power move.

Let me tell you a story. A few years back, I met a couple, the Watsons. They lived in a beautiful, four-bedroom mission style they had owned for 30 years. It was paid off. They were “stable,” or so they thought. But the roof was 22 years old, the HVAC was 18 years old, and the property taxes in their county had just been reassessed. They were “millionaires on paper” because the house was worth $1.2 million, but they were eating generic cereal because their monthly “carrying costs” were eating their Social Security checks alive. From a first-principles perspective, their house was a non-performing asset. It was a pile of bricks that they were paying to live in, rather than an investment that paid them. We are going to look at why that model is broken now for many people.

Video Guide Overview

Affiliate Disclosure

To keep the data fresh and the lights on at HousingAfter60.com, I use affiliate links. If you click one and make a purchase, I may earn a small commission at no extra cost to you. I only recommend technical tools and services that I would trust in my own 100+ property portfolio. Technical accuracy is my priority; these links just help fund the research.

The “Short” Answer

Being a “Forever Tenant” means choosing to rent long-term in retirement instead of owning. In 2026, this strategy can be smarter because it keeps your money liquid and investable, eliminates the risk of major surprise repairs, and provides the flexibility to move as your health or family needs change. While homeowners are stuck dealing with rising property taxes and “insurance deserts,” renters have a capped, predictable monthly cost. However, this strategy requires disciplined financial planning to manage rent inflation and ensure your home sale proceeds are invested wisely. For many, the “peace of mind” of calling a landlord instead of a contractor is the best ROI they will ever see.

What Is a “Forever Tenant” (And Who This Applies To)

Technical Deep Dive: The Logic of Dead Capital and Opportunity Cost

In the world of professional investing, we look at Opportunity Cost. If you have $800,000 tied up in a house, that is dead capital. It is not generating a monthly check for you. In fact, in 2026, it is likely draining your cash flow through property taxes that have outpaced inflation. If you sell that home and invest that $800,000 into a diversified portfolio yielding 5.5% in dividends or interest, you are looking at $44,000 a year in passive income. That’s nearly $3,700 a month. In many markets, that covers your rent entirely, leaving your principal untouched. A Forever Tenant understands that their net worth is a tool to be used, not a trophy to be looked at.

Who Should Consider This?

There are two groups where this logic is undeniable. First, the Middle-Income Retiree who is one major plumbing disaster away from a financial crisis. If a $15,000 sewer line replacement would ruin your year, you shouldn’t be the one responsible for it. Second, the High-Net-Worth Retiree who values capital efficiency. These individuals realize that a $2 million home is a concentrated risk. They’d rather have that money spread across global markets while they rent a luxury condo that offers 24/7 maintenance and a concierge. They choose flexibility over the “pride” of a deed.

The Traditional Case for Owning—and Why It Weakens in Retirement

Technical Deep Dive: Structural Engineering and Maintenance Cycles

I have renovated over 100 properties, and I can tell you that houses have a maintenance clock that never stops ticking. By the time you hit your 60s, if you’ve lived in your home for two decades, you are entering the “CapEx Storm.”

- Roofing Systems: A standard architectural shingle roof for a 2,500 sq. ft. home averages $19,500. If you need a full tear-off due to old decking, add another $4,000.

- HVAC Systems: New 2026 energy mandates have pushed the cost of a high-efficiency heat pump system to nearly $11,000.

- Plumbing: If your home was built between 1975 and 1995, you likely have polybutylene or aging copper. A full re-pipe is a $12,000 to $18,000 job that involves tearing out drywall.

When you are 70, do you really want to be supervising a crew of structural engineers or plumbers? When you rent, these are the landlord’s problems. If the AC dies in July, you simply send a text. If the roof leaks, you aren’t the one climbing a ladder. This is a transfer of physical risk that has a massive psychological benefit.

| Maintenance Item | Labor Cost (2026) | Material Cost (2026) | Total Pro Est. |

|---|---|---|---|

| Full Roof (2.5k sq ft) | $9,500 | $10,000 | $19,500 |

| Main Sewer Line Fix | $12,000 | $3,000 | $15,000 |

| Heat Pump HVAC | $4,500 | $6,500 | $11,000 |

| Affiliate Product | Technical Purpose | 2026 Price Est. |

|---|---|---|

| Moen Flo Smart Shutoff | AI-driven leak detection to save your security deposit. | $499 |

| FLIR One Thermal Cam | Check rental windows for drafts and heat loss. | $249 |

| Lectric XP 3.0 E-Bike | Mobility tool for high-density rental districts. | $999 |

The Real Advantages of Renting in Retirement

Technical Deep Dive: IRC Section 121 and the Tax-Free Windfall

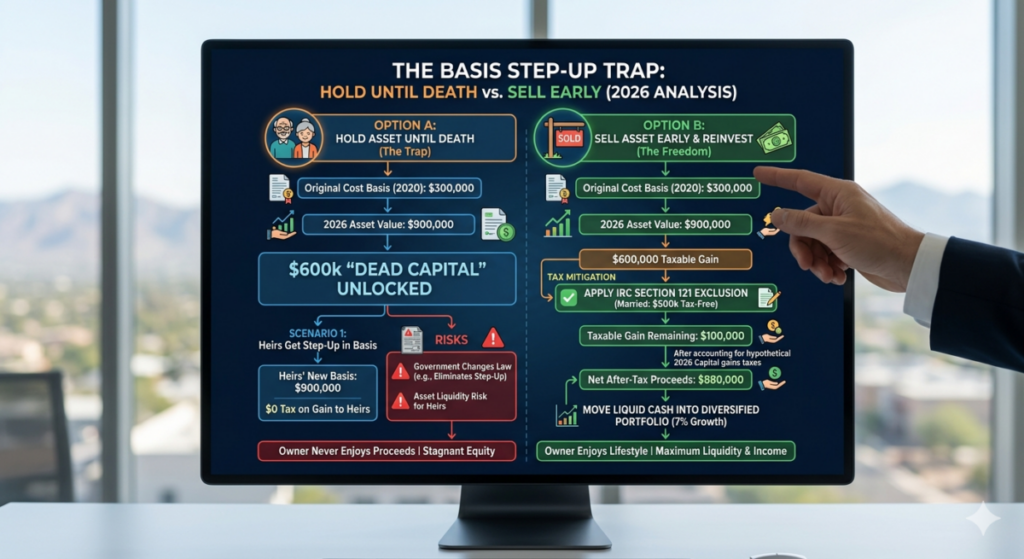

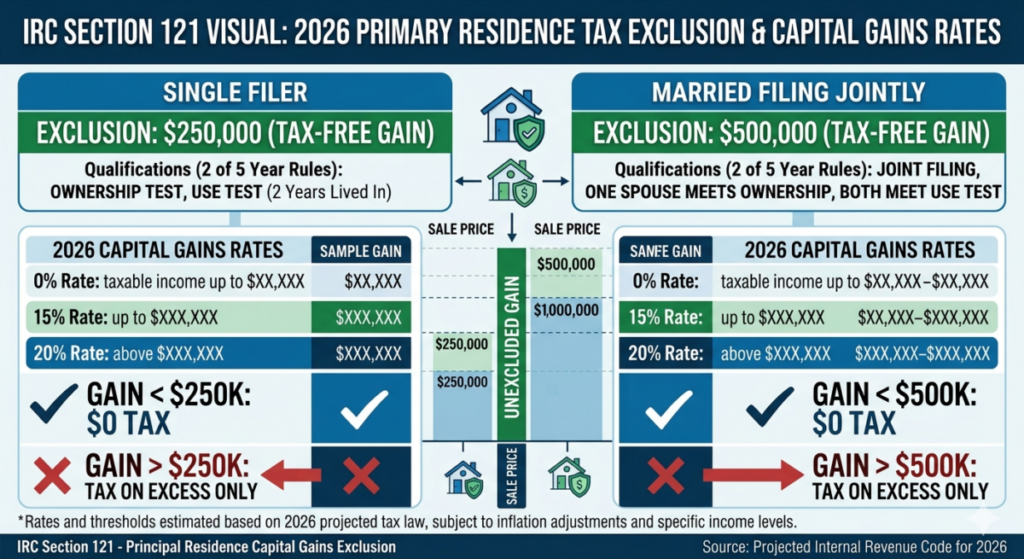

If you are planning to become a Forever Tenant, you have to play the IRS tax code like a fiddle. IRC Section 121 allows you to exclude up to $500,000 (married) or $250,000 (single) of capital gains from the sale of your primary home.

- The “2-in-5” Rule: You must have owned and lived in the home for at least two of the five years leading up to the sale.

- The Step-Up Trap: Many people hold onto their homes until they die so their kids get a Step-Up in Basis. But here’s the problem: you can’t eat that tax benefit while you’re alive. If you sell now, take the $500,000 tax-free, and rent, you have more cash to actually enjoy your life.

- The Timing Risk: If you move out of your home and rent for three and a half years before selling, you lose the Section 121 exclusion because you no longer meet the “2-in-5” criteria. You must sell within three years of moving out to keep that money away from the IRS.

This is a massive tax arbitrage play. You are harvesting your gains tax-free and converting them into liquid capital. In my 23 years as an investor, I’ve seen more wealth built through smart tax timing than through actual property appreciation.

Predictability of Costs and Insurance Shields

In 2026, we are seeing “Insurance Deserts” in states like Florida, California, and Texas. Premiums for homeowners are rising 20% to 50% year-over-year. As a renter, you buy Renters Insurance. It costs about $30 a month. You are not responsible for the $8,000 annual policy on the building. If the landlord’s insurance goes up, they may try to raise the rent, but market competition often prevents them from passing the full cost to you. You are insulated from the insurance death spiral affecting homeowners.

The Hidden Costs of Owning (That Retirees Often Underestimate)

Technical Deep Dive: Zoning Variances and Neighborhood Volatility

When you buy a house, you are also “buying” the local zoning laws. Many cities are aggressively re-zoning single-family neighborhoods for “missing middle” housing (duplexes and triplexes). If you are an owner, you have no recourse if a noisy three-story apartment building goes up next to your garden. Your property value might suffer, or your lifestyle might be ruined. As a Forever Tenant, you have the ultimate power: the 30-day notice. If the neighborhood changes in a way you don’t like, you simply move. You aren’t “locked in” to a depreciating or degrading location. This is Geographic Optionality, and it’s worth its weight in gold.

The “Unseen” ROI of Liquidity

Let’s talk about Liquidity Risk. A house is the most illiquid asset you can own. In a down market, it can take 6 to 12 months to sell. If you have a medical emergency and need $100,000 for private-pay care, you can’t get it out of your kitchen. A bank is unlikely to give a HELOC (Home Equity Line of Credit) to a retiree whose only income is Social Security. But if you are a renter with $1 million in a brokerage account, that money is available in 48 hours. In 2026, cash flow is more important than net worth.

The Real Risks of Being a Forever Tenant

Technical Deep Dive: Rent Inflation and Longevity Risk

I wouldn’t be Charles O’Dell if I didn’t give you the cold, hard truth: Rent Inflation is the biggest threat to this strategy. Over the last 40 years, rents have generally outpaced the Consumer Price Index (CPI).

- The Protection Strategy: You must negotiate Long-Term Lease Riders. In 2026, sophisticated tenants are asking for 3-year leases with pre-set 3% annual increases.

- Supply and Demand: Look for rentals in areas with high apartment construction. High supply means landlords have less pricing power. Avoid “boutique” areas where no new housing can be built; those landlords will squeeze you every single year.

You also face Longevity Risk. If you live to 105, will your equity sustain your rent? This is why we don’t spend the principal of our home sale. We only spend the yield. If you treat your home equity like an endowment, you can survive a 40-year retirement as a tenant.

Financial Comparison: Renting vs Owning in Retirement

The 10-Year Opportunity Cost Scenario

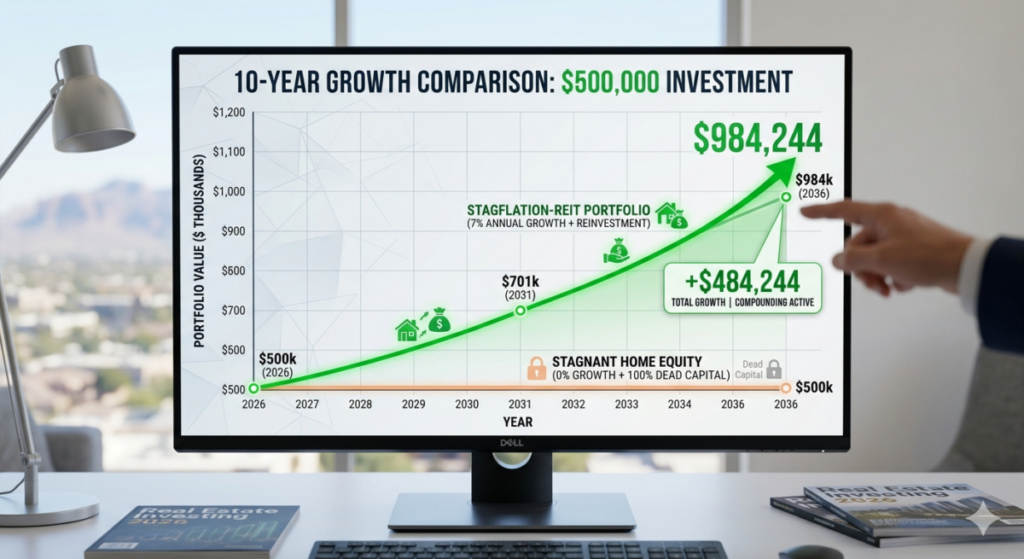

Let’s look at the numbers. Imagine you own a $600,000 home. Your annual taxes, insurance, and maintenance are $18,000. If you keep it for 10 years, and it appreciates at 3%, it’s worth $806,000. You’ve spent $180,000 in “carry costs.” Your net gain is roughly $26,000. Now, imagine you sell, net $550,000 after fees, and invest it at 6%. * Year 1 Income: $33,000. * Total Income over 10 years (compounded): Over $400,000. You use that income to pay $2,800/mo in rent ($336,000 total). The Forever Tenant still has their $550,000 principal plus the remaining $64,000 in excess income. The homeowner is “stuck” with a house that requires a $20,000 roof at year 11. The math isn’t even close.

| Scenario (10 Years) | Homeowner (Keep $600k) | Renter (Invest $550k) |

|---|---|---|

| Estimated Final Asset Value | $806,000 (Property) | $984,000 (Portfolio) |

| Total Out-of-Pocket Expenses | $180,000 (Taxes/Ins/Maint) | $336,000 (Rent) |

| **Liquid Cash on Hand** | **$0** | **$648,000 (After Rent)** |

How to Execute a “Forever Tenant” Strategy (Step-by-Step)

- Calculate Your True “Carrying Cost”: Look at your bank statements for the last 2 years. Sum up property taxes, insurance, HOA, pool maintenance, lawn care, and every trip to Home Depot. This is your housing baseline.

- Get a Hard Real Estate Valuation: Don’t rely on Zillow. Get a professional broker’s opinion. You need to know exactly how much net cash you will walk away with after the 6% commission and closing costs.

- Consult a Tax Specialist: Verify your IRC Section 121 eligibility. Ensure you haven’t used the exclusion on another property in the last 2 years.

- Determine Your Investable Yield: Speak to a fiduciary advisor. How much monthly income can your net equity safely generate? If it’s $4,000, that is your rent budget.

- Identify “Purpose-Built” Rentals: Look for 55+ luxury rentals. These buildings are designed with Universal Design (no steps, wide doors). They are easier to live in as you age than a converted 1920s house.

- Negotiate the Lease: Landlords love stable, high-credit seniors. Ask for a multi-year lease with a fixed increase cap. This is your hedge against rent inflation.

- Setup a “Rental Reserve” Fund: Take 6 months of rent and put it in a separate High-Yield Savings Account. This acts as your “maintenance fund”—except the only maintenance you’re doing is maintaining your lifestyle.

Common Mistakes to Avoid

The “Lump Sum” Spending Trap

The most dangerous mistake is treating your home equity like a lottery win. If you sell your house for $500,000 and spend $100,000 on a luxury RV, you have just sabotaged your Forever Tenant strategy. That $100,000 was supposed to generate $500 a month in rent money. Now, it’s a depreciating asset sitting in a driveway. You must be disciplined. That capital is your housing security; treat it with the same respect you gave your 401k.

Ignoring “Universal Design” in Your Selection

I’ve seen people rent beautiful lofts with industrial stairs because they looked “cool” at age 62. At age 72, after a hip replacement, that loft becomes a prison. When you are a Forever Tenant, you have the luxury of choice. Choose a place with zero-entry showers, lever-style door handles, and elevator access. If you have to move again because you picked a non-accessible unit, the moving costs will eat your ROI. Read my guide on downsizing logic for more on this.

Practical Checklist: Should You Be a Forever Tenant?

- [ ] Is your home equity more than 50% of your total net worth? (If so, you are un-diversified).

- [ ] Are you spending more than 10 hours a month on home maintenance or yard work?

- [ ] Is your property tax bill increasing faster than your Social Security COLA?

- [ ] Do you want to move closer to family without the 6-month hassle of selling a house?

- [ ] Are you comfortable managing an investment portfolio (or hiring a pro)?

- [ ] Can your liquidated equity generate enough yield to cover 80% of your rent?

Internal Resources

For more first-principles real estate analysis, explore our other guides:

- Condo Special Assessments: How to Avoid a $50,000 Surprise

- Bridge Loans: How to Buy (or Rent) Before You Sell

- The Math of Downsizing: Why Smaller is Richer

Summary

In 2026, the decision to rent vs. own is no longer a default one. It is a mathematical choice. Owning offers control and nostalgia, but it comes with the heavy price of illiquidity, variable costs, and physical burden. Renting offers flexibility, simplicity, and the ability to put your “dead capital” to work. The smartest choice is the one that aligns with your 10-year health outlook and your financial floor. I have flipped 100+ houses, and I can tell you this: I’ve never met a renter who was sad that they didn’t have to fix a sewer pipe on Christmas Eve. Embrace the Forever Tenant lifestyle and take back your retirement.

Bio: Charles O’Dell

Charles O’Dell is the Lead Content Strategist for HousingAfter60.com and a veteran real estate investor with 23+ years of experience. He has facilitated hundreds of transactions and completed over 100 property flips. Prior to his real estate career, Charles was a practicing CPA and financial planner with American Express. This background allows him to see through the “marketing fluff” of the real estate industry and provide seniors with logic-driven, cost-transparent solutions. Charles specializes in helping homeowners over age 60 maximize their net worth by navigating the complex world of tax strategy and property management.

Written by Charles O’Dell, a 23-year real estate veteran with 100+ flips and a former CPA background.